Key takeaways:

- Investment‑grade (IG) corporate credit faces supply‑driven headwinds, particularly among the hyperscalers, which have embarked on large, multi-year CapEx programs. We think spreads would need to move materially from current levels before hyperscaler valuations begin to look attractive.

- In contrast to the IG market, high yield offers expanding AI‑linked opportunities, with minimal direct issuance exposure to the hyperscalers, stronger technicals, and better valuations.

- While securitized credit provides some of the most attractive relative value opportunities, the securitized landscape may come with potentially higher risk, necessitating an active, research-driven approach, in our view.

The rapid acceleration of artificial intelligence (AI)-related capital spending is reshaping the fixed income landscape, primarily through a sharp increase in bond issuance from large technology and infrastructure-heavy issuers. The near-term implications for investors are nuanced, with supply dynamics, balance sheet discipline, and entry point selection playing a decisive role in outcomes.

As a result, evaluating fixed income markets through the AI lens requires moving beyond the headlines and focusing instead on how issuers finance AI capital expenditures (CapEx), whether spreads compensate for risk, and how investment-grade (IG) corporate opportunities stack up against AI-linked alternatives in high yield and securitized sectors.

1. IG corporates

The AI infrastructure buildout (data centers, chips, power, networking) is driving large, multi-year CapEx programs, particularly among hyperscalers.1 AI-related issuance represents hundreds of billions of dollars annually at the corporate level, and thus far has been concentrated within IG markets. Consequently, even strong issuers face near-term technical drag amid the sharp increase in supply.

Higher gross issuance has not had a uniform effect on credit spreads. Rather, we have started to witness notable divergence at the security level, with credit impacts differing materially by an issuer’s balance sheet strength, business model, and willingness to protect bondholders. In our view, this divergence makes active management ever more important in the current environment.

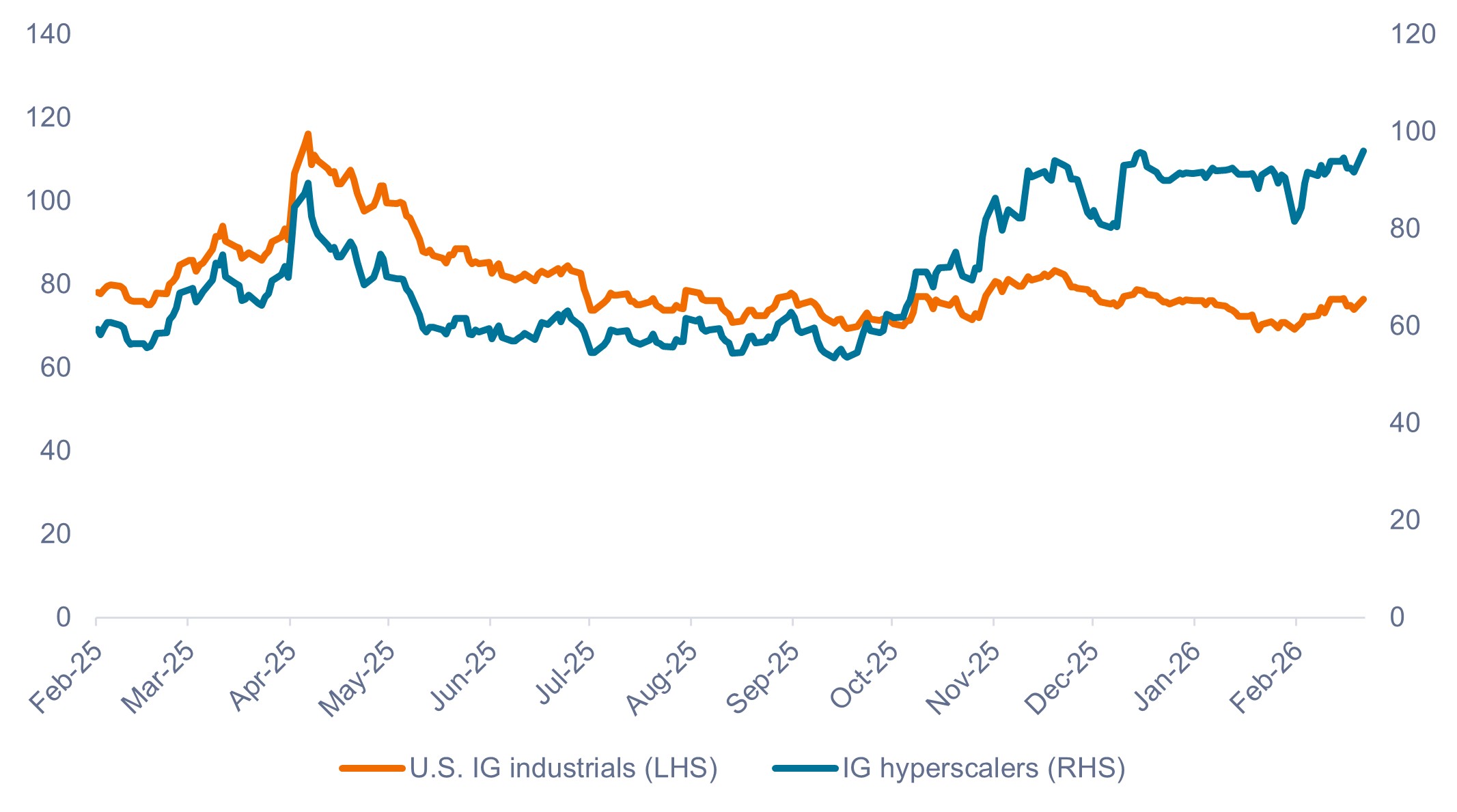

As shown in Exhibit 1, hyperscaler spreads remained tight (in our view, unsustainably so) relative to industrials for much of 2025, before starting to widen late in the year to reflect their ambitious CapEx plans.

Exhibit 1: Hyperscaler vs. IG industrials credit spreads (Feb 2025 – Feb 2026)

Hyperscaler spreads began to widen late in Q3 ’25 but might not yet fully reflect technical and fundamental risks.

Source: Bloomberg, Janus Henderson Investors, as of 23 February 2026.

Historical research shows that large CapEx cycles funded primarily with debt have tended to be followed by meaningful spread widening. Despite the recent widening, we believe the hyperscaler cohort remains historically expensive, as current spreads still reflect strong confidence in execution, leaving limited margin for error.

Essentially, we think spreads would need to move materially from current levels before hyperscaler valuations begin to look attractive.

2. High yield

The rapid buildout of AI infrastructure is expanding the opportunity set for high-yield credit, where technicals are far more constructive compared to IG corporates. The high yield market is less impacted by the massive amount of issuance from IG-rated hyperscalers, while interesting opportunities in ancillary industries are opening up, which we recently covered in detail.

Early beneficiaries within high yield have been power generators – particularly Independent Power Producers (IPPs) – given AI data centers’ surging energy needs and hyperscalers’ long-dated power contracts. (To put the power demand of AI chips and application in perspective, some estimates suggest that three New York City’s worth of power will be needed to sustain the grid by 2030.)

As power constraints intensify, opportunities have broadened to AI-linked data centers, including firms pivoting from Bitcoin mining to high performance computing (HPC), supported by innovative lease-backed financing structures that prioritize debt service.

A new class of AI native “neo cloud” operators further extends the investable universe, while upstream suppliers in memory and networking add cyclical and secular exposure.

Finally, while competitive alliances across chips, cloud, and software are reshaping the ecosystem and creating both opportunity and volatility, overall AI driven CapEx is expected to continue to support a growing range of high yield issuers across the data center supply chain.

We think valuations are also more attractive in the high yield segment. As an example, BB rated Terawulf Inc. emerged as the first Bitcoin miner to pivot toward HPC with a long term lease from Google and tap the high yield market for financing. Its 2030 bonds – which come with a lease backstop from Google – presently offer around 260 basis points (bps) of excess spread over U.S. Treasuries, while Google’s bonds of similar duration offer just 35 bps of spread over Treasuries.

3. Securitized credit – ABS and CMBS

In our view, some of the most attractive opportunities related to the data-center buildout exist within asset-backed securities (ABS) and commercial mortgage-backed securities (CMBS). That said, these deals also come with potentially higher risk and uncertainty, and it is therefore critically important to adopt an active, research-driven approach. The deal structures are very important, as is the technology behind the data center, where it’s located, who the tenants are, etc.

Technicals in the ABS and CMBS market look more attractive to us than in the IG corporate space. Combining ABS and CMBS, we expected $25 to $30 billion of new issuance a year. We think that’s easily digestible for a roughly $5 trillion (excluding agency MBS) securitized market.

We believe valuations on AI-linked bonds are also most attractive within securitized credit, potentially offering the highest upside. Indicatively, various BBB-rated CMBS and ABS deals currently offer over 300 bps in spread over Treasuries, whereas similarly rated prime auto ABS may trade in the 125 bps range. Essentially, one can get double the spread of some of the other fixed income asset classes with the same credit rating via securitized credit.

While Janus Henderson never relies on ratings to price risk and determine relative value, it does point to the disconnect between sectors in the securitized markets where our bottom-up, research-driven approach may discern opportunity.

Summary

Given IG corporate credit’s supply‑driven headwinds, particularly among the hyperscalers, we think spreads would need to move materially from current levels before hyperscaler valuations begin to look attractive. In contrast, high yield and securitized sectors may offer expanding AI‑linked opportunities with better technicals and more attractive valuations.

Importantly, the evolving fixed income landscape may come with potentially higher risk and uncertainty, necessitating, in our view, an active, research-driven approach backed by a strong team with extensive experience investing in corporate and securitized markets.

Janus Henderson’s model of collaboration and knowledge-sharing among fixed income, securitized, and equity research analysts may allow us to provide differentiated and well-informed insights.

1 The hyperscaler cohort is made up of Microsoft, Google, Meta, Amazon, and Oracle.

Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Excess return is the total return of a bond or portfolio minus a benchmark return (often a risk-free rate or duration-matched risk-free bond). It measures the performance above what is expected, representing the compensation for taking on additional credit, interest rate, or liquidity risk beyond the risk-free rate.

IMPORTANT INFORMATION

Actively managed portfolios may fail to produce the intended results. No investment strategy can ensure a profit or eliminate the risk of loss.

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield bonds, or “junk bonds,” are corporate debt securities with lower credit ratings (below BBB−/Baa3) that offer higher interest rates to compensate for a greater risk of default. They are issued by companies with lower creditworthiness or high debt levels. While riskier, they offer higher income potential and lower sensitivity to interest rate changes.

Investment-grade securities: A security typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments. The higher quality of these bonds is reflected in their higher credit ratings when compared with bonds thought to have a higher risk of default, such as high-yield bonds.

Securitized products, such as mortgage-backed securities and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.