Key takeaways:

- Investment‑grade (IG) corporate credit faces supply‑driven headwinds, particularly among the hyperscalers, which have embarked on large, multi-year CapEx programs. We think spreads would need to move materially from current levels before hyperscaler valuations begin to look attractive.

- In contrast to the IG market, high yield offers expanding AI‑linked opportunities, with minimal direct issuance exposure to the hyperscalers, stronger technicals, and better valuations.

- While securitized credit provides some of the most attractive relative value opportunities, the securitized landscape may come with potentially higher risk, necessitating an active, research-driven approach, in our view.

The rapid acceleration of artificial intelligence (AI)-related capital spending is reshaping the fixed income landscape, primarily through a sharp increase in bond issuance from large technology and infrastructure-heavy issuers. The near-term implications for investors are nuanced, with supply dynamics, balance sheet discipline, and entry point selection playing a decisive role in outcomes.

As a result, evaluating fixed income markets through the AI lens requires moving beyond the headlines and focusing instead on how issuers finance AI capital expenditures (CapEx), whether spreads compensate for risk, and how investment-grade (IG) corporate opportunities stack up against AI-linked alternatives in high yield and securitized sectors.

1. IG corporates

The AI infrastructure buildout (data centers, chips, power, networking) is driving large, multi-year CapEx programs, particularly among hyperscalers.1 AI-related issuance represents hundreds of billions of dollars annually at the corporate level, and thus far has been concentrated within IG markets. Consequently, even strong issuers face near-term technical drag amid the sharp increase in supply.

Higher gross issuance has not had a uniform effect on credit spreads. Rather, we have started to witness notable divergence at the security level, with credit impacts differing materially by an issuer’s balance sheet strength, business model, and willingness to protect bondholders. In our view, this divergence makes active management ever more important in the current environment.

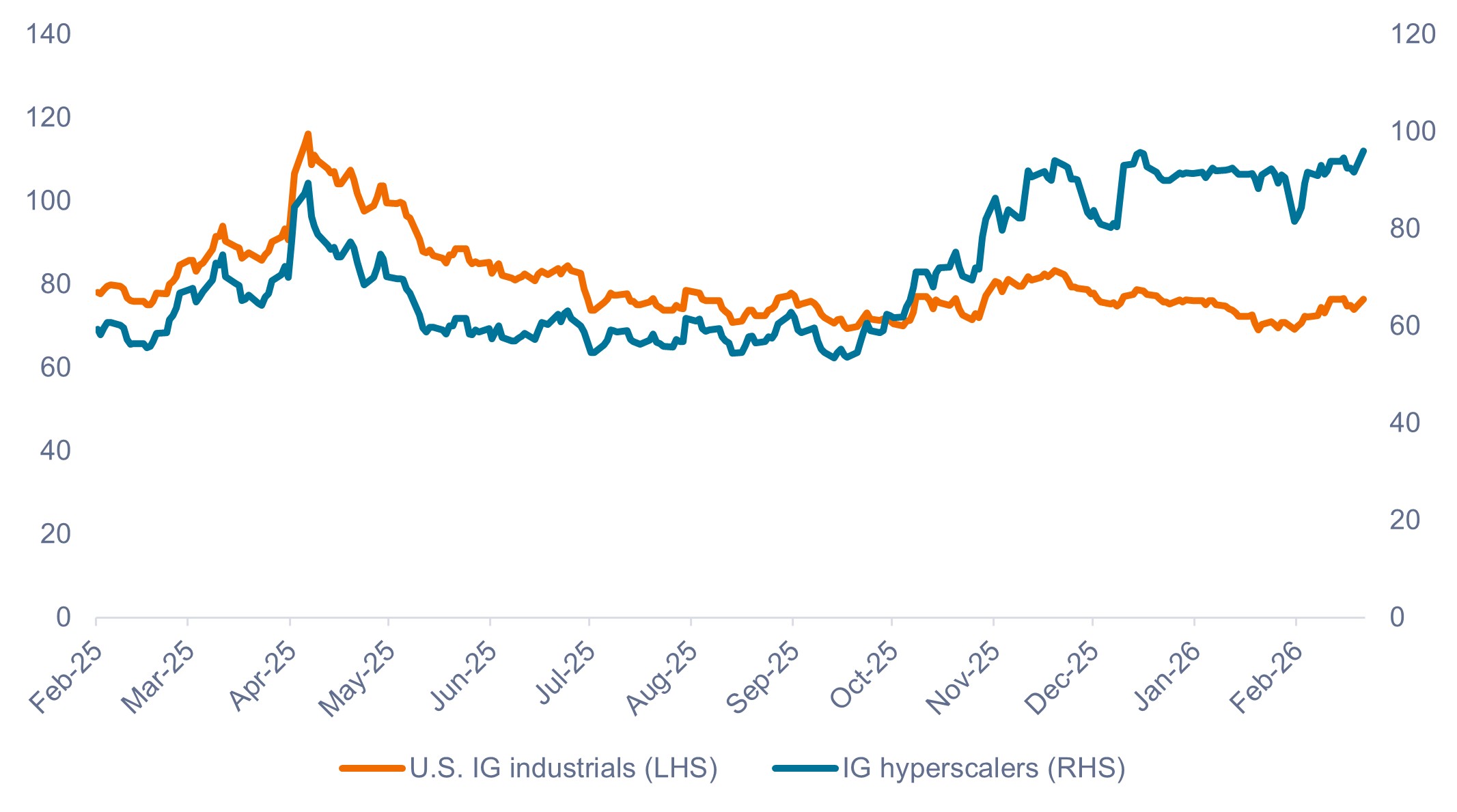

As shown in Exhibit 1, hyperscaler spreads remained tight (in our view, unsustainably so) relative to industrials for much of 2025, before starting to widen late in the year to reflect their ambitious CapEx plans.

Exhibit 1: Hyperscaler vs. IG industrials credit spreads (Feb 2025 – Feb 2026)

Hyperscaler spreads began to widen late in Q3 ’25 but might not yet fully reflect technical and fundamental risks.

Source: Bloomberg, Janus Henderson Investors, as of 23 February 2026.

Historical research shows that large CapEx cycles funded primarily with debt have tended to be followed by meaningful spread widening. Despite the recent widening, we believe the hyperscaler cohort remains historically expensive, as current spreads still reflect strong confidence in execution, leaving limited margin for error.

Essentially, we think spreads would need to move materially from current levels before hyperscaler valuations begin to look attractive.

2. High yield

The rapid buildout of AI infrastructure is expanding the opportunity set for high-yield credit, where technicals are far more constructive compared to IG corporates. The high yield market is less impacted by the massive amount of issuance from IG-rated hyperscalers, while interesting opportunities in ancillary industries are opening up, which we recently covered in detail.

Early beneficiaries within high yield have been power generators – particularly Independent Power Producers (IPPs) – given AI data centers’ surging energy needs and hyperscalers’ long-dated power contracts. (To put the power demand of AI chips and application in perspective, some estimates suggest that three New York City’s worth of power will be needed to sustain the grid by 2030.)

As power constraints intensify, opportunities have broadened to AI-linked data centers, including firms pivoting from Bitcoin mining to high performance computing (HPC), supported by innovative lease-backed financing structures that prioritize debt service.

A new class of AI native “neo cloud” operators further extends the investable universe, while upstream suppliers in memory and networking add cyclical and secular exposure.

Finally, while competitive alliances across chips, cloud, and software are reshaping the ecosystem and creating both opportunity and volatility, overall AI driven CapEx is expected to continue to support a growing range of high yield issuers across the data center supply chain.

We think valuations are also more attractive in the high yield segment. As an example, BB rated Terawulf Inc. emerged as the first Bitcoin miner to pivot toward HPC with a long term lease from Google and tap the high yield market for financing. Its 2030 bonds – which come with a lease backstop from Google – presently offer around 260 basis points (bps) of excess spread over U.S. Treasuries, while Google’s bonds of similar duration offer just 35 bps of spread over Treasuries.

3. Securitized credit – ABS and CMBS

In our view, some of the most attractive opportunities related to the data-center buildout exist within asset-backed securities (ABS) and commercial mortgage-backed securities (CMBS). That said, these deals also come with potentially higher risk and uncertainty, and it is therefore critically important to adopt an active, research-driven approach. The deal structures are very important, as is the technology behind the data center, where it’s located, who the tenants are, etc.

Technicals in the ABS and CMBS market look more attractive to us than in the IG corporate space. Combining ABS and CMBS, we expected $25 to $30 billion of new issuance a year. We think that’s easily digestible for a roughly $5 trillion (excluding agency MBS) securitized market.

We believe valuations on AI-linked bonds are also most attractive within securitized credit, potentially offering the highest upside. Indicatively, various BBB-rated CMBS and ABS deals currently offer over 300 bps in spread over Treasuries, whereas similarly rated prime auto ABS may trade in the 125 bps range. Essentially, one can get double the spread of some of the other fixed income asset classes with the same credit rating via securitized credit.

While Janus Henderson never relies on ratings to price risk and determine relative value, it does point to the disconnect between sectors in the securitized markets where our bottom-up, research-driven approach may discern opportunity.

Summary

Given IG corporate credit’s supply‑driven headwinds, particularly among the hyperscalers, we think spreads would need to move materially from current levels before hyperscaler valuations begin to look attractive. In contrast, high yield and securitized sectors may offer expanding AI‑linked opportunities with better technicals and more attractive valuations.

Importantly, the evolving fixed income landscape may come with potentially higher risk and uncertainty, necessitating, in our view, an active, research-driven approach backed by a strong team with extensive experience investing in corporate and securitized markets.

Janus Henderson’s model of collaboration and knowledge-sharing among fixed income, securitized, and equity research analysts may allow us to provide differentiated and well-informed insights.

1 The hyperscaler cohort is made up of Microsoft, Google, Meta, Amazon, and Oracle.

Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Excess return is the total return of a bond or portfolio minus a benchmark return (often a risk-free rate or duration-matched risk-free bond). It measures the performance above what is expected, representing the compensation for taking on additional credit, interest rate, or liquidity risk beyond the risk-free rate.

IMPORTANT INFORMATION

Actively managed portfolios may fail to produce the intended results. No investment strategy can ensure a profit or eliminate the risk of loss.

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield bonds, or “junk bonds,” are corporate debt securities with lower credit ratings (below BBB−/Baa3) that offer higher interest rates to compensate for a greater risk of default. They are issued by companies with lower creditworthiness or high debt levels. While riskier, they offer higher income potential and lower sensitivity to interest rate changes.

Investment-grade securities: A security typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments. The higher quality of these bonds is reflected in their higher credit ratings when compared with bonds thought to have a higher risk of default, such as high-yield bonds.

Securitized products, such as mortgage-backed securities and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Non vi è alcuna garanzia che le tendenze passate continuino o che le previsioni si realizzino.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Il Fondo investe in obbligazioni ad alto rendimento (non investment grade) che, sebbene offrano di norma un interesse superiore a quelle investment grade, sono più speculative e più sensibili a variazioni sfavorevoli delle condizioni di mercato.

- Alcune obbligazioni (obbligazioni callable) consentono ai loro emittenti il diritto di rimborsare anticipatamente il capitale o di estendere la scadenza. Gli emittenti possono esercitare tali diritti laddove li ritengano vantaggiosi e, di conseguenza, il valore del Fondo può esserne influenzato.

- Un Fondo che presenta un’esposizione elevata a un determinato paese o regione geografica comporta un livello maggiore di rischio rispetto a un Fondo più diversificato.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo può sostenere un livello di costi di operazione più elevato per effetto dell’investimento su mercati caratterizzati da una minore attività di contrattazione o meno sviluppati rispetto a un fondo che investa su mercati più attivi/sviluppati.

- Le spese correnti possono essere prelevate, in tutto o in parte, dal capitale, il che potrebbe erodere il capitale o ridurne il potenziale di crescita.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.

- Oltre al reddito, questa classe di azioni può distribuire plusvalenze di capitale realizzate e non realizzate e il capitale inizialmente investito. Sono dedotti dal capitale anche commissioni, oneri e spese. Entrambi i fattori possono comportare l’erosione del capitale e un potenziale ridotto di crescita del medesimo. Si richiama l’attenzione degli investitori anche sul fatto che le distribuzioni di tale natura possono essere trattate (e quindi imponibili) come reddito, secondo la legislazione fiscale locale.