Key takeaways:

- Delivering what we characterize as a “pre-emptive” cut, the Fed prioritized supporting a flagging labor market despite elevated inflation.

- Should the Fed’s view that tariffs represent a “one-off” to price levels prove inaccurate, December’s cut, along with any in 2026, could lead to persistent inflation exerting upward pressure on the long end of yield curves.

- In periods of elevated uncertainty, we believe bond investors should prioritize diversification and steady yields – two characteristics that can potentially be achieved by seeking out shorter-dated, global issuance.

Bond investors who were looking to unearth clear insight on the future state of the U.S. economy and policy rate path likely viewed the Federal Reserve’s (Fed) December statement as something of a nonevent. We found some value in it as – after a slight misdirection by Chairman Jerome Powell in his October comments – the central bank’s ensuing efforts to telegraph perhaps a final pre-emptive 25 basis point (bps) cut served as evidence of the Fed’s adherence to forward guidance.

One could argue that for a data-driven Fed, the notion of being pre-emptive is something of a contradiction, as the decision seemed to be made with an eye toward what might transpire over the next 12 months. Not helping matters was the dearth of recent economic data due to the recently resolved government shutdown. Furthermore, language referencing that risks on each side of the Fed’s dual mandate (price stability and full employment) are both present could have been grounds to wait and see – an approach taken by the two hawkish dissenters. But in the end, nine other voters concluded that a third successive rate cut was the most prudent course.

Tension within the data

For Chairman Powell, the rationale for favoring labor over prices could be found in tariffs. Data reveal that persistent inflation over much of 2025 is owed to an acceleration in goods prices. The Fed is pinning its hopes on the assumption that tariffs will be a one-time resetting of price levels and once that flows through, year-over-year inflation will again start to drift back toward the central bank’s 2.0% target.

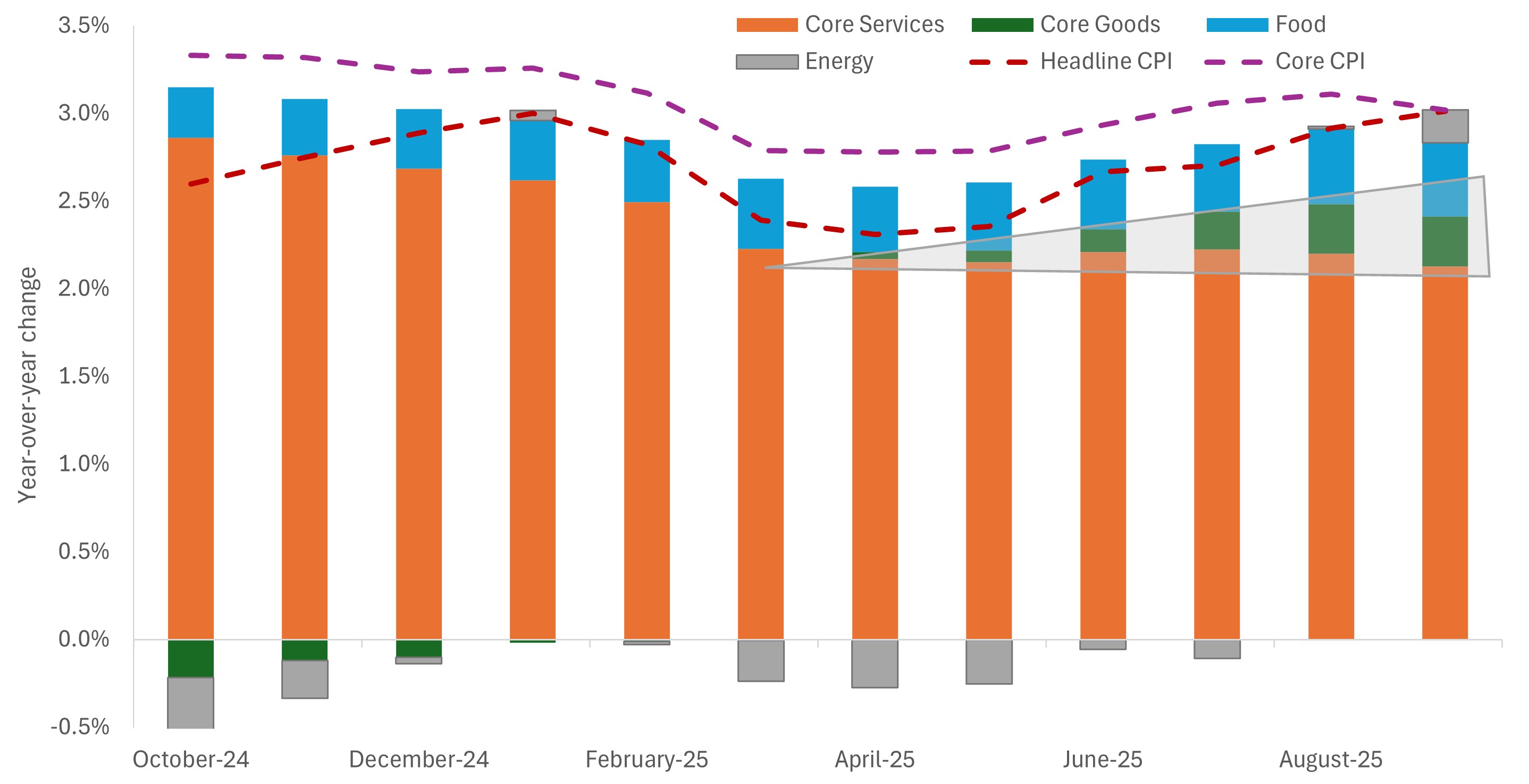

Exhibit 1: Components of U.S. consumer price index

Persistent headline – and core – inflation are largely attributable to a rise in goods prices which is denting positive trends in core services and, more recently, energy prices.

Source: Bloomberg, Janus Henderson Investors, as of 30 September 2025.

The Fed’s expectation that the upside risk to inflation may prove ephemeral allowed it to prioritize what it views as relatively worrying labor market trends. The unemployment rate ticked up three-tenths of one percent, to 4.4%, between June and September – the last available month. Similarly, average payroll gains have dipped to stall speed, averaging 39,000 over the last five available months. Even with an absence of October and November data – along with the administration’s immigration policy clouding labor market supply and demand dynamics – the mid-year softness proved sufficient for the Fed to act.

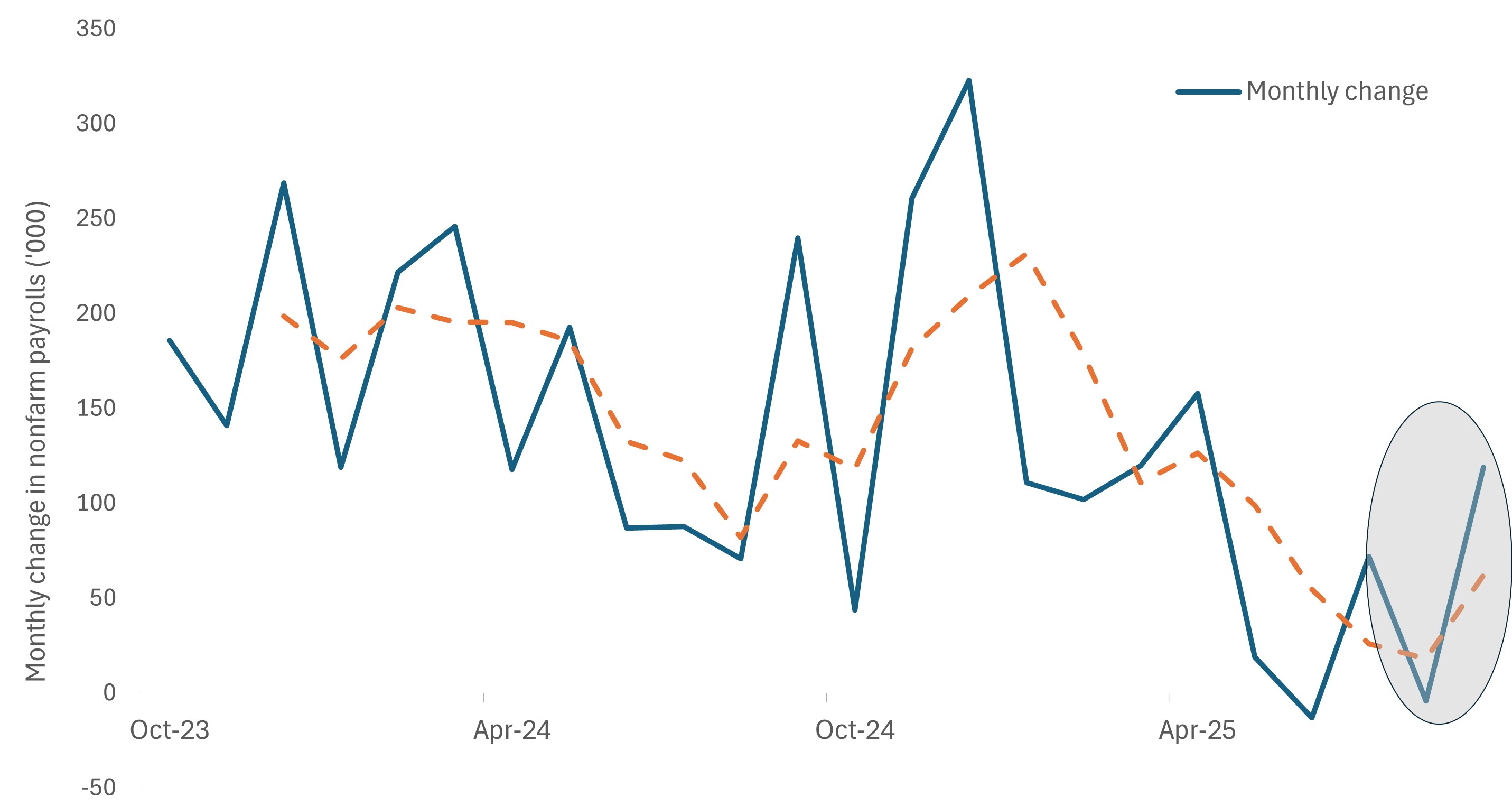

Exhibit 2: U.S. nonfarm payroll changes

The nonfarm payrolls data through September reflected a similar softening trend seen in private labor market data and this was likely enough to compel the Fed to tilt its bias toward supporting job growth.

Source: Janus Henderson Investors, as of 30 September 2025.

The tension within the Fed’s mandate is further illuminated by the central bank’s updated Summary of Economic Projections. Even when factoring out the effects of the government shutdown, 2026 economic growth has been modestly revised upward. Reflecting the Fed’s sanguine view toward tariffs, both headline and core inflation for next year were modestly revised downward to 2.4% and 2.5%, respectively. Interestingly, even with plodding economic growth and the recent uptick, the unemployment rate is expected to finish 2026 at 4.4% – unchanged from its September projection.

The greatest evidence that the December decision can be characterized as a hawkish cut is the Fed’s own projected interest rate path being unchanged from October. The median estimate of surveyed members indicates one cut each in 2026 and 2027. Futures markets are more dovish, pricing in two 25 bps cuts next year. That view, however, could reflect the expected shift in the Fed’s composition, with the end of Chairman Powell’s tenure and the appointment of a new Chair who could more closely reflect President Trump’s attitude toward monetary policy. We must state that the Chair represents just one vote, and the presumption is that most members greatly respect the value placed on Fed independence.

Uncertainty merits diversification – and steady yield

The Fed itself admitted that it’s in the unenviable position of operating in an environment where both inflation and the labor market command their attention. Bond investors find themselves in the same predicament. We are aligned with the consensus view that future rate hikes are off the table. After this meeting, status quo means possibly only two more rate cuts this cycle. Should that prove to be too hawkish, economic growth could surprise to the downside, resulting in declining mid- to longer-dated Treasury yields.

Of course, the risk is that if a still-resilient consumer sector rolls over, following an already flagging housing market, cyclically exposed corporate credits could suffer. We see this as a low probability scenario but one that should not be completely ignored given current tight credit spreads.

A wild-card scenario is a potentially more-pliable Fed cutting rates more than anticipated, especially given that inflation is still residing above the bank’s 2.0% target. Tariffs’ impact on prices not proving transitory would compound the upward pressure on prices. That policy error, while likely not on the scale of the 1970s, in our view, would punish mid- to longer-dated bonds.

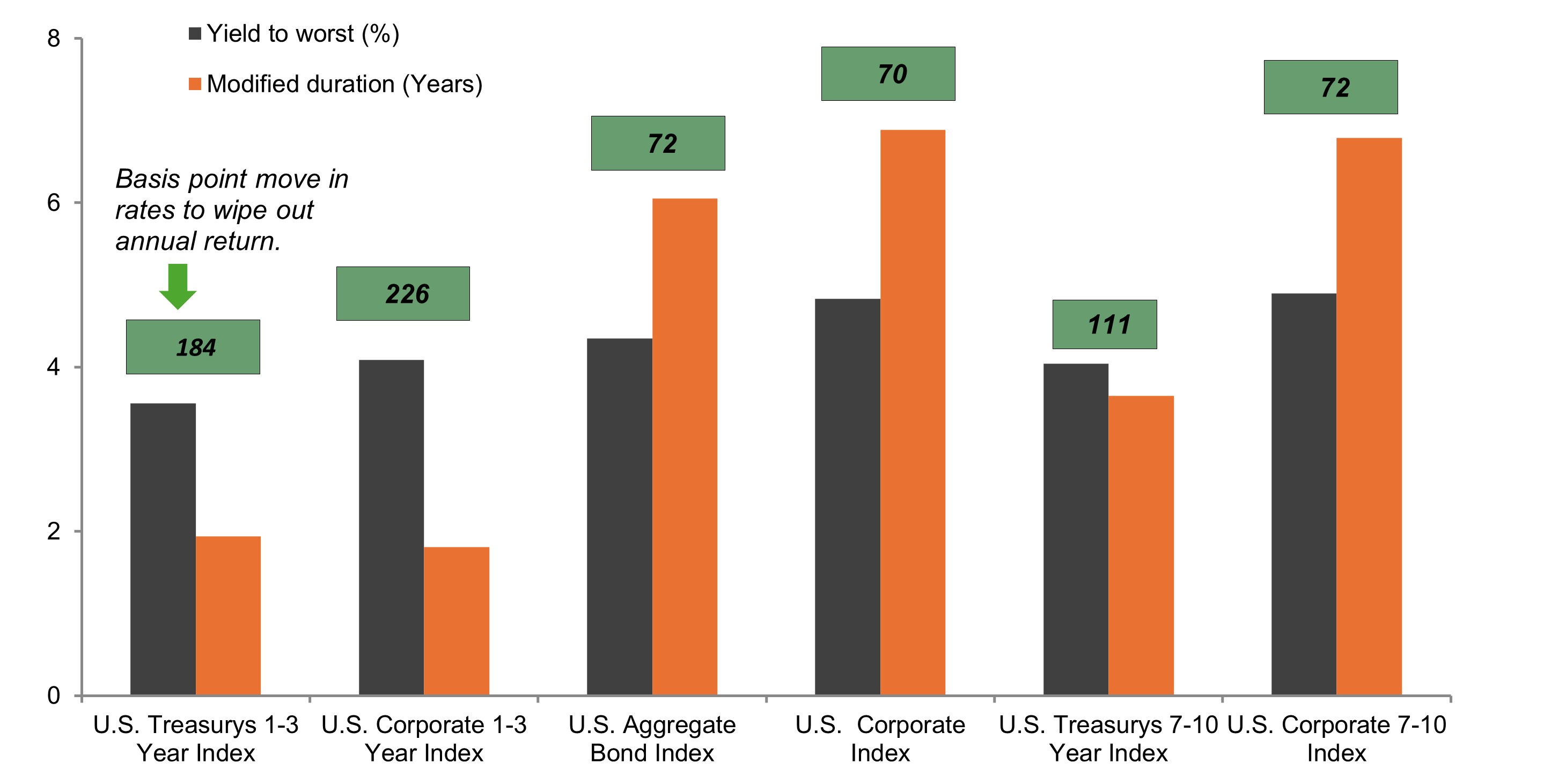

Exhibit 3: U.S. bond segments yield and duration exposure

After years of policy distortions upending the traditional relationship, shorter-dated securities again generate yields sufficient to absorb any potential upside interest rate risk; this characteristic is welcome in a period of inflation and rate uncertainty.

Source: Bloomberg, as of 10 December 2025.

As we argued in our Market GPS 2026 outlook, periods of economic and policy uncertainty don’t lend themselves well to excessive risk taking. With yields on the front end of sovereign and credit curves still attractive – albeit beneath recent highs – we believe fixed income investors can still generate attractive income streams via shorter-maturity issuance that is less exposed to interest rate volatility.

Lastly, we think uncertainty should force bond investors to prioritize diversification. An effective way to accomplish that in the current environment, in our view, is to allocate across jurisdictions. Economic cycles and policy prescriptions are diverging, enabling investors to capture income in regions with still high – and stable – rates while also participating in capital appreciation in countries where conditions merit a resumption of easing.

IMPORTANT INFORMATION

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

Bloomberg US Corporate Bond Index measures the investment grade, fixed rate, taxable corporate bond market.

The Bloomberg US Treasury 1-3 Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with 1-2.999 years to maturity.

The Bloomberg US Corporate 1-3 Year Index measures the investment grade, fixed-rate, taxable corporate bond market with 1-3 year maturities.

The Bloomberg US Treasury 7-10 Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with 7-10 years to maturity.

The Bloomberg US Corporate 7-10 Year Index measures the investment grade, fixed-rate, taxable corporate bond market with 7-10 year maturities.

Bloomberg U.S. Aggregate Bond Index is a broad-based measure of the investment grade, US dollar-denominated, fixed-rate taxable bond market.

Basis point: One basis point (bp) equals 1/100 of a percentage point, 1bp = 0.01%.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Duration: Duration measures the sensitivity of a bond’s or fixed income portfolio’s price to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Monetary policy: The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. Monetary policy tools include setting interest rates and controlling the supply of money.

Quantitative Easing (QE) is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market

Volatility measures risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

Yield-to-worst: The lowest yield a bond with a special feature (such as a call option) can achieve provided the issuer does not default.

Yield curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Non vi è alcuna garanzia che le tendenze passate continuino o che le previsioni si realizzino.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Alcune obbligazioni (obbligazioni callable) consentono ai loro emittenti il diritto di rimborsare anticipatamente il capitale o di estendere la scadenza. Gli emittenti possono esercitare tali diritti laddove li ritengano vantaggiosi e, di conseguenza, il valore del Fondo può esserne influenzato.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Qualora il Fondo detenga attività in valute diverse da quella di base del Fondo o l'investitore detenga azioni o quote in un'altra valuta (a meno che non siano "coperte"), il valore dell'investimento potrebbe subire le oscillazioni del tasso di cambio.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.

Specific risks

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Il Fondo investe in obbligazioni ad alto rendimento (non investment grade) che, sebbene offrano di norma un interesse superiore a quelle investment grade, sono più speculative e più sensibili a variazioni sfavorevoli delle condizioni di mercato.

- Alcune obbligazioni (obbligazioni callable) consentono ai loro emittenti il diritto di rimborsare anticipatamente il capitale o di estendere la scadenza. Gli emittenti possono esercitare tali diritti laddove li ritengano vantaggiosi e, di conseguenza, il valore del Fondo può esserne influenzato.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Qualora il Fondo detenga attività in valute diverse da quella di base del Fondo o l'investitore detenga azioni o quote in un'altra valuta (a meno che non siano "coperte"), il valore dell'investimento potrebbe subire le oscillazioni del tasso di cambio.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.

- Oltre al reddito, questa classe di azioni può distribuire plusvalenze di capitale realizzate e non realizzate e il capitale inizialmente investito. Sono dedotti dal capitale anche commissioni, oneri e spese. Entrambi i fattori possono comportare l’erosione del capitale e un potenziale ridotto di crescita del medesimo. Si richiama l’attenzione degli investitori anche sul fatto che le distribuzioni di tale natura possono essere trattate (e quindi imponibili) come reddito, secondo la legislazione fiscale locale.