Securitized

Markets

Education and access

The securitized market, worth $14.6 trillion, offers investors significant opportunities

Explore each of the U.S. Securitized Markets to learn the characteristics of each asset class

Agency MBS

Mortgage-Backed

Securities

Agency MBS

Mortgage-Backed Securities

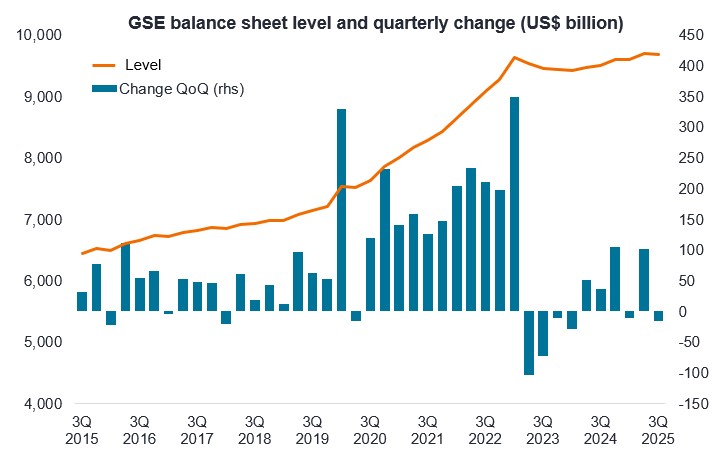

Agency MBS are issued or guaranteed by one of three government or quasi-government agencies: Fannie Mae, Freddie Mac, and Ginnie Mae. Because of this government support, the credit risk within agency MBS is considered negligible, similar to U.S. Treasuries.

Learn moreCMBS

Commercial Mortgage-

Backed Securities

CMBS

Commercial Mortgage-Backed Securities

CMBS are collections of commercial mortgage loans issued by banks, insurers, and alternate lenders to finance purchases of commercial real estate, such as office, industrial, retail, hospitality, and multi-family. CMBS structures help link the financing needs of real estate buyers with investors' capital.

Learn moreCLO

Collateralized Loan

Obligations

CLO

Collateralized Loan Obligations

CLOs are managed portfolios of bank loans that have been securitized into new instruments of varying credit ratings. CLOs have increasingly become the link between the financing needs of smaller companies and investors seeking higher yields.

Learn moreABS

Asset-Backed

Securities

ABS

Asset-Backed Securities

ABS are built around pools of similar cash-flowing assets that include auto loans, credit card receivables, and student loans, all of which grant investors exposure to the consumer credit market.

Learn moreNon-Agency RMBS

Mortgage-Backed

Securities

Non-Agency RMBS

Mortgage-Backed Securities

Non-agency RMBS are created by private entities and do not carry a guarantee from a government agency. Non-agency RMBS are typically comprised of residential mortgages that are unable to meet the criteria to qualify as agency loans.

Learn moreMeet the team behind our success in securitized markets

1st

top growing actively managed fixed-income ETF provider for taxable bond ETFs*

3rd

largest active fixed-income ETF provider by AUM*

$44.6B

in firmwide securitized assets

*Source: Morningstar Asset Flows Data as of 12/31/24

Explore our suite of securitized ETFs

AAA CLO ETF

For investors looking for a fund that seeks to generate yield above money markets while maintaining high-quality benefits.

BBB CLO ETF

For investors looking for a fund that aims to maximize yield in a floating rate strategy.

Mortgage-Backed Securities ETF

For investors seeking above-market total returns by modeling inefficiencies in borrower behavior.

Securitized Income ETF

For investors looking for income diversification and higher yield potential.

Benefits of having securitized assets in your portfolio

Diversify risk exposures

Manage duration & improve credit quality

Access better yield opportunities

Insights

How to play the AI mega-theme in fixed income

Key considerations for investors as they navigate the impact of the rapid acceleration of AI-related capital spending on fixed income markets.

Chart to Watch: Supportive action in mortgages

Exploring the dispersion in the loan market.

CEO Sessions: Understanding individual credits is key to navigating the higher cost of capital environment

Discussion on value opportunities in credit, collateralised loan obligations and mortgages, and why really understanding each credit will be pivotal in 2026.