Key takeaways:

- Tech’s meteoric growth in recent years has left many investors underweight to the sector. Many remain hesitant to increase allocations, citing valuations and concerns about sustained growth.

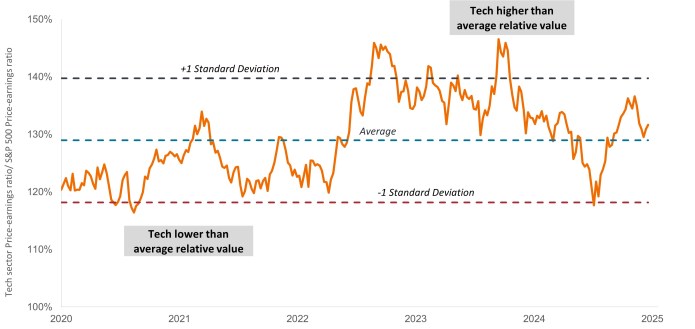

- Tech’s earnings multiples are not stretched relative to the broader market in historical terms, and this premium is arguably justified given the sector’s superior margins and higher expected earnings growth.

- Given our expectation that tech will continue to account for a rising share of aggregate corporate earnings, current entry points invite conversations about how higher tech exposure can benefit broader portfolios.

Source: Janus Henderson Investors, Bloomberg, as of 19 September 2025.

Note: Price-earnings ratios based on blended forward 12-month earnings estimates.

Conversations about how tech fits within a broader equities allocation invariably include two questions: First, “Doesn’t it account for a large portion of the benchmark?” and second, “Isn’t it expensive?”

The share tech and internet stocks in the S&P 500® Index has expanded to roughly 40%. This has left investors who had been underweight tech even less exposed to powerful secular themes such as artificial intelligence (AI). Others trimmed exposure during the rally, seeking to avoid concentration. But there is risk to being materially underweight tech.

Our view is that, as themes like AI play out over a multi-year horizon, leading tech companies will compound earnings at a rate far higher than that of broader equities. Modestly increasing tech exposure – but still keeping it under market weight – can position investors to participate in themes that we believe are likely to account for an increasing portion of aggregate corporate earnings.

In the past five years, technologies like cloud computing were first catalyzed by the digital transition brought by COVID-19 lockdowns then joined by the generational theme of AI. The power of the sector’s business models is illustrated by operating margins expected to average 34% over the next two years, compared to 18% for broader stocks. Attractive margins and top-line growth are estimated to deliver earnings growth averaging 19% over the next two years compared to 13% for the S&P 500.

These projections, when coupled with reasonable valuations, provide a compelling argument for investors to reconsider the size of their tech allocation.

We believe the market continues to underappreciate the ability of leading tech companies to compound earnings across the duration of the secular theme with which they are associated. Within this context, many of these innovators’ valuations remain reasonable.

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

Related insights

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Non vi è alcuna garanzia che le tendenze passate continuino o che le previsioni si realizzino.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

Tutti i contenuti del presente documento hanno solo scopo informativo o di utilizzo generale e non riguardano nello specifico i requisiti di singoli clienti.

Janus Henderson Capital Funds Plc è un OICVM di diritto irlandese con separazione patrimoniale tra i comparti. Si ricorda agli investitori che le rispettive decisioni d'investimento vanno intraprese solo in virtù del Prospetto più recente che contiene informazioni su commissioni, spese e rischi ed è disponibile presso tutti i distributori e gli agenti per i pagamenti/agente per i serviz e va letto con attenzione. Questa è una comunicazione di marketing. Consultare il prospetto dell’OICVM e il KIID prima di prendere qualsiasi decisione finale di investimento. Il fondo può non essere adatto a tutti gli investitori e non è disponibile per tutti gli investitori in tutte le giurisdizioni. Non è disponibile per i soggetti statunitensi. I rendimenti passati non sono indicativi dei risultati futuri. Il tasso di rendimento può variare e il valoredel capitale investito è soggetto a oscillazioni a causa dell'andamento del mercato e dei tassi di cambio. In caso di rimborso, il valore delle azioni può essere maggiore o minore del rispettivo costo iniziale. Il presente documento non costituisce una sollecitazione alla vendita di azioni e nessun contenuto dello stesso è da intendersi come una consulenza agli investimenti. Janus Henderson Investors Europe S.A. può decidere di risolvere gli accordi di commercializzazione di questo Organismo d'investimento collettivo del risparmio in conformità alla normativa applicabile.

- Le Azioni/Quote possono perdere valore rapidamente e di norma implicano rischi più elevati rispetto alle obbligazioni o agli strumenti del mercato monetario. Di conseguenza il valore del proprio investimento potrebbe diminuire.

- Le azioni di società a piccola e media capitalizzazione possono presentare una maggiore volatilità rispetto a quelle di società più ampie e talvolta può essere difficile valutare o vendere tali azioni al momento e al prezzo desiderati, il che aumenta il rischio di perdite.

- Un Fondo che presenta un’esposizione elevata a un determinato paese o regione geografica comporta un livello maggiore di rischio rispetto a un Fondo più diversificato.

- Il Fondo si concentra su determinati settori o temi d’investimento e potrebbe risentire pesantemente di fattori quali eventuali variazioni ai regolamenti governativi, una maggiore competizione nei prezzi, progressi tecnologici ed altri eventi negativi.

- Questo Fondo può avere un portafoglio particolarmente concentrato rispetto al suo universo d’investimento o altri fondi del settore. Un evento sfavorevole riguardante anche un numero ridotto di partecipazioni potrebbe creare una notevole volatilità o perdite per il Fondo.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Qualora il Fondo detenga attività in valute diverse da quella di base del Fondo o l'investitore detenga azioni o quote in un'altra valuta (a meno che non siano "coperte"), il valore dell'investimento potrebbe subire le oscillazioni del tasso di cambio.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.