Key takeaways:

- While the market has mostly been concerned with the inflationary effects of the closure of the Strait of Hormuz, we believe risks to global growth could increase the longer the conflict drags on.

- To determine where to best source duration, we believe investors need to gauge a region’s economic health coming into this crisis, as well as its exposure to hydrocarbon imports and its monetary policy mandate.

- With inflation rising globally, we believe investors should favor modest duration in regions that likely won’t raise rates in 2026 and only consider extending duration where flagging growth necessitates looser policy should inflationary conditions allow for it.

Over two months since hostilities erupted between the U.S., Israel, and Iran and one month since a tenuous ceasefire was announced, the Strait of Hormuz remains effectively closed, thus depriving the global economy of one-fifth of the seaborne crude oil and natural gas needed to fuel it. As evidenced by some equities indices reaching record highs in early May and corporate bond spreads remaining tight, investors have largely shrugged, expecting the crisis to be short lived, with the main fallout a transitory bout of inflation. We are less sanguine.

Geopolitical events are notoriously hard to predict. And unlike a financial crisis, they are not resolved through some market-clearing mechanism. Consequently, we believe investors should acknowledge the risk posed by the prospect of the conflict stretching well into the summer – or longer.

Thus far, much of the concern has been on the inflationary impulse reverberating through the global economy. As evidenced by prices at the U.S. gas pump, not even large energy producers are immune. However, the longer this conflict lasts, the greater the risk it presents to economic growth. Higher transportation prices, especially in Europe, could see summer travel fall prey to demand destruction. Elsewhere, economic activity may be curtailed due to a lack of essential feedstock, with a shortage of fertilizer to plant Asian crops an unfortunate example.

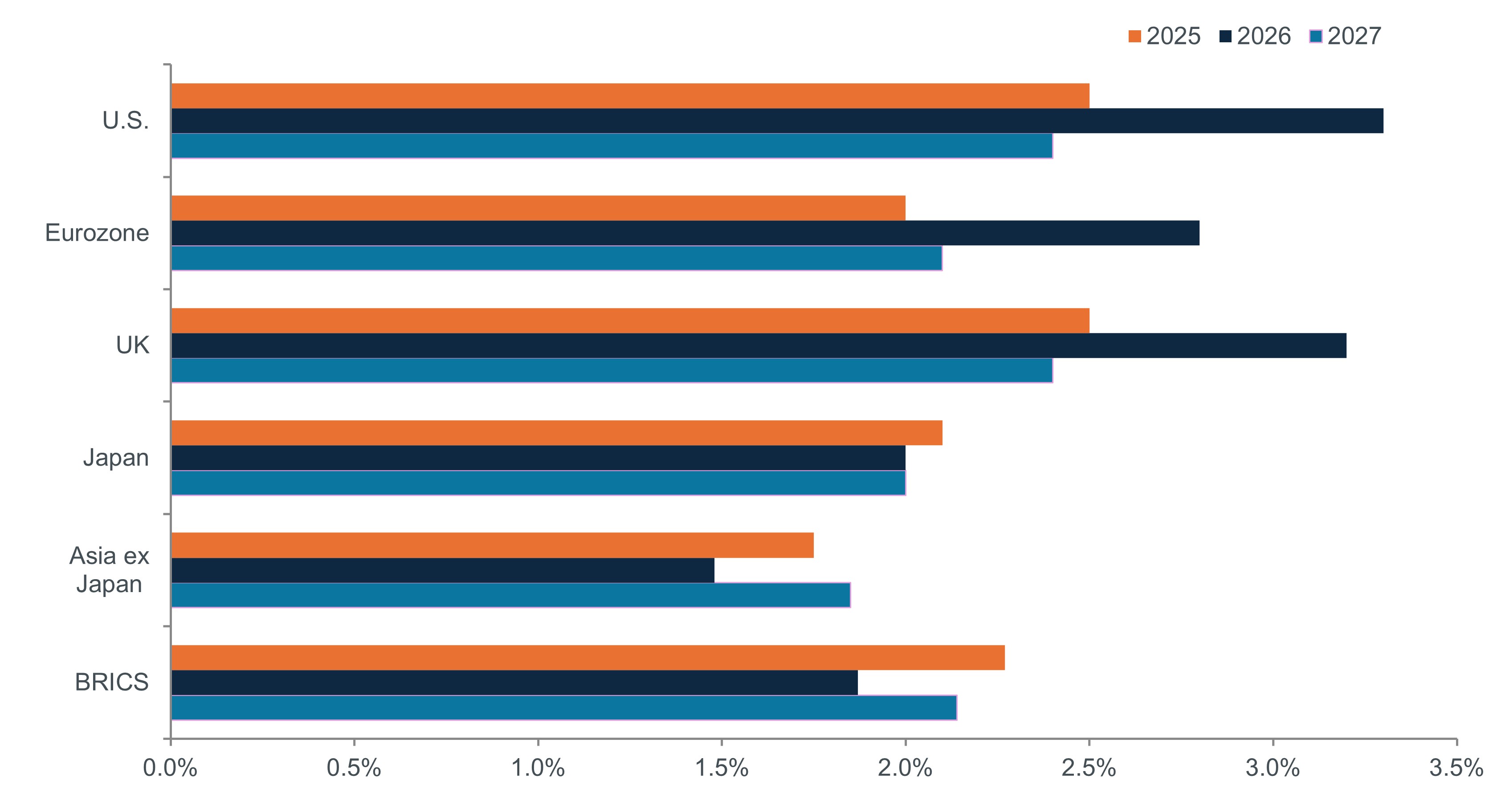

Exhibit 1: Global inflation expectations

The Hormuz crisis illustrates the global nature of energy markets and how even the U.S. – an energy superpower – is not immune to its inflationary effects.

Source: Bloomberg, Janus Henderson Investors, as of 15 May 2026. Forecasts are a consensus of analysts’ and economists’ views and thus should not be interpreted as the definitive path of future developments.

With both inflation and growth being risk factors, we believe investors should seek to position bond allocations to minimize exposure to each of these sources of potential drawdowns. This exercise could also uncover opportunities for capital appreciation within certain jurisdictions and under certain conditions. Given credit spreads’ tightness, duration positioning will likely play an outsized role in determining aggregate bond returns over the next several months. Much will hinge on how inflation and supply constraints impact specific regions and how policy – monetary and fiscal – is adjusted to dampen the impact of this crisis.

A timely framework

While higher energy prices are being felt globally, certain regions are bearing the brunt. The same holds true with risks to growth. To help investors determine how to position portfolios across jurisdictions, we believe a timely framework is necessary. Considerations are:

1. The state of the region’s economy leading into the crisis.

2. Its exposure to commodities-based inflation.

3. The mandate – or prevailing bias – of its central bank.

The dispersion of answers to these questions is surprisingly broad, making it all the more necessary to apply each of these filters to regions within the fixed income universe.

Exhibit 2: Mandates of major central banks

With its dual mandate of managing price levels and the labor market, the U.S. has room to wait, whereas other central banks – even those with slowing economies – may be compelled to raise rates given their focus on inflation.

| Bank | Policy mandate |

| Federal Reserve | Maximum employment, stable prices, moderate long-term interest rates |

| Bank of Canada | Primary objective of low and stable inflation while also supporting maximum sustainable employment |

| European Central Bank | Maintain price stability |

| Bank of England | Maintain monetary and financial stability |

| Reserve Bank of Australia | Stable currency, full employment, economic prosperity and welfare |

| Reserve Bank of New Zealand | Full employment and maintain future purchasing power of money |

Source: Bloomberg, Janus Henderson Investors, as of 15 May 2026.

The U.S.: Insulated, not immune

The degree to which an acute supply shock can have global ramifications is best illustrated by the energy-led inflation spike in the U.S. The country is an energy superpower and is considerably more insulated from Middle Eastern supply disruptions than other regions, but in a global market – such as that for seaborne hydrocarbons – product, and thus price, tend to adjust to reflect changes in aggregate supply/demand dynamics.

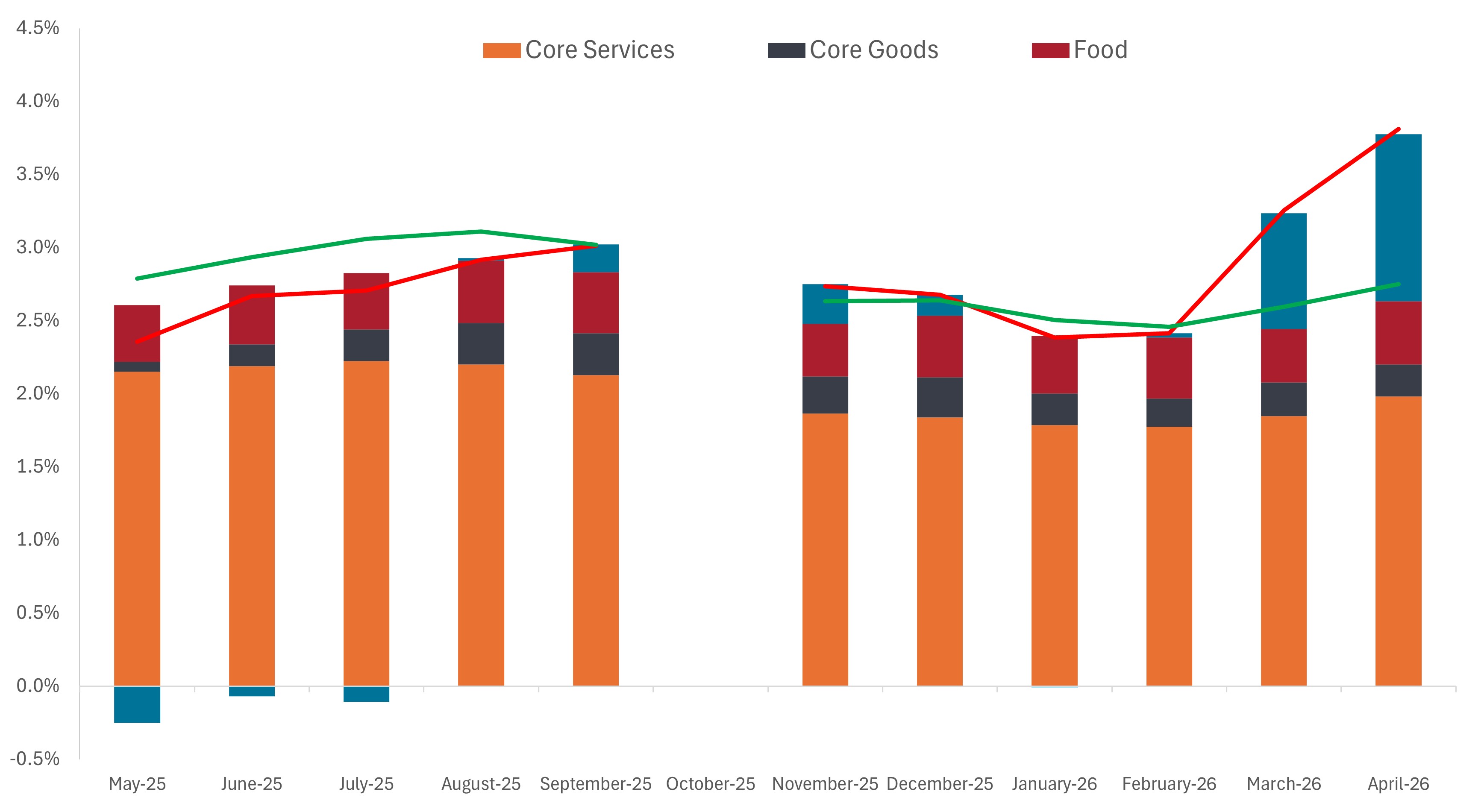

Exhibit 3: Components of U.S. Consumer Price Index

Energy’s contribution to U.S. inflation echoes what is occurring in other regions, except that those highly dependent on energy imports are facing even worse upward price pressures.

Source: Bloomberg, Janus Henderson Investors, as of 15 May 2026. Note: October had no inflation data due to government shutdown.

Entering into the crisis, U.S. economic growth was sturdy. Recent jobs data continue to bear that out. Even prior to the war, there was debate on how much the Federal Reserve (Fed) should cut rates in 2026. The weakness exhibited in 2025 payrolls growth was receding and inflation still resided above the Fed’s 2.0% target. The spike in energy prices largely ended any discussion of rate cuts.

Futures markets now indicate little movement on policy rates into 2027. And while a still a low probability, rate increases have entered the conversation.

The bar for a hike would be high. Continued closure of the Strait of Hormuz could keep upward pressure on energy prices, thus causing them to leach into other parts of the consumer price basket. But ample domestic energy production means that the U.S. would largely be shielded from an economic slowdown attributable to lack of key industrial inputs. And as the recent earnings season indicates, corporate America appears in solid shape, with earnings anticipated to push higher in the quarters ahead.

Furthermore, many economists tend to believe that the inflationary contribution of peak tariffs should roll off year-over-year comparables over the summer, leaving energy prices as the main – and potentially transitory – source of higher consumer prices over the remainder of the year. While a better case scenario, bears would advise monitoring real wages, as higher gas prices could become a headwind for thus-far resilient household spending during the key summer months.

Europe and the UK: Same headaches, different responses?

The situation in Europe is more challenging. Disruption to Middle East energy imports exacerbates supply constraints caused by the Russia-Ukraine war. Leading into the conflict, European growth was already stuck in low gear. And considerably higher energy prices have a greater likelihood of impacting business and consumer behavior than they do in the U.S.

Even with both the UK and the eurozone looking at sub-1.0% GDP growth for 2026, based on consensus estimates, both regions’ central banks will likely be compelled to raise interest rates over the remainder of the year. That central banks would resort to such action – despite monetary policy being an ineffective tool in addressing supply-driven inflation – illustrates the gravity of the situation. But as both the Banks of England (BOE) and the European Central Bank place emphasis on price stability, they likely have little choice given the magnitude – and potential duration – of higher energy prices.

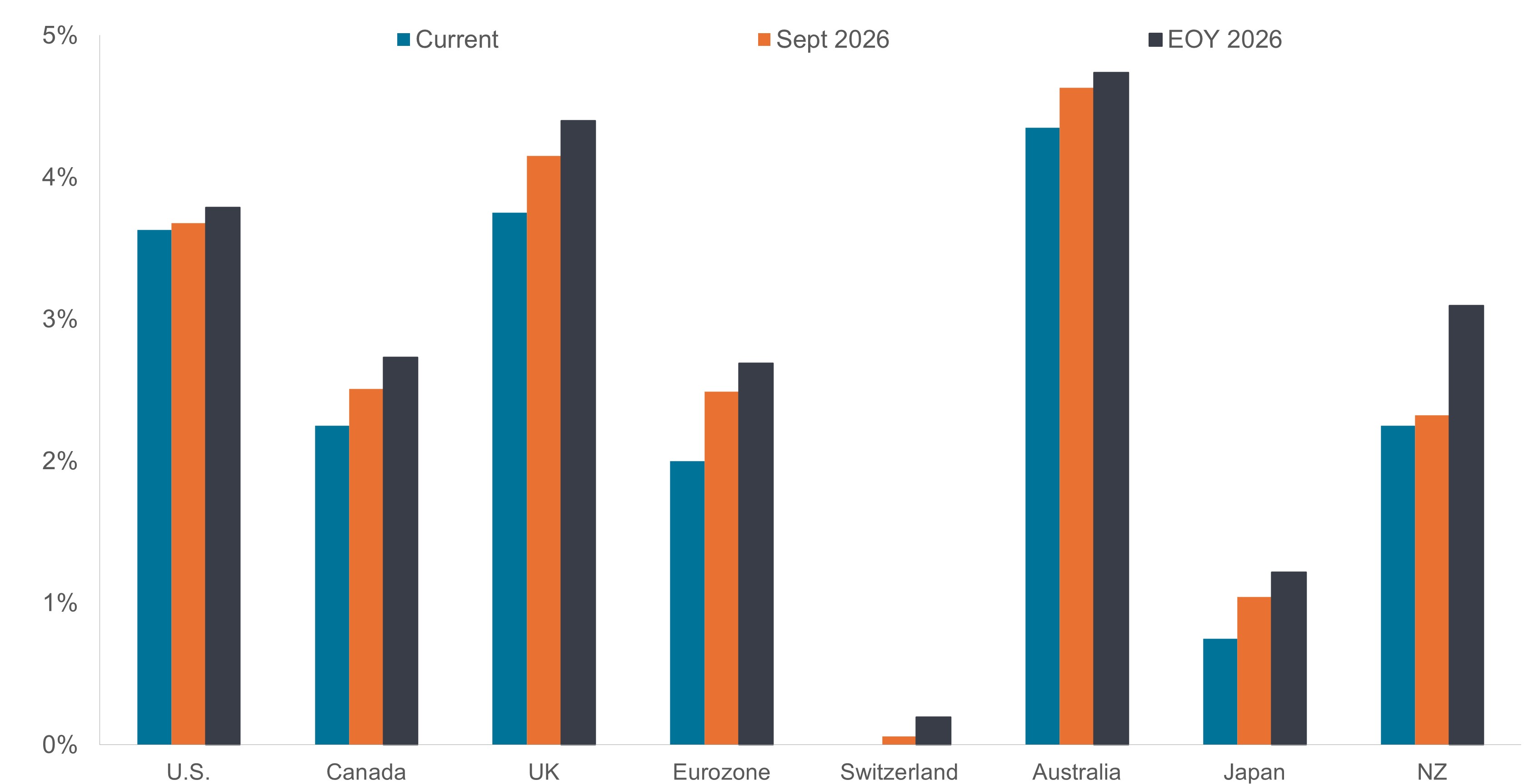

Exhibit 4: Implied interest rates paths over remainder of 2026

Diverging economic trajectories over the past couple of years had allowed for monetary policy paths to chart their own course, but the emergence of energy-related inflation has largely made it a question of “when” and “how much” most central banks will raise rates.

Source: Bloomberg, Janus Henderson Investors, as of 15 May 2026. Implied interest rates are derived from futures and swaps markets, referencing underlying central bank policy rates. These change daily with market prices and cannot be viewed as a definitive future path for monetary policy.

In the UK, the timing is especially inopportune, as poor year-over-year inflation comparables had been rolling off. Had that continued, the BOE could have had the latitude to cut rates. Higher rates, on the other hand, will only add another headwind to flagging economic growth. Addressing growth via fiscal policy is a tenuous discussion point in the UK, as the government is still dealing with the credibility problem set off during Liz Truss’s brief tenure, with succeeding administrations not doing much better in confronting persistent deficits.

In contrast, the eurozone – and especially Germany – has largely been given a pass when leaning into fiscal expansion. For years, austerity had been seen as a brake on growth. The need for defense spending in the wake of Russia’s invasion of Ukraine, along with the ongoing trend of deglobalization, is compelling European governments to invest to improve both military capability and economic competitiveness.

Asia, Australia, and New Zealand: A one-two punch

Asia, Australia, and New Zealand are arguably the regions where both inflation and growth headwinds pose substantial risk. Much of the product flowing through the Strait of Hormuz is bound for Asian markets. Like Europe, Japan is facing sub 1.0%, economic growth in 2026. Sustained higher energy prices would invariably alter consumer behavior as households make tough decisions, while aggregate growth could suffer should key inputs not reach the country’s industrial base. Over the past few years, the country has emerged from its deflationary era, but like other countries, the Bank of Japan (BOJ) is likely mindful of the deleterious effects of eroding household purchasing power. Consequently, while perhaps not to the degree of other regions, the BOJ is more likely than not to increase rates over the next several months.

While Australia may be a major exporter of commodities – namely metals and coal – it must import much of its oil. The health of the country’s export market is inextricably linked to the economic growth of its northern neighbors. Should growth materially slow in Japan, India, and China, Australian miners would suffer.

More directly, the Reserve Bank of Australia has been vexed by elevated inflation for several quarters, with its anticipated policy path already hawkish. Rather than using monetary policy as a blunt tool to quell inflation – which may not work anyway – the Australian government has rolled out an alternative approach in the form of fiscal programs to alleviate pressure on consumers’ wallets. Among these are setting price caps on certain products and delivering energy rebates to businesses and households.

Uncertainty begets patience

Prior to the Iran conflict, global economies had been on diverging economic paths. This typically creates opportunities for fixed income investors to tailor duration and credit exposure to local conditions. This approach has the potential to optimize the tenets of capital preservation and income generation within a diversified bond portfolio. We believe the same philosophy can be effective during a sustained inflationary shock, but with a bias toward capital preservation.

With interest rates having risen since early March, especially along the front end of yield curves, investors can now be compensated for maintaining low duration exposure. The key is to concentrate duration in regions – like the U.S. – that are more likely than not to be on hold perhaps through the remainder of 2026.

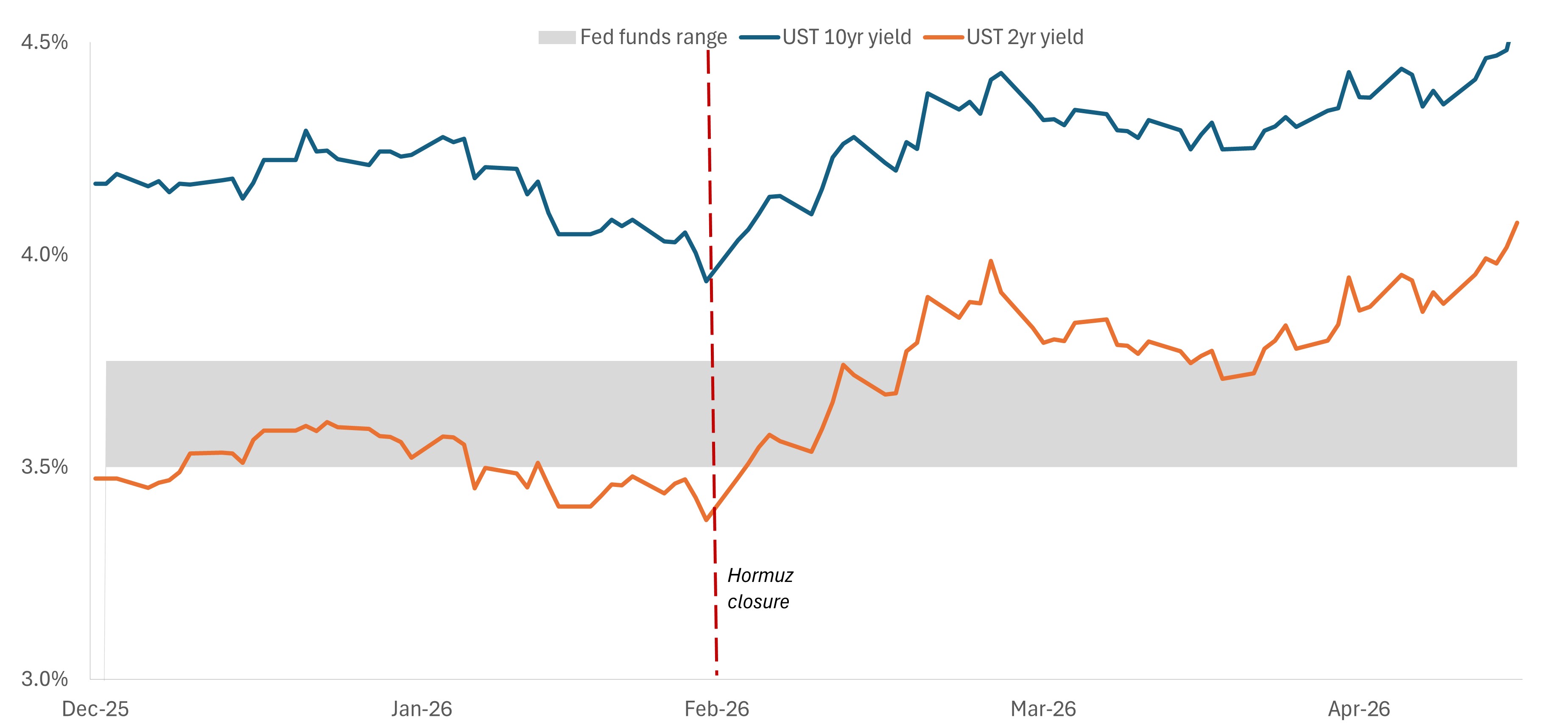

Exhibit 5: U.S. Yields before and after the commencement of hostilities

With shorter-dated yields having already risen, investors can use these maturities to express a guarded view toward duration until greater visibility emerges on how long elevated inflation lasts and where growth may ultimately merit looser policy.

Source: Bloomberg, Janus Henderson Investors, as of 15 May 2026.

In regions dependent upon energy imports, even if oil and liquified natural gas prices don’t climb higher, how long they stay high remains the key variable in how much more policy rates climb and how long they stay there. Until the market gains visibility into this, we’d be cautious about adding interest rate exposure in these regions.

In contrast to the prevailing market view, we are mindful of a binary outcome, with weakening economies being the alternative to sustained inflation. At some point, should growth be fundamentally downgraded and central banks forced to react, we could see investors judiciously increasing duration in regions where policy is likely to ease.

Similarly, if a resolution to the Iran conflict is reached, energy prices fall, and central banks can again prioritize growth in jurisdictions where it’s merited, we could also see extending duration. Neither case, however, has presented itself. Therefore, in our view, caution remains the order of the day.

Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Fiscal policy uses tax policies and government spending to influence macroeconomic conditions, including employment and inflation.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

A yield curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.