Key takeaways:

- 2025 saw insured losses from natural catastrophes exceed the US$100 billion mark for the sixth year in a row.

- Climate‑related hazards such as rising temperatures, wildfires, extreme precipitation, flooding, and water stress can directly impair buildings, disrupt real estate operations, increase the cost of insurance and alter the economics of property markets.

- As active real estate specialists we have unique insights into physical risks faced by REITs, enabled by regular property visits, management meetings, and targeted engagement to support our decision-making process.

With global temperatures rising, the increased unpredictability and intensity of extreme weather events have led to both devastating human consequences and record financial impact. 2025 was one of the top three warmest years on record, and marked another year of insured losses over the US$100 billion mark.1 In Los Angeles, the year began with the costliest wildfire event in US history, with it costing approximately US$28 billion in total.2 The second half of the year saw the devastating impacts from tropical cyclones across Asia, as well as significant damage caused by Hurricane Melissa in Latin America. Regions historically considered as lower risk, such as Europe, are also now facing severe climate-related hazards, reinforcing the need for resilience strategies that address intensifying extreme weather events.

Escalating weather patterns: A new reality for real estate

Climate change is an increasingly significant challenge for the real estate sector, carrying both short and long‑term implications. Physical damage to assets, rising insurance premiums, and the costs of enhancing building resilience—such as retrofitting to withstand extreme weather, reducing heat loss and heat gain, and improving energy efficiency—are all factors that must be considered. Together, these issues play a critical role in assessing the long‑term viability and return potential of real estate as a tangible asset class.

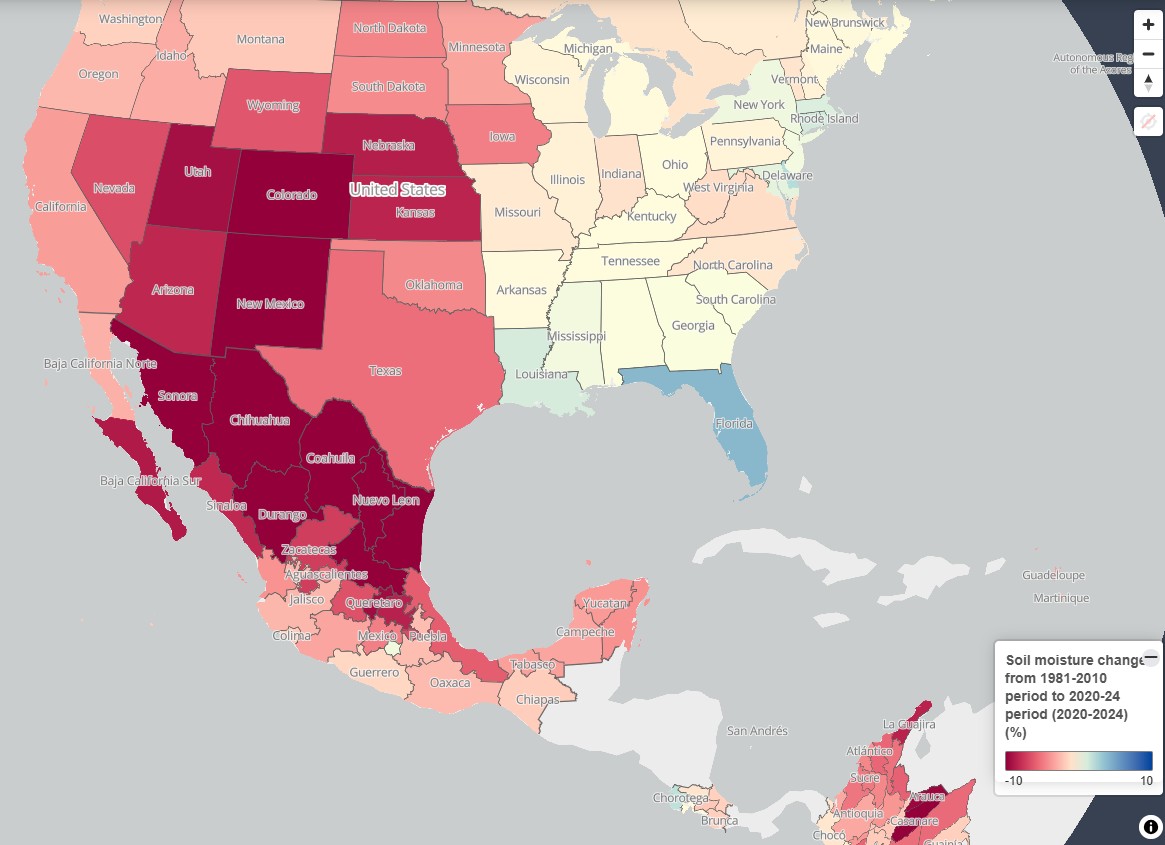

Figure 1: US states exposed to droughts or floods during 2020-2024, compared to 1981-2010

Source: OECD Local Data Portal Climate Monitor; Climate impacts and risks Wet and Dry; 9 February 2026.

As investors in global listed real estate, we are cognisant that property is inherently vulnerable to the impacts of extreme weather. Climate‑related hazards can directly impair buildings, disrupt real estate operations, and alter the economics of property markets. These risks can impact company fundamentals in various ways, for example:

- An increase in maintenance and capital expenditure assumptions, especially where building resilience upgrades are required.

- Higher insurance costs, which can materially alter Net Operating Income (NOI) sustainability.

- Disruption to occupancy and operations, including heat‑related productivity impacts in sectors such as construction and logistics.

- Lower asset liquidity and terminal values, particularly in markets facing structural climatic shifts.

Assessing and integrating physical climate risk

The Global Property Equities Team believes companies adapting to physical climate risks including those of extreme weather, are typically more likely to outperform over time.

A recurring challenge in this area is the limited reliability and coverage of physical risk-data for listed property companies with diverse portfolios of property assets in different climates. As a result, physical climate risk currently remains an important qualitative assessment for many real estate investment managers, rather than a rigid quantitative input.

Engagement with companies—understanding location‑specific exposures, mitigation investments, and insurance dynamics, in our view, is key.

Relative positioning using engagement approach

Company engagement informs our relative value framework that accounts for dispersion between companies. Through site visits, frequent management meetings and targeted discussions with management, we can evaluate which companies are adapting well to climate risk and which companies need to improve. This ensures our physical risk assessment is grounded in real‑world asset and operator understanding. All else being equal, we believe that portfolios with stronger climate‑resilience profiles can typically justify higher expected total returns. For companies with weaker climate practices, our engagement focuses on helping them improve their resilience.

Targeted thematic engagement

In addition to our ongoing discussions, last year we undertook a dedicated engagement in collaboration with Janus Henderson’s central Responsibility Team, specifically working with the Responsible Investment & Governance pillar. We focused this engagement on companies we identified as having the most financially material exposure to climate‑related risks. Topics covered included:

- Asset resilience and climate adaptation strategies

- Strategies to mitigate potential increase in insurance premiums

- Risk assessments for new developments and acquisitions

Regional insights from our engagements

United States

Across the US, real estate investment trusts (REITs) face a variety of different extreme weather events. Residential REITs in particular, are impacted by variability in the pricing of insurance and exposed to the risk of increased premiums. We therefore engaged with companies to understand how they were thinking strategically about managing the costs of insuring their portfolios.

Over time, we have seen REITs increasingly turn to captive insurance policies as well as self-insurance to manage insurance costs. Companies also spoke to their efforts to improve asset resilience and disaster mitigation – whether that’s rebuilding sea walls, landscaping to remove flammable material or as simple as building with raised pedestals on a floodplain. These actions looked to have supported the real estate sector’s in discussions with insurers to help keep premiums manageable.

Europe

Extreme weather and climate change caused more financial damage in Europe between 2020 and 2023 than it did in the whole preceding decade.3

We engaged with REITs with exposure to southern Europe where more frequent and intense extreme weather events have been concentrated. Companies tend to view resiliency as a necessary part of their overall capex budget; we have seen investments into asset protection go as far as adapting photovoltaic (PV) solar panel installations with fire-resistant measures. One company has designed new data centres with zero water usage for cooling. This is critical for maintaining operations in regions at risk of drought, as well as enhancing competitiveness by reducing costs.

The catastrophic Valencia flooding in 2024 caused US$11 billion worth of damage and saw one years’ worth of rain in one day.4 We spoke with a company that was impacted by the event, to understand the measures – such as early warning sensors – that were put into place to ensure the safety of those in the building and reduce the ultimate damage.

Australia

Extreme weather, such as flooding is becoming more prevalent in Australia, particularly in New South Wales and Queensland where there is a concentration of real assets.

We spoke with a REIT with predominately Australian exposure; the company was able to demonstrate how it considered climate risk throughout the portfolio life cycle. For instance, excessive rain had caused delays to construction in the past – actions to mitigate this in future included careful scheduling and early-stage work to enable flexibility.

Building REITs’ resilience for the future

Physical climate risk is a present and growing challenge for real estate investors. Whilst some companies are further ahead in assessing and integrating physical climate risk into acquisition, development and asset upgrade decisions, REITs across all geographies are increasingly engaged on the issue. However, data quality remains a challenge, especially for listed investors. Improved transparency on methodologies for assessing climate risk and evidence of strategic climate planning are essential.

As extreme weather and resilience measures vary by location, assessing risk in REIT portfolios diversified across property types and regions is challenging. This reinforces the importance of on-the-ground research and active engagement with companies to understand asset quality and preparedness at a granular level, ensuring more informed investment decisions for clients.

Modeling physical climate risk is widely acknowledged as essential, yet in practice it remains complex and challenging. Many investors are still working to move beyond high‑level indicators toward embedding climate risk meaningfully into business and investment decisions. Those making progress today, like Janus Henderson, are doing so through sustained analysis and engagement—positioning climate risk assessment as a growing strategic advantage as asset damage and business disruptions accelerate.

Dara O’Rourke, Associate Professor at UC Berkeley’s Rausser College of Natural Resources

Janus Henderson x Berkeley Insight Collective – Content Series

![]()

This article is part of a larger content series showcasing the Janus Henderson x Berkeley Insight Collective. We explore the critical insights and learnings from the co-developed curriculum that aims to empower our investment teams to make more informed decisions on behalf of our clients.

1,2 Gallagher Natural Catastrophe and Climate Risk Report January 2026.

3FT.com; Europe’s bill for extreme weather damage more than doubles this decade; 29 September 2025.

4Munich RE; Climate change and its dramatic consequences; February 2026.

Capital expenditure: Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment, vehicles, software or any other input needed to maintain or improve operations and foster future growth.

Liquidity: A measure of how easily an asset can be bought or sold in the market. Assets that can be easily traded in the market in high volumes (without causing a major price move) are referred to as ‘liquid’.

Net operating income (NOI): A metric used in commercial real estate to measure the profitability of income-generating properties. It represents the income generated by a property after subtracting all necessary operating expenses from the total revenue. NOI is a standardized measure of profitability that allows investors to analyse and compare different property investments.

Physical climate risks: Damages and losses to property that occur due to the physical consequences of climate change. These physical risks result from acute climatic events, such as flooding, wildfires and extreme heat, and chronic climatic events like droughts and coastal inundation.

Real estate investment trust (REITs): An investment vehicle that invests in real estate through direct ownership of property assets, property shares, or mortgages. As they are listed on a stock exchange, REITs are usually highly-liquid and trade like shares. Real estate securities, including REITs, may be subject to additional risks including interest-rate, management, tax, economic, environmental, and concentration risks.

Terminal value: The estimated present value of a business beyond the explicit forecast period; typically taking into account the value of all future cash flows beyond a particular projection period.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- This Fund may have a particularly concentrated portfolio relative to its investment universe or other funds in its sector. An adverse event impacting even a small number of holdings could create significant volatility or losses for the Fund.

- The Fund invests in real estate investment trusts (REITs) and other companies or funds engaged in property investment, which involve risks above those associated with investing directly in property. In particular, REITs may be subject to less strict regulation than the Fund itself and may experience greater volatility than their underlying assets.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.