Key takeaways:

- Government bond yields have moved materially higher as geopolitical disruption, most notably around the Strait of Hormuz, has reignited inflation concerns and pushed markets to price out rate cuts and even consider further hikes. This has lifted corporate bond yields to attractive absolute levels, especially in investment grade, but reflects macro and political risk rather than a benign growth backdrop.

- While yields look appealing in absolute terms, credit spreads are close to historical tights, implying limited compensation for downside risk. Strong corporate earnings, sector-specific tailwinds (energy, European chemicals, AI-related capex beneficiaries), and solid demand for new issuance have kept spreads compressed even as tail risks from geopolitics, inflation, and policy uncertainty remain elevated.

- Earnings resilience and supportive technicals have underpinned credit markets so far, but risks are building. Potential demand destruction from higher prices, pressure on rate-sensitive sectors, heavy issuance, and the possibility of further rate hikes all argue for caution. With spreads pricing in little negative surprise, this is not an environment that rewards taking excessive credit risk.

Geopolitics and politics more locally is having an outsized impact on fixed income markets this year. Politics is notoriously difficult to predict so credit investors are left trying to understand what the repercussions might be based on the existing economic backdrop and corporate fundamentals.

Underlying change

There has been a recent notable shift higher in government bond yields. This is principally driven by inflation concerns as the closure of the Strait of Hormuz feeds into higher oil prices. Expectations for rate cuts have given way to potential rate rises as central banks look to keep inflation in check. The yield moves have been notable at the short end but also further along the yield curve, particularly in the UK where political concerns around government spending, together with a relatively high level of inflation-linked debt has made markets uneasy.

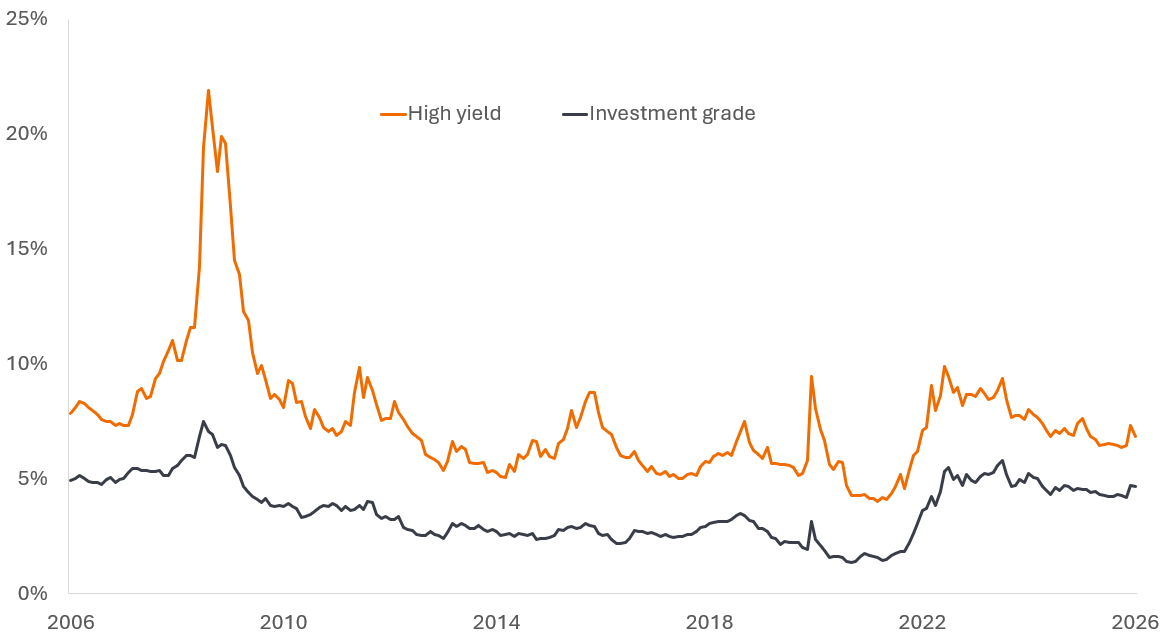

For credit investors the rise in government bond yields has lifted yields across corporate bonds. Relative to the last 20 years (using yield data in Figure 1), yields are around the middle of the pack (44th percentile) for global high yield bonds and high historically for global investment grade bonds (73rd percentile). What this means is that compared with today, yields have been lower on investment grade bonds 73% of the time over the last 20 years.

Figure 1: Global corporate yields look relatively attractive (%)

Source: LSEG Datastream, ICE BofA Global High Yield Bond Index, ICE BofA Global Corporate Bond Index (investment grade), yield to worst, 30 April 2006 to 30 April 2026. Yield to worst is the lowest yield a lowest yield a bond with a special feature (such as a call option) can achieve provided the issuer does not default. Yields may vary over time and are not guaranteed.

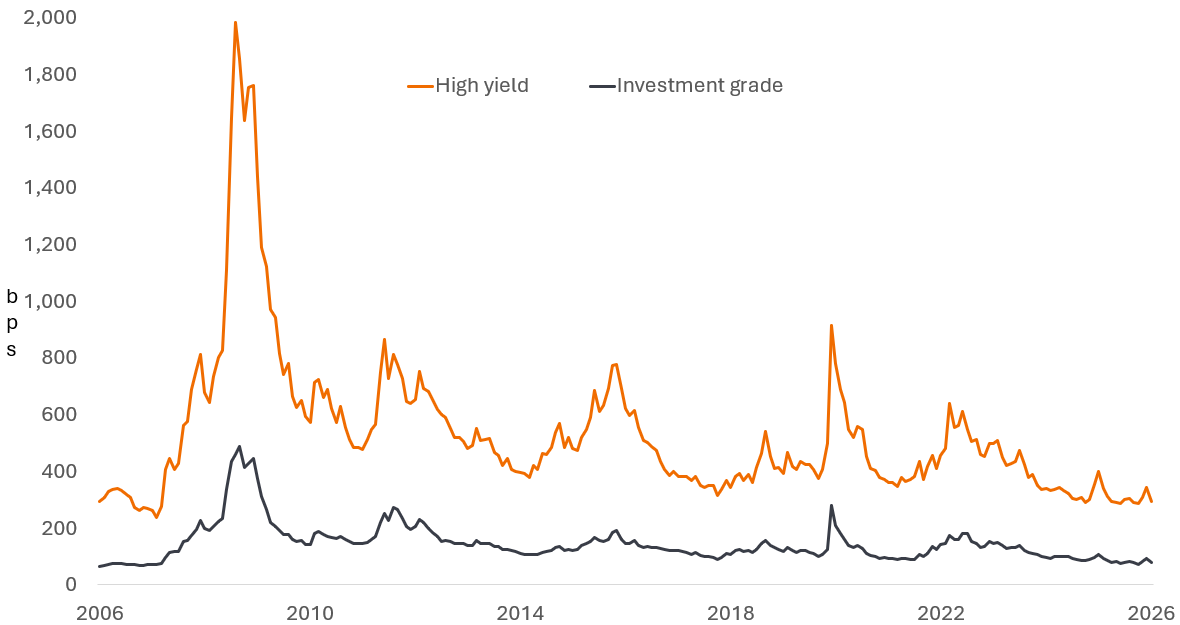

Of course, as credit investors, we are not just interested in yield. We want to know how much extra yield compensation we are receiving for the credit risk of investing in a corporate bond as opposed to the corresponding government bond. This is the credit spread and it is the difference between the yield on a corporate bond and the yield of a government bond of similar maturity. It is typically quoted in basis points. On this measure, credit looks less appealing (Figure 2). High yield is at the 5th percentile and investment grade at 8th percentile, so spreads have rarely been lower.

Figure 2: Global credit spreads are near their tights (basis points)

Source: LSEG Datastream, ICE BofA Global High Yield Bond Index, ICE BofA Global Corporate Bond Index (investment grade), option-adjusted spread over government bonds (OAS Govt), 30 April 2006 to 30 April 2026. Basis point (bp) equals 1/100 of a percentage point, 1bp = 0.01%, 100bps = 1%. Spread percentile ranges based on same data as this chart. Yields may vary over time and are not guaranteed.

That might seem an odd state of affairs when you consider that geopolitical tensions are elevated. There are, however, several factors that seem to be holding spreads at tight levels.

Earnings strength (in unexpected places)

With many companies having reported first quarter earnings for 2026, we have a reasonably good idea of earnings strength. In the US, at the time of writing in early May, some 317 of the 500 companies in the S&P 500 Index had reported, with first quarter earnings 25% higher year-on-year, although closer to 17% if non-operating gains in Big Tech are stripped out.1 It is a similar story in Europe, where 115 out of 244 companies in the MSCI Europe Index have reported, with average earnings growth of 6.8%.2

As might be expected, energy companies globally are benefiting from higher prices, but a less obvious beneficiary is the European chemicals sector. Here, a combination of anti-dumping measures against imported chemicals, together with reduced competition from Asia as raw materials and shipping routes are disrupted, is leading to higher profit margins.

Similar effects can be seen among suppliers meeting the capex spend of hyperscalers. As Big Tech builds datacenters to support artificial intelligence (AI) it is leading to increased demand for energy supply from utilities and electronic equipment makers.

We are mindful that the longer disruption goes on, the higher prices could increasingly lead to demand destruction. It is notable that autos (a big discretionary spend and often requiring financing, which may itself rise if interest rates rise) and travel and leisure (where potential fuel shortages and expiring hedges on fuel could shrink earnings) have seen the steepest downward revisions in earnings recently.3

Technicals

Supply of corporate bonds has been elevated with US investment grade issuance tracking at US$795 billion (up 20% year-on-year). That compares with US high yield issuance of US$111bn (up 49% yoy), European investment grade at €258 bn (+9% yoy), and European high yield at €44bn (+34% yoy).4

So far this year, supply has been well met by investors. A large element of the increase in investment grade supply is related to hyperscaler capex on datacenters to support AI. Given that many of these companies are highly cash-generative and have relatively low borrowing levels, there has been strong appetite from investors.

With the rump of the Q1 earnings season in the rear-view mirror, we think that more companies might approach the market and seek to issue or refinance in the coming weeks. There may be a spot of indigestion, therefore, which could create opportunities in the primary (new issue) market for credit investors as companies may need to offer higher concessions to attract investors.

Valuations the key sticking point

Taken together, credit markets are engaged in a fine balancing act: relatively tight spreads reflect strong corporate fundamentals but signify a market that is pricing in little negative tail risk. For now, the global economy has proved resilient but some of the lagged effects of the Middle East conflict have yet to take effect even if the Strait of Hormuz is reopened. For example, Europe will need to restock its depleted gas inventories over the summer. AI capex has been underpinning growth, so anything that causes this to falter could have negative repercussions. And fixed income markets may have to contend with actual rate hikes if inflationary concerns trump growth prospects among central bankers. In our view, now does not feel like the time to be taking on excessive risk.

1Source: BofA Earnings Tracker, 3 May 2026.

2Source: Morgan Stanley, Earnings Season Monitor, 1 May 2026. Consensus earnings based on IBES data.

3Source: Deutsche Bank, IG and HY Strategy, 28 April 2026.

4Source: Morgan Stanley, year to date to 27 April 2026.

Basis point (bp): One basis point equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

Bond: A debt security issued by a company or a government used as a way of raising money. The investor buying the bond is effectively lending money to the issuer of the bond. Bonds offer a return to investors in the form of fixed-periodic payments (a coupon), and the eventual return at maturity of the original amount invested—the par value. Because of their fixed-periodic interest payments, they are also often called fixed-income instruments.

Capital expenditure: Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment, or vehicles in order to maintain or improve operations and foster future growth.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit spread: The difference in yield between securities with similar maturity but different credit quality, often used to describe the difference in yield between corporate bonds and government bonds. Widening spreads generally indicate a deteriorating creditworthiness of corporate borrowers, while narrowing indicates improving.

High-yield bond: A bond with a lower credit rating than an investment-grade bond, also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher-interest rate (coupon ) to compensate for the additional risk.

Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures; the opposite of deflation.

Primary market/secondary market: Newly-issued bonds are traded on the primary market, with issuers selling their bonds directly to investors to raise capital (borrow). The purchase or sale of any existing bond occurs in the secondary market, between investors.

Valuation metrics: Metrics used to gauge a company’s performance, financial health, and expectations for future earnings, e.g. P/E ratio and ROE.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- CoCos can fall sharply in value if the financial strength of an issuer weakens and a predetermined trigger event causes the bonds to be converted into shares/units of the issuer or to be partly or wholly written off.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.