Key takeaways:

- China’s AI momentum is increasingly about distribution and economics – mass onboarding plus a ‘cost cliff’ that turns AI into a daily utility.

- Versus the US, China’s AI advantages include its open-source approach, state-driven initiatives, and a sensible approach to funding and capacity building.

- Stock-picking opportunities abound given China’s broader systems-level acceleration in AI, with a strong pivot toward agentic use cases with a focus on measurable return-on-investment (ROI).

China’s AI story in 2026 is shifting from “catch-up” to “compete” – and in some areas, to lead. DeepSeek’s R-1 model release in early 2025 questioned US AI dominance and was a wake-up call to the world that China was able to produce cutting-edge AI at much lower cost in comparison to US AI companies like OpenAI’s ChatGPT. At the time, it caused a US$600 billion drop in NVIDIA’s market valuation.1

Impressive humanoid robots dancing and performing martial arts alongside human performers at China’s most watched Lunar New Year gala broadcast wowed the world and served as a reminder of China’s role as a leader in AI, rivalling the US and the Middle East. Those who witnessed the same event a year earlier would have observed that the simple movements on show then had progressed significantly just a year later.

Meanwhile, more recently, the ‘Two Sessions’ conference, which revealed the full details of the Five-Year Plan for 2026-30, re-emphasised China’s increasing emphasis on technology and innovation to drive growth and productivity. This is underpinned by new targets: China aims to increase research and development (R&D) spending by >7% per annum, raise the digital economy’s share from 10.5% to circa 12.5% of GDP by 2030, while maintaining higher labour productivity growth than GDP growth.2

China is leading efforts towards mass adoption of AI

A cluster of major AI models were released around Lunar New Year (Bytedance’s Seedance 2.0, Alibaba’s Qwen 3.5, Knowledge Atlas’s GLM-5, Moonshot’s Kimi K2.5, plus MiniMax M2.7 in March, while DeepSeek V4 is upcoming in April). The celebrations were used as an opportunity for AI to reach an inflation point in terms of increasing AI mass adoption and literacy. Hundreds of millions of users were encouraged to try AI through gamified ‘red packet’ (a tradition where cash is given out during the celebration) campaigns and embedded AI features inside everyday apps and telecom services.

For example, China Telecom integrated its large language models (LLMs) directly into the phone network. Users in lower-tier cities could generate ‘AI video ringtones’ for Chinese New Year greetings with zero prompting skills. We believe this is the ‘red packet’ moment for AI, just as Tencent’s WeChat used red packets to normalise mobile payments back in 2014. The WeChat ‘digital red packets’ feature was introduced and quickly went viral as users sent them to friends and family instead of physical cash. It was also the first time mobile payments were adopted en masse by a wider cohort of users, including in non-urban areas and older age groups.

Adoption at scale can quickly create ‘winner-takes-most’ dynamics in consumer AI – especially where incumbents can bundle AI into existing ecosystems such as payments, commerce, social, and video creation. The real battle begins after the holiday. The winner will not be the company that gives away the most cash, but which can retain these new users.

Overall, ByteDance has been the leader in AI-to-consumer engagement. Alibaba is catching up fast, and Tencent and other existing internet giants are also playing along to retain the users with their existing ecosystem.

China is demonstrating several technological breakthroughs with the release of the latest AI models:

Video generation leadership

Following ByteDance’s low-key launch of Seedance in June 2025, the company released a much more advanced Seedance 2.0 in February 2026, which combines text, visuals and audio to generate cinema-quality short videos at much lower cost. Seedance 2.0 currently looks to be a leader in video generation, outperforming OpenAI’s Sora 2 and Google’s Veo 3 on several metrics.3 This is the first time a Chinese model has claimed top spot in a primary multi-modal track, ie. the capability to understand and process different types of information, such as text, images, audio, and video, simultaneously.

The ‘agent’ revolution

The focus has moved from chatbots to agents – AI that does work. As the agent AI era begins, the metrics for success are becoming more measurable via return-on-investment (ROI), cost reduction and other operational efficiencies.

Examples of China AI technological innovation that is rivalling US peers:4

- Knowledge Atlas’s Zhipu (GLM-5) achieved open-source SOTA-level performance in coding and agent capabilities, and has been recognised as performing on par with Anthropic’s Claude 3.5 Sonnet.

- MiniMax (M2.5) launched the world’s first agent-native (agentic LLM) model (10 billion parameters), designed specifically for executing complex tasks with high efficiency.

- Moonshot (Kimi K2.5) introduced reasoning capabilities akin to OpenAI’s o1 model.

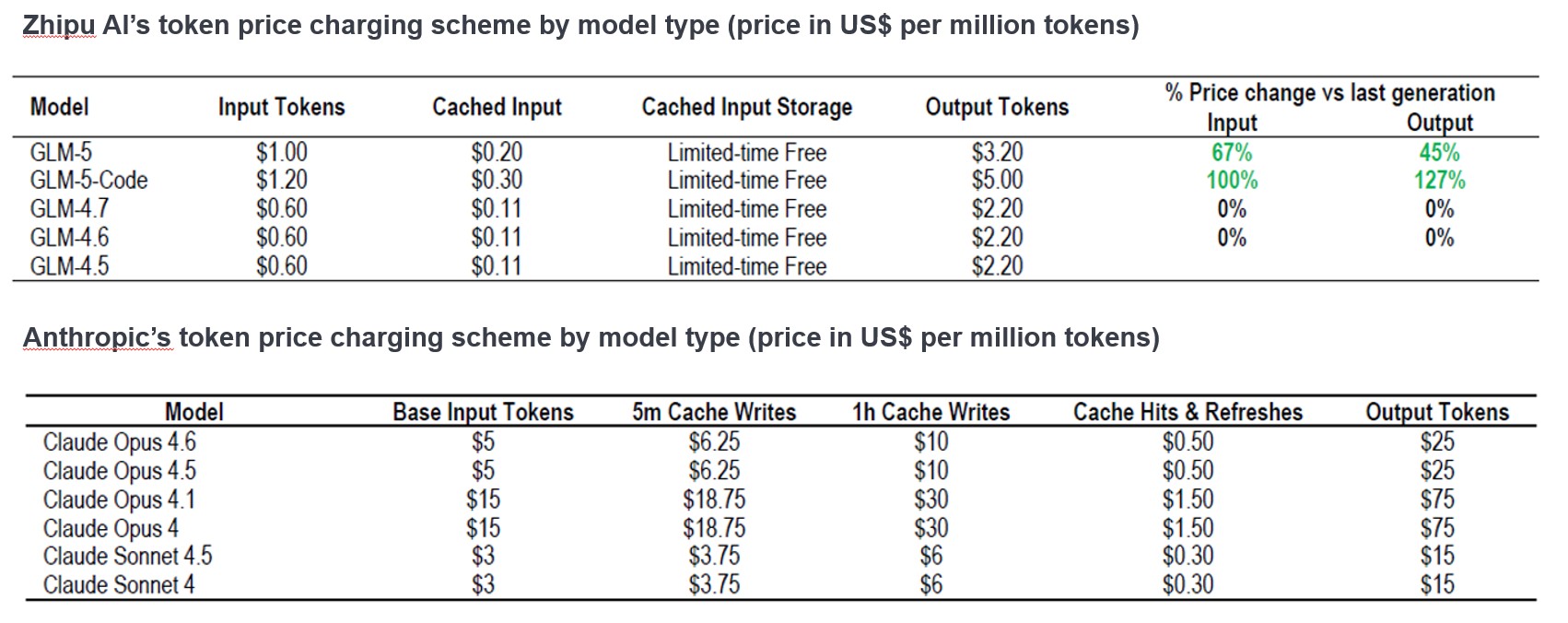

The cost cliff

The cost of agent workflows has plummeted. What cost US$300/month in API calls (allows one application to request data or services from another application) just weeks ago, is now available via domestic open-source models for a fraction of the price. This is enabling AI to transition from being a luxury good to a daily utility.

Figure 1: Cost comparison China AI (Zhipu-GLM) versus US peer (Anthropic-Claude)

Source: JP Morgan; China Artificial Intelligence, Asia Pacific Equity Research; 9 February 2026.

China AI vs US AI: Different strategies, different advantages

While the ‘DeepSeek’ moment in early 2025 drove a re-rating in many China AI stocks, widespread fears of an AI bubble saw some companies’ share prices come under pressure throughout the year. However, year-to-date in 2026, we have seen select AI companies rally hard, buoyed by growing investor confidence in the AI capabilities among China’s AI startups and their growth potential. Also providing a boost is the government’s ‘AI+’ policy, announced in August 2025, which aims to promote extensive and in-depth integration of AI across various areas, across science and technology, industrial development, consumption, wellbeing, and governance.

We believe China has four competitive advantages in the AI race:

1. Open source models

The US market is dominated by closed-source models, where users are restricted from viewing, modifying, redistributing LLM source code and typically subject to licensing. China, by comparison, has aggressively embraced open-source as a competitive strategy. By open-sourcing powerful models, like Alibaba’s Qwen and DeepSeek, Chinese firms are building a huge global user community. This creates a flywheel of iteration – thousands of developers worldwide are testing, fixing, and fine-tuning these models faster than any single closed lab can match. Given token prices in China are only a fraction of US peers, this means high-performance inference is available for fast adoption by enterprises and individuals.

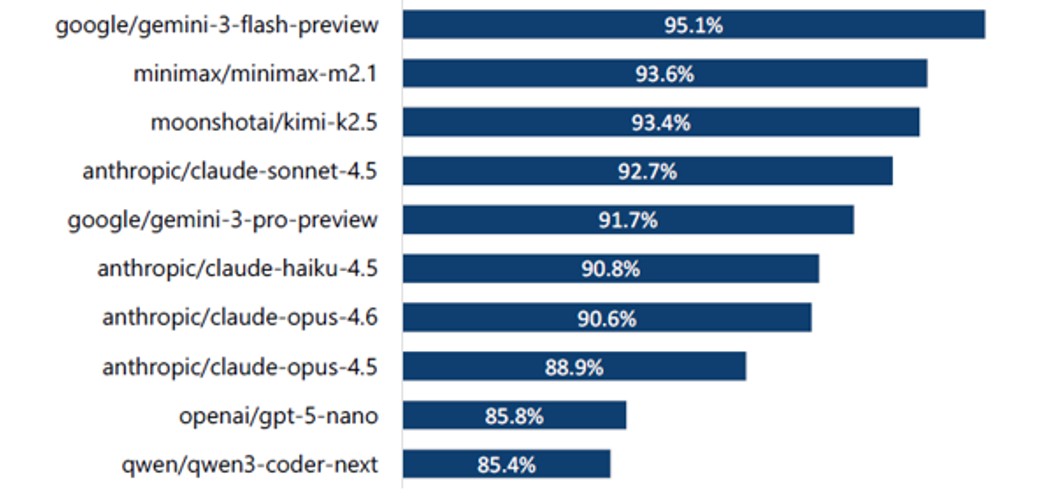

Recently, data from OpenRouter5 showed that token consumption in February 2026 had risen significantly because of a surge in adoption of open source operator OpenClaw. This free open-source autonomous AI agent allows users to move beyond AI chat to ‘do work’ (eg. calendar management, sending emails, checking flights, etc) by connecting with apps like WhatsApp, WeChat, Microsoft Teams, Telegram, and web browsers.

The top three AI models using OpenClaw were all from China, and coincided with the release of several high performance and cost-efficient models, including Moonshot’s Kimi K2.5 (Jan ’26), Minimax’s M2.5 (Feb ’26) and Zhipu’s GLM-5 (Feb ’26).3 While Google’s Gemini 3 was ranked highest in terms of success rate, MiniMax M2.1 was highlighted by OpenClaw’s founder Peter Stringer, as being the recommended LLM in terms of success rate, speed and cost.4

Figure 2: Global top ten LLM models by success rate (8 March 2026)

Source: Jeffries Equity Research: China Internet; PinchBench, Jeffries data; 12 March 2026.

2. Focus on monetisation

With comparatively fewer sources (and quantum) of funding and a more limited supply of advanced chips versus their US rivals, Chinese AI companies have tended to focus more on monetisation. The Chinese ecosystem is ruthlessly pragmatic – we are seeing a pivot away from theoretical benchmarks toward immediate commercial application.

In additional to consumer chatbots, China is also integrating AI more widely across its industries and sectors. Applying AI to industrial processes – such as quality control or supply chain optimisation – is harder than building a chat app. It takes time to implement, requiring deep integration with hardware and real-world data. However, once established, the value generation is immense and often sticky. This is where China’s status as the ‘world’s factory’ enables it to have a significant data advantage versus other countries.

3. State-driven infrastructure

China is doing what it has always done best: building infrastructure faster and cheaper: power generation, chips, data centres, and advanced cooling systems. Central and local governments are building the infrastructure needed, particularly data centres in the western part of China, where solar and wind power is abundant. A state-driven approach can expedite the building out of heavy infrastructure, for example, including the energy grid upgrades and power allocation required for AI clusters.

4. Limited overcapacity risk

Because Chinese capital markets have been tighter (higher capital costs versus the West), there is no irrational exuberance around funding for long-cycle projects. Capital has flowed more sensibly, making the risk of overcapacity significantly lower than in the US.

Investment opportunities: Looking beyond the obvious ‘AI winners’

Apart from China’s internet giants, semiconductor and hardware companies, investors may want to look to the broader China AI ecosystem to diversify their AI exposure. For example, looking to AI infrastructure, building data centres in China requires navigating complex state regulations relating to power consumption and land use. Companies like GDS and VNET have the permits, the power quotas, and the government relationships to facilitate this. Pure AI plays like MiniMax and Zhipu AI look on track to scale their application programming interface (API allows software to communicate with each other) business towards global developers. The revenue mix and margins for related business have the potential to scale up swiftly across the memory and semiconductor supply chains, autonomous driving, and humanoid-related technology and applications.

Conclusion: China’s AI inflection is driven by adoption and scale, not just models

In our view, China is currently undergoing a broader systems-level acceleration in AI: mass onboarding via consumer platforms, rapid iteration through open ecosystems, and a strong pivot toward agentic use cases with a focus on measurable return-on-investment (ROI). This matters for investors, because AI adoption – not just raw model capability – tends to determine who captures profit pools.

Both domestic and international investors are now taking a more constructive view on China’s long-term prospects, despite the near-term challenges facing the economy, including greater global macro uncertainty, a weak property sector and lacklustre domestic consumption. While risks remain, we believe the alignment of the government’s focus to boost productivity with AI, looser monetary policy, a US-China détente and favourable currency dynamics, offers fertile ground for stock picking.

1 BBC News; It shocked the market but has China’s DeepSeek changed AI? 10 August 2025.

2 Morgan Stanley Research; China Musings; 10 March 2026.

3 https://aitoolsreview.co.uk; LantaAI evaluation; 17 February 2026.

4 JP Morgan research, China Artificial Intelligence; 9 February 2026.

5 Jeffries Equity Research: China Internet; data from OpenRouter, Jeffries; 12 March 2026.

Agent-native LLM (or agentic LLM): Refers to a large language model specifically designed to function as the brain of an autonomous agent, rather than just a passive text‑generation tool. Unlike standard LLMs, these models are optimised for reasoning, planning, tool usage, and interacting with external environments to complete multi‑step tasks.

API (Application Programming Interface): An interface for developers to plug AI into software products.

Capex (capital expenditure): Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment, or vehicles in order to maintain or improve operations and foster future growth.

Closed‑source model: A model kept proprietary; users access it via a controlled API or product.

Inference: Refers to artificial intelligence processing. Whereas machine learning and deep learning refer to training neural networks, AI inference applies knowledge from a trained neural network model and uses it to infer a result.

LLM (large language model): A specialised type of artificial intelligence that has been trained on vast amounts of text to understand existing content and generate original content.

Model‑as‑a‑Service (MaaS): Selling AI access via APIs, typically priced by usage.

Multimodal AI: AI that can work with multiple input/output types (text, images, audio, video).

Open‑source model: A model whose weights (core parameters) are released so others can run and modify it.

ROI (return on investment): A financial ratio used to measure the performance of an investment, calculated by dividing net profit/loss by the initial cost of the investment.

Token: AI tokens are the fundamental building blocks of input and output that Large Language Models (LLMs) use. They are the smallest units of data used by a LLM to process and generate text/output that is useful.

Utilisation rate: How much of a data centre’s capacity is actively used by customers.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Emerging markets expose the Fund to higher volatility and greater risk of loss than developed markets; they are susceptible to adverse political and economic events, and may be less well regulated with less robust custody and settlement procedures.

- The Fund may invest in China A shares via a Stock Connect programme. This may introduce additional risks including operational, regulatory, liquidity and settlement risks.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- This Fund may have a particularly concentrated portfolio relative to its investment universe or other funds in its sector. An adverse event impacting even a small number of holdings could create significant volatility or losses for the Fund.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- The Fund follows a growth investment style that creates a bias towards certain types of companies. This may result in the Fund significantly underperforming or outperforming the wider market.