Key takeaways:

- Equities declined in the first quarter, driven by a large pullback in March as the Middle East conflict pushed energy prices sharply higher, creating concerns about the potential impact on growth and inflation.

- Artificial Intelligence (AI) remained a powerful cross‑sector theme, but rapid advances in AI models accelerated dispersion, reinforcing the need for selectivity as opportunities emerge for well‑positioned companies while risks increase for those vulnerable to AI‑driven disruption.

- Amid an uncertain macro environment and heightened geopolitical tensions, we believe maintaining a long‑term view remains important, with opportunities continuing to favor companies aligned with durable secular drivers such as AI adoption, electrification, and healthcare innovation.

The stock market declined in the first quarter of 2026 after a large pullback in March erased year-to-date gains. Style divergence and sector rotation were the key themes as enthusiasm around AI gave way to greater scrutiny of valuations and capital spending. Concerns around AI‑driven business model disruption also weighed on software and technology‑adjacent sectors, while the escalation of the Middle East conflict and surging oil prices added to volatility in March, with all sectors but energy ending the month lower.

Against this backdrop, market leadership broadened away from mega-cap technology stocks, allowing global indices to outperform their U.S. counterparts. Looking ahead, while we remain mindful of ongoing geopolitical risks and the potential impact of higher energy prices on growth and inflation, we have been reassured by strong corporate earnings and broader market participation globally.

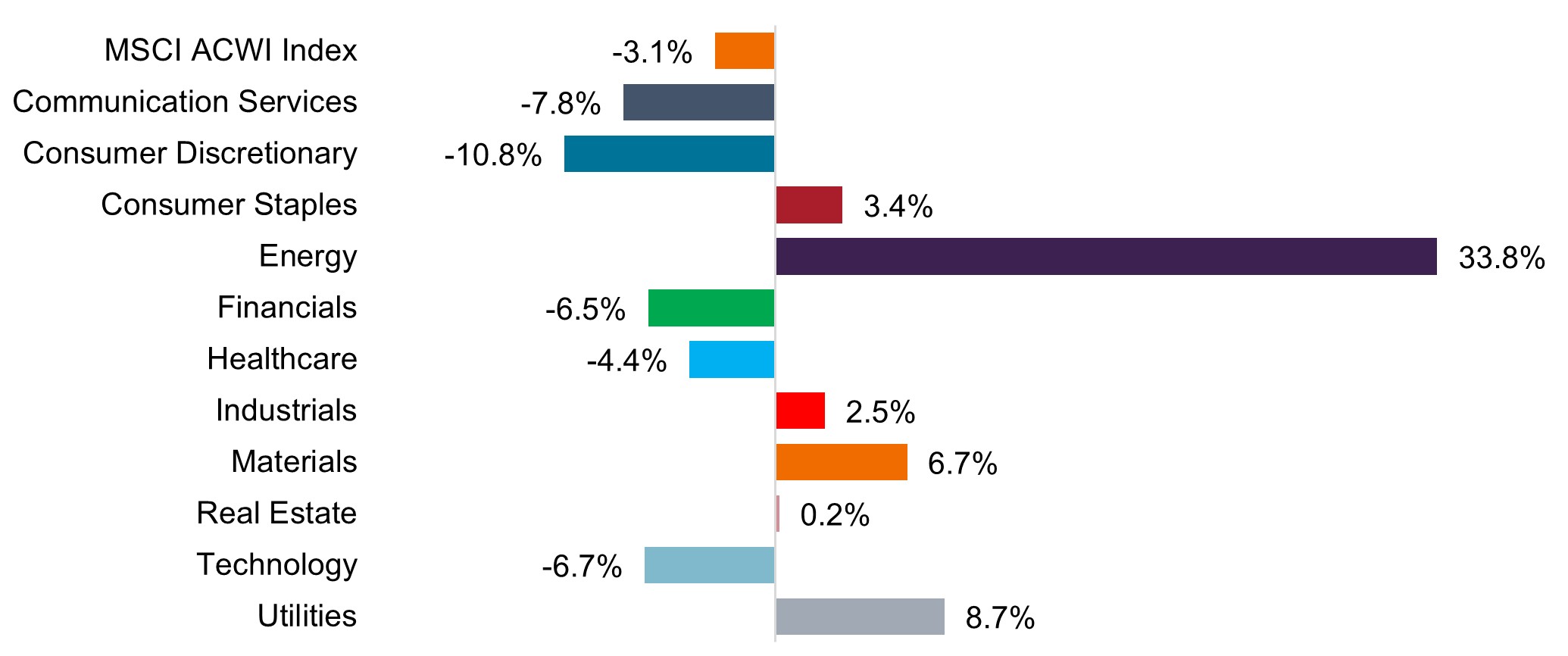

Q1 2026 global equity performance (total return)

Energy rallied amid the surge in crude prices, while utilities and materials also saw strong gains. Consumer discretionary, communication services, and technology sectors were among the worst performers.

Source: Bloomberg, data from 31 December 2025 to 31 March 2026. Returns are for the MSCI All Country World Index (ACWI) and its 11 sectors. The MSCI ACWI Index captures large- and mid-cap representation across 23 developed markets and 24 emerging markets countries. Past performance is no guarantee of future results.

Communication Services

AI innovation and digital disruption remain powerful drivers

What happened: Communication Services stocks underperformed broader market indices in the first quarter, as the conflict in the Middle East spurred more defensive investor behavior. We continued to see divergence in the trajectory of individual stocks across the sector. Shares of Netflix rebounded from fourth-quarter weakness as the company shifted away from its plans to acquire Warner Bros. By contrast, shares of Google-parent company Alphabet and Meta fell despite strong advertising demand, as investors worried over the pace of and potential returns from their tremendous capital investments in AI.

Looking ahead: We remain optimistic on the long-term prospects for the Communications Services sector. We are especially bullish about AI, which in our view has the potential to be even more pervasive and value-generating than the market expects. We believe we could see further consolidation within the sector as both value and investor interest coalesce around the largest digitally native platforms best equipped to attract both content (supply) and users (demand).

Consumer

Opportunities for consumer-facing companies despite near-term uncertainty

What happened: Consumer-related stocks had a challenging first quarter as investors worried over how consumers may adapt to higher gasoline prices, especially heading into the summer driving season. Fears of renewed inflation and even stagflation also weighed on investor sentiment, leading to a rotation away from consumer discretionary stocks, such as home furnishings sellers and online travel agencies, and toward more defensive areas, such as beverage companies and automotive parts retailers.

Looking ahead: Despite near-term uncertainty around oil prices, we believe U.S. households remain on strong financial footing. While we have seen signs of strain on lower-income households, we have also noted continued robust spending by higher-income consumers benefiting from equity-price appreciation. At the same time, we recognize that the ability to spend does not always translate into willingness, especially when consumers face uncertainty, and we recognize we could see more cautious behavior until we have greater clarity on the length and economic impact of the Middle East conflict. We continue to focus on companies with high-quality business models, strong balance sheets, and resilient earnings growth. We have also found opportunities in companies benefiting from secular growth themes such as AI and digitization.

Energy & Utilities

Potential long-term upside given market developments and secular growth themes

Noah Barrett

What happened: Energy stocks delivered strong first-quarter performance, well outperforming the broader market. The war in the Middle East disrupted energy production and distribution networks, triggering fears of a supply shock. As a result, the price of Brent crude oil jumped over 85% during the quarter. Against this backdrop, investors turned more defensive, and utilities stocks were positive performers.

Looking ahead: We expect higher commodity prices to remain a tailwind for energy stocks in the second quarter, even as production disruptions may negatively impact first-quarter financial results for some energy companies. With the Strait of Hormuz closed at the time of this writing, the global market is losing roughly 10 million barrels a day in crude oil supply. We have some buffer against a supply shock, since the market started the year with an oversupply of oil, but inventories are being drawn down. As a result, the market is already pricing in expectations for higher-for-longer oil prices. Even if the Strait reopens, a return to pre‑conflict supply levels will likely be a multi‑month process.

We expect energy demand will continue to rise over the next decade, but we recognize that we may see a growing focus on alternatives and a move away from imported petroleum in China and other markets. As a result, we think there is more downside than upside risk for oil prices over the longer term. We remain defensive in our positioning, even as we focus on energy companies with high-quality, long-term prospects that we believe are underappreciated by the market.

Financials

Seeking out cyclical and secular growth opportunities

What happened: Financials stocks started the year on solid footing, supported by resilient economic and earnings growth and stable consumer spending trends. Later in the quarter, financials stocks sold off on worries over the impact of the Middle East war on energy prices and global economic growth. Investors also tried to assess how advancements in AI technology may impact the sector, and this uncertainty pressured some financials stocks.

Looking ahead: The global financial services sector offers many opportunities for putting our deep fundamental research to work. We continue to see potential around rising global wealth and advancements in technologies such as AI. Growing adoption of AI presents both opportunities and risks to financial business models, and we are actively engaged in research and dialogue to identify potential winners and avoid potential losers. We are also constructive on the outlook for select European banks, which may benefit from an improving regulatory backdrop and potential industry consolidation. Interest rates also remain well above zero in most major markets, which may provide an earnings tailwind for financial services companies.

Healthcare

Innovation and increased M&A continue to create constructive backdrop

What happened: Healthcare stocks ended the first quarter lower amid heightened geopolitical tensions, as the war in Iran raised inflation concerns and lowered expectations for interest rate cuts. Medical device and technology stocks were among the weakest sector performers. Pharmaceuticals stocks registered modest gains, helped by regulatory momentum and landmark drug approvals. Dealmaking also accelerated, with several multi-billion-dollar acquisitions as cash-rich pharmaceutical companies sought to strengthen their pipelines by acquiring firms with unique capabilities or new treatments.

Looking ahead: We believe the outlook for healthcare stocks remains positive despite near-term headwinds and uncertainty around the leadership of key government healthcare agencies. We are excited about the potential for additional drug launches and promising clinical trials. We expect the rapid pace of clinical data releases to continue, with the potential for large new opportunities across oncology, cardiovascular, and neurological diseases, as well as in specialized areas such as myotonic dystrophy and achondroplasia. We also continue to see opportunities across early commercial-stage companies with potential breakthrough products, as well as in lower-risk, late-stage development companies that face less clinical uncertainty. Additionally, we have seen potential with select medical device companies and managed care companies priced at a discount to both historical averages and the market.

Industrials

Remaining focused on stable growers and unique catalysts for profitability

What happened: Industrials stocks delivered modest first-quarter gains while outperforming the broader market. Early in the quarter, industrials shares rose on hopes for a broad-based cyclical recovery. The Institute for Supply Management Purchasing Managers’ Index rose above 50 for the first time since 2022, signaling renewed expansion in manufacturing activity. However, such reports are backward looking, and it remains to be seen how rising energy prices and potential supply chain disruptions may impact near-term industrial activity.

Looking ahead: The outlook for an emerging industrial recovery may hinge on the duration of the Middle East conflict and its impact on global growth and inflation. We are closely monitoring geopolitical risks, commodity prices, interest rates, tariffs, and shifts in consumer and business confidence as we assess conditions across the industrials sector and in cyclical end-markets such as freight. As we await clarity on the near-term environment, we continue to prioritize companies with exposure to strong secular themes, such as commercial aerospace, electrification, and precision farming, that we believe are less exposed to cyclical uncertainty. We are also on the lookout for well-managed companies that are making operational improvements or have unique catalysts that may drive stable profit growth, even in uncertain environments.

Technology

AI remains a generational investment theme

What happened: Information technology stocks delivered mixed performance in a quarter characterized by rapid advances in AI models. Expectations for rising capital spending supported strong share price performance for capital equipment companies, including suppliers of memory chips and optical components required for AI infrastructure. At the same time, shares of hyperscalers fell as investors scrutinized the impact of aggressive AI-related capital expenditures on their cash-flow growth. Software shares also fell on fears that AI-driven solutions may result in new and more disruptive competition to existing business models, especially as the cost of code declines.

Looking ahead: We believe AI is a generational secular trend that will play out over the coming decade, with continued advancements in AI technology and growing demand for AI capabilities. Companies continue to invest rapidly in AI, and we believe they have no incentive to slow their spending as they work to meet surging demand and strengthen their competitive footing. We remain focused on finding the long-term winners from this trend while avoiding businesses that will face secular headwinds. In particular, we have seen opportunity with suppliers of components and materials that are critical to the AI buildout. We believe a selective approach to software investments, with an emphasis on companies using AI to accelerate their businesses or expand their margins, may also be rewarded.

IMPORTANT INFORMATION

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Consumer discretionary industries can be significantly affected by the performance of the overall economy, interest rates, competition, consumer confidence and spending, and changes in demographics and consumer tastes.

Consumer staples industries can be significantly affected by demographics and product trends, competitive pricing, food fads, marketing campaigns, environmental factors, and government regulation, the performance of the overall economy, interest rates, and consumer confidence.

Energy industries can be significantly affected by fluctuations in energy prices and supply and demand of fuels, conservation, the success of exploration projects, and tax and other government regulations.

Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition.

Health care industries are subject to government regulation and reimbursement rates, as well as government approval of products and services, which could have a significant effect on price and availability, and can be significantly affected by rapid obsolescence and patent expirations.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Volatility measures risk using the dispersion of returns for a given investment.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.