Key takeaways:

- Markets are reacting to energy supply and shipping risks rather than geopolitical escalation. Oil prices are reflecting a temporary risk premium, with duration – not headlines – determining whether the shock becomes macro‑relevant for emerging markets (EMs).

- Sustained higher energy prices would increase differentiation across EMs, benefiting exporters while pressuring importers through weaker trade balances, inflation pass‑through and wider spreads. So far, market reactions remain orderly and contained.

- We are closely monitoring energy‑driven pressures, sovereign bond market responses and country‑level impacts, engaging actively with research providers and market participants to identify vulnerabilities should a persistent shock materialise.

As markets assess the conflict in the Middle East, the dominant transmission channel has not been geopolitical escalation itself, but the implications for energy flows. Oil prices moved sharply higher and commercial shipping through the Strait of Hormuz effectively stalled, driven by heightened security risks, tanker incidents, GPS interference and the withdrawal of insurance coverage. To date, markets are pricing in an energy risk premium, rather than a confirmed or permanent loss of supply, but the situation remains fluid.

Will it be short-lived?

Whether this is a short-lived geopolitical risk-shock, a structural shock to oil prices or somewhere in between is key as it will determine the impact on the global economy and the resultant winners and losers.

Other channels, including inflation dynamics and potential US Federal Reserve (Fed) interest rate repricing, are secondary and become relevant only if energy prices remain elevated for a sustained period.

In practical terms, markets will be driven by oil prices and their persistence over time, with clear implications for EM winners and losers:

- Short-term: Oil price volatility is the dominant driver. Short‑lived geopolitical shocks historically have little real economic effect, and markets can absorb temporary energy spikes. Near‑term price action is therefore likely to reflect risk premia and positioning rather than a fundamental reassessment of growth.

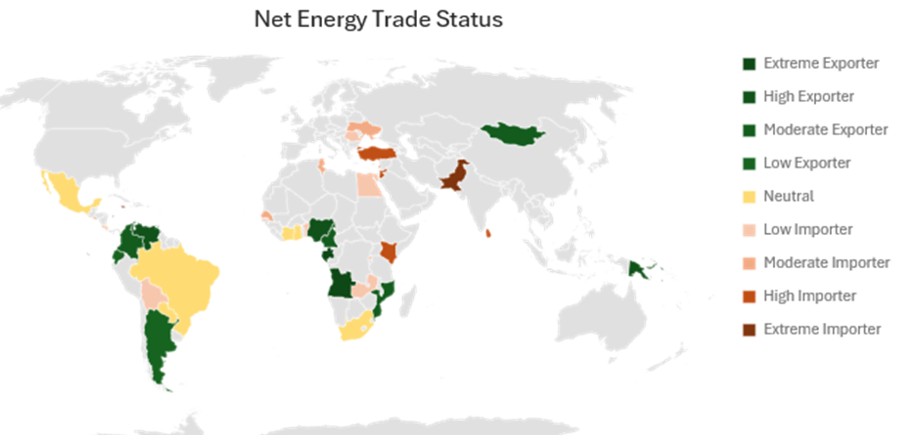

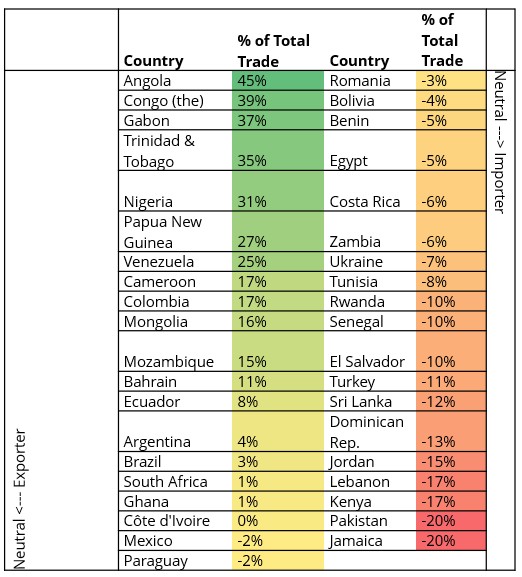

- Medium-term: If elevated oil prices persist, differentiation across EM becomes more pronounced. Oil exporters benefit, while energy‑importing sovereigns face pressure through weaker trade balances (as reflected in their net energy trade positions in Figure 1 and 2), inflation pass‑through and wider sovereign bond spreads.

- Long term: A sustained period of high energy prices would materially alter the global macroeconomic outlook, feeding into inflation expectations, central‑bank policy re-pricing (including the Fed), and broader financial conditions.

In short, duration matters more than headlines. The longer energy prices remain elevated, the more macro‑relevant the shock becomes, and the more differentiation we expect to see within EM.

Figure 1: Emerging market oil/energy sensitivity

Source: Australian Bureau of Statistics, GeoNames, Microsfot, Navinto, Open Places, OpenstreetMap, Overture Maps Foundation, TomTom, Zenrin, as at 2 March 2026.

Figure 2: Net energy trade as a % of total trade

Source: Stifel, 2 March 2026.

Near‑term outcomes hinge on energy and shipping stabilisation

This remains a developing situation, and near‑term outcomes will depend on how quickly energy markets and shipping conditions normalise. We are actively engaging with internal and external research providers, market participants and regional specialists to assess market sentiment, evolving risks and country‑level implications. Our focus is on understanding where energy‑driven pressures are most acute, how sovereign bond markets are responding, and how various EM countries are impacted. So far, the market reaction has been very orderly, with only a modest spread widening and muted safe-haven behaviour.

Sovereign: Typically refers to debt issued by a national government. Sovereign bonds are backed by the country’s creditworthiness and ability to repay.

Emerging market investments have historically been subject to significant gains and/or losses. As such, returns may be subject to volatility.

Sovereign debt securities are subject to the additional risk that, under some political, diplomatic, social or economic circumstances, some developing countries that issue lower quality debt securities may be unable or unwilling to make principal or interest payments as they come due.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Credit spread: The difference in yield between securities with similar maturity but different credit quality, often used to describe the difference in yield between corporate bonds and government bonds. Widening spreads generally indicate a deteriorating creditworthiness of corporate borrowers, while narrowing indicates improving.

Financial Conditions: Financial conditions describe the overall ease or tightness with which households, businesses and governments can obtain funding in the economy.

Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures; the opposite of deflation.

Interest rates: The amount charged for borrowing money, shown as a percentage of the amount owed. Base interest rates (the Bank Rate) are generally set by central banks, such as the Federal Reserve in the US or Bank of England in the UK, and influence the interest rates that lenders charge to access their own lending or saving.

Net energy trade position: The net energy trade position represents the difference between a country’s or region’s total energy exports and total energy imports, indicating whether they are a net exporter (positive) or a net importer (negative).

Risk premium: The additional return an investment is expected to provide in excess of the risk-free rate. The riskier an asset is deemed to be, the higher its risk premium to compensate investors for the additional risk.

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Non vi è alcuna garanzia che le tendenze passate continuino o che le previsioni si realizzino.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe. Le obbligazioni ad alto rendimento (non investment grade) sono più speculative e sensibili ai cambiamenti avversi delle condizioni di mercato.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Alcune obbligazioni (obbligazioni callable) consentono ai loro emittenti il diritto di rimborsare anticipatamente il capitale o di estendere la scadenza. Gli emittenti possono esercitare tali diritti laddove li ritengano vantaggiosi e, di conseguenza, il valore del Fondo può esserne influenzato.

- I mercati emergenti espongono il Fondo a una volatilità più elevata e a un maggior rischio di perdite rispetto ai mercati sviluppati; sono sensibili a eventi politici ed economici negativi e possono essere meno ben regolamentati e prevedere procedure di custodia e regolamento meno solide.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo può sostenere un livello di costi di operazione più elevato per effetto dell’investimento su mercati caratterizzati da una minore attività di contrattazione o meno sviluppati rispetto a un fondo che investa su mercati più attivi/sviluppati.

- Le spese correnti possono essere prelevate, in tutto o in parte, dal capitale, il che potrebbe erodere il capitale o ridurne il potenziale di crescita.

- I CoCo (Obbligazioni contingent convertible) possono subire brusche riduzioni di valore in caso d’indebolimento della solidità finanziaria di un emittente e qualora un evento trigger prefissato comporti la conversione delle obbligazioni in azioni dell’emittente o il loro storno parziale o totale.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.