焦点分析

- 利率市场目前处于两难境地:一方面是高油价和人工智能(AI)相关资本支出带来的通胀压力,另一方面是美伊可能达成协议带来的局势缓解前景。

- 公司信贷息差处于低位,但支撑这一局面的基本面和技术性因素依然稳固:企业盈利表现强劲,投资者配置需求旺盛,新增供给已得到市场有效吸纳。

- 证券化资产可提供额外且多元化的收益来源,有助于投资者在单位风险下实现收益最大化。

展望2026年时,很少有人预料到以色列/美国与伊朗之间会爆发战争。因此,我们在年度展望中提出的“寻求韧性”建议被证明是极具先见之明的。2026年上半年固定收益市场面临的挑战,主要反映了利率预期的转变。市场日益担忧,中东油气供应中断导致能源价格上涨,最终可能传导至更广泛的通胀。

利率主导,信贷次之

全球经济运行驳斥了悲观论者的预言,但地缘政治紧张局势却体现在利率波动上。主权债券收益率上升,反映了货币政策的重新调整:降息预期普遍转为观望,部分情况下甚至转为加息。新的财政担忧也推高了收益率,在多数发达市场,长期债券收益率突破了近年来的高点。

鉴于美联储利率政策前景仍不明朗,而其他主要央行的政策倾向偏鹰派,我们对久期风险保持谨慎。通胀担忧上升,不仅是因为中东冲突的影响,也因为各国经济表现出强于预期的韧性。与此同时,在预期的生产力提升实现之前,事实证明人工智能(AI)相关的支出在初期具有通胀效应(例如芯片和内存成本上升)。

尽管如此,收益率的回升和利率的波动也可能带来一些战术性机遇。只要中东供应中断对通胀产生的二阶效应得到控制,战争的解决可能会促使收益率下行。这在很大程度上取决于霍尔木兹海峡的航运中断会持续多久。这种不明朗的利率前景可能有利于许多证券化资产的浮动利率结构。

主权债券收益率的上行带动了公司债券收益率上升,从而削弱了回报率。然而,全球经济表现出了显著的韧性。消费保持稳健(通常与调查中显示的悲观情绪相反),劳动力市场也未见颓势。

信贷息差(同期限公司债相较于国债的额外收益率,通常被视为企业健康状况的晴雨表)经历了一轮“先扩后收”的循环。息差在冲突初期有所扩大,但此后已回落至接近年初水平,即处于20年来的历史低位附近。唯一的例外是低质量债券(CCC级),其息差处于平均水平左右,这表明市场正在区分信用状况较好和较差的借款人。

图表1:全球信贷息差经历了一个完整的轮回(基点)

| Investment grade | High yield | ||||||

| AAA | AA | 中国 | BBB | BB | B | CCC | |

| 一月 | 36 | 47 | 63 | 92 | 185 | 336 | 992 |

| 二月 | 45 | 55 | 73 | 103 | 199 | 361 | 1,055 |

| 三月 | 44 | 60 | 79 | 112 | 227 | 399 | 1,117 |

| 四月 | 40 | 53 | 70 | 100 | 190 | 337 | 1,021 |

| 五月 | 36 | 50 | 65 | 93 | 182 | 325 | 1,035 |

| 2026年5月31日息差相对于过去20年的百分位排名 | |||||||

| 3% | 6% | 1% | 1% | 1% | 8% | 52% | |

资料来源:彭博,截至2026年5月31日的月末数据。相对于国债的选择权调整息差(以基点计)。1个基点 = 0.01%,100个基点 = 1%。投资级 = 特定信用评级的ICE BofA全球公司债指数。高收益 = 特定信用评级的ICE BofA全球高收益债指数。百分位排名1%意味着信贷息差接近20年来的最低点,100%意味着处于最高点,50%意味着处于过去20年区间的中间位置。过往业绩并不预示未来回报。

虽然息差相对于过去20年可能较低,但整体收益率仍具吸引力,因为同期国债收益率正处于最高水平附近。尽管息差收窄,但整体收益率仍吸引了追求收益的投资者。归根结底,息差随经济周期波动,而今年以来,几乎没有迹象表明经济增长会出现重大减速。中东冲突的滞后影响可能会在未来几个月显现,因此投资者应保持警惕,但我们认为,过度谨慎可能会带来机会成本。

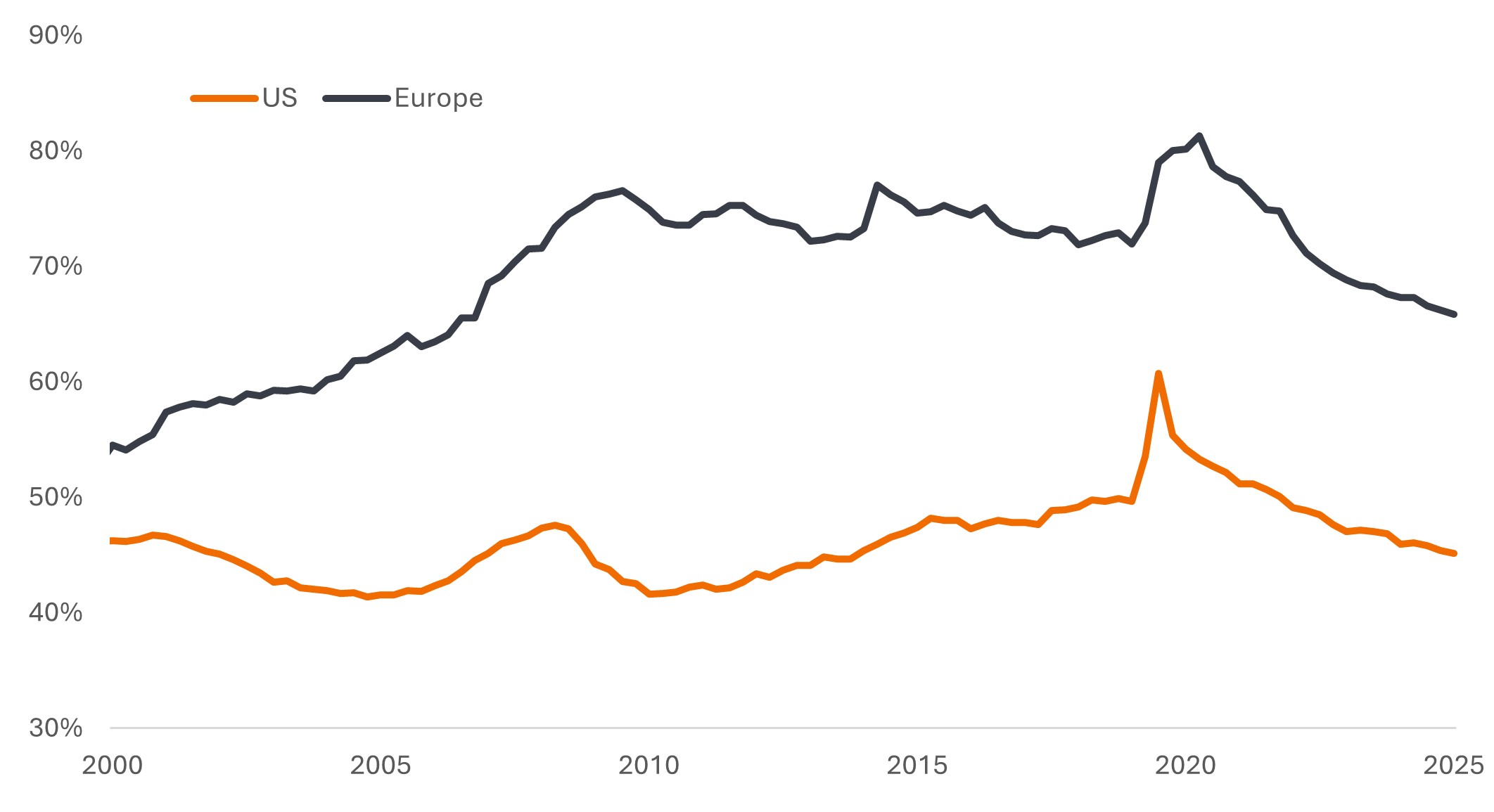

强劲的盈利改善了市场情绪。2026年第一季度,标普500®指数的同比盈利增长率为28.6%,是自2021年第四季度以来的最快增速(当年的数据因疫情后的反弹而出现了正向扭曲)。1虽然有人认为市场可能过于乐观,但近年来息差收窄的趋势源于强劲的基本面。企业杠杆率近期一直在下降,而且这不仅仅是美国市场的现象。

图表2:企业杠杆率持续下降

非金融企业债务证券及贷款占国内生产总值(GDP)的百分比

资料来源:美国:美联储经济数据库(FRED),欧洲:欧洲央行,欧元区20国。2000年第四季度至2025年第四季度。 GDP = 国内生产总值,是衡量经济规模的指标,代表一个国家或地区在特定时期(通常为每季度或每年)内生产的所有最终产品和服务的价值。

再结合强劲的家庭资产负债表、许多国家的低失业率、直到近期能源价格飙升前一直在增长的实际工资,以及美国的减税政策,息差收窄就变得更容易解释了。

供给创造自身需求

考虑到“超大规模云服务提供商”(hyperscalers)为投资AI而大量发行债券,这种企业杠杆率下降的观点似乎有些矛盾。预计仅今年一年,超大规模云服务提供商的资本支出就将达到约8,000亿美元。22026年,市场可能需要消化约2,400亿美元与AI相关的债券发行。3尽管绝大多数债券是由一些信用质量最高的借款人发行的(其中许多企业几乎没有净负债),但庞大的新发规模可能会考验投资者的胃口,并对公司债息差造成压力。AI建设带来的机遇也出现在证券化领域,尤其是基础设施资产支持证券(ABS)。

对于其他借款人而言,可能会出现“挤出效应”,导致2026年下半年息差出现小幅扩大。与此相对的是,借贷和支出有助于推动经济中其他领域的收入增长。市场面临的一个关键风险是,如果超大规模云服务提供商缩减支出计划,这可能会削弱市场的乐观情绪,并对风险资产造成损害。

我们目前正处于AI发展的探索阶段。没人能确定其全部成本和收益,但它已经是一项有助于推动经济增长的变革性技术。对AI取代现有商业模式的担忧已导致软件行业面临压力,这转而给部分私募信贷市场带来了挑战——更多是与限制赎回相关的负面消息,而非系统性问题。另一方面则是所谓的HALO(重资产、低淘汰率)公司,如电网、大宗商品和制造业,这些行业被认为基本上不会受到被取代的威胁。

收益来源的多样化

我们注意到,股市的持续强劲表现已营造出一种亢奋情绪。股市回调的可能性正在增加:如果霍尔木兹海峡封锁带来的滞后效应不能尽快解决,可能会通过增长疲软或通胀上升而显现弊端;美联储可能会发出转向加息的信号;此外,沉重的股市IPO排期(通常是市场见顶的预兆)可能会引发市场“消化不良”。

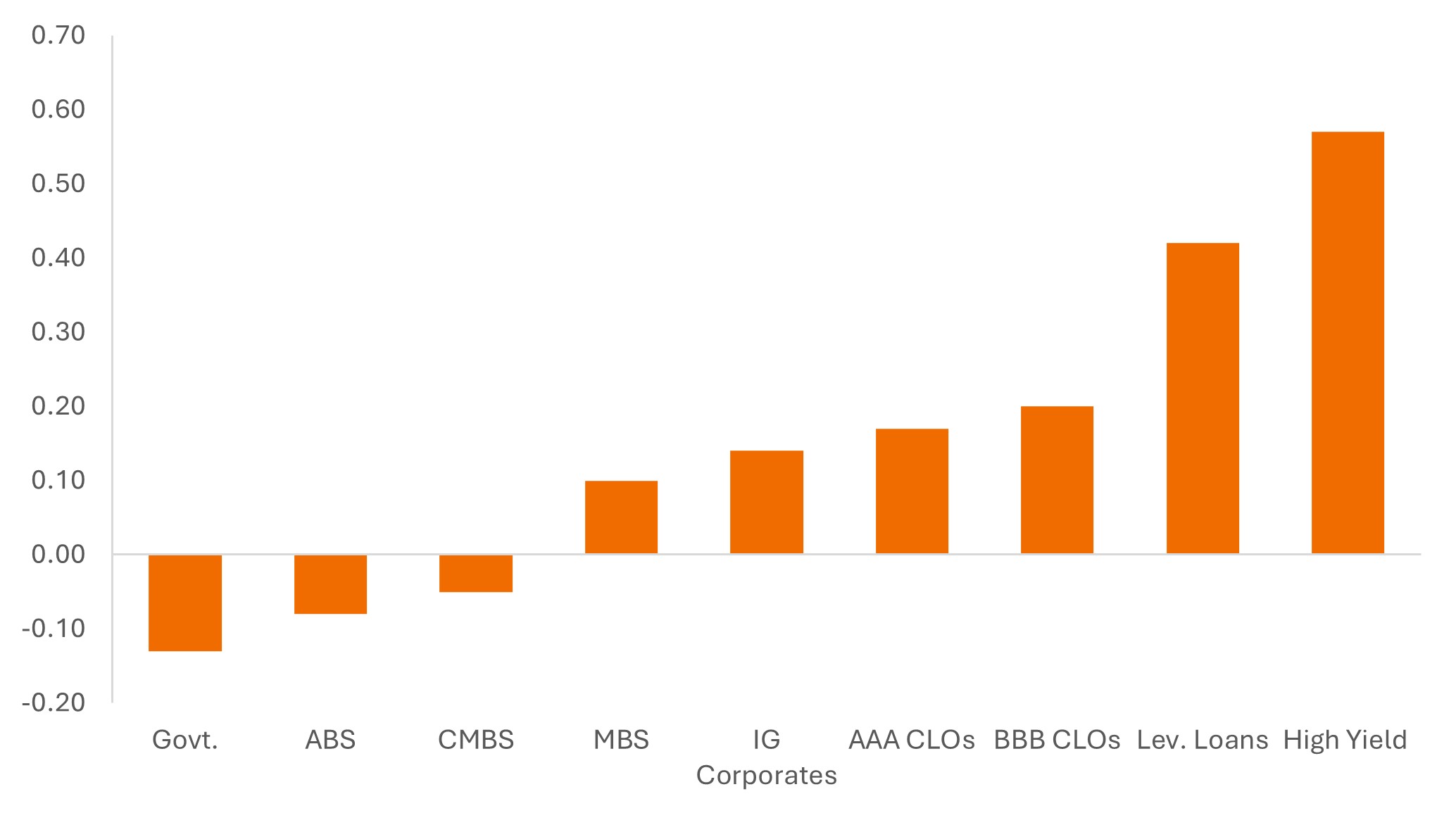

考虑固定收益中哪些领域与股市的相关性较低可能是有益的。毕竟,除了收益之外,固定收益资产类别通常被视为投资组合的多元化工具。高收益债券对企业经营状况敏感,与股市的相关性最为紧密。国债通常具有负相关性,因为当宏观环境走弱时,它们的表现通常优于大盘。

ABS和商业抵押贷款支持证券等证券化资产与股市的相关性较低,甚至是负相关。某种程度上,这是因为它们往往会对特定或差异化的周期(住房供应、旅游、零售消费、租赁市场等)做出反应,而且证券化指数的信用质量通常高于公司债。

图表3:各资产类别与标普500®指数的相关性(2016年至2026年)

资料来源:彭博、摩根大通、骏利亨德森投资,截至2026年5月31日。截至2026年5月31日的10年间每日相关性。代表资产类别的指数:政府债券= 彭博美国国债指数;ABS = 彭博美国综合资产支持证券指数;CMBS = 彭博美国投资级商业抵押贷款支持证券指数;MBS = 彭博美国抵押贷款支持证券指数;投资级公司债 = 彭博美国投资级公司债券指数;AAA及BBB级CLO= 摩根大通CLO指数;杠杆贷款 = 晨星LSTA杠杆贷款指数;高收益 = 彭博美国高收益债券指数。过往业绩并不预示未来回报。

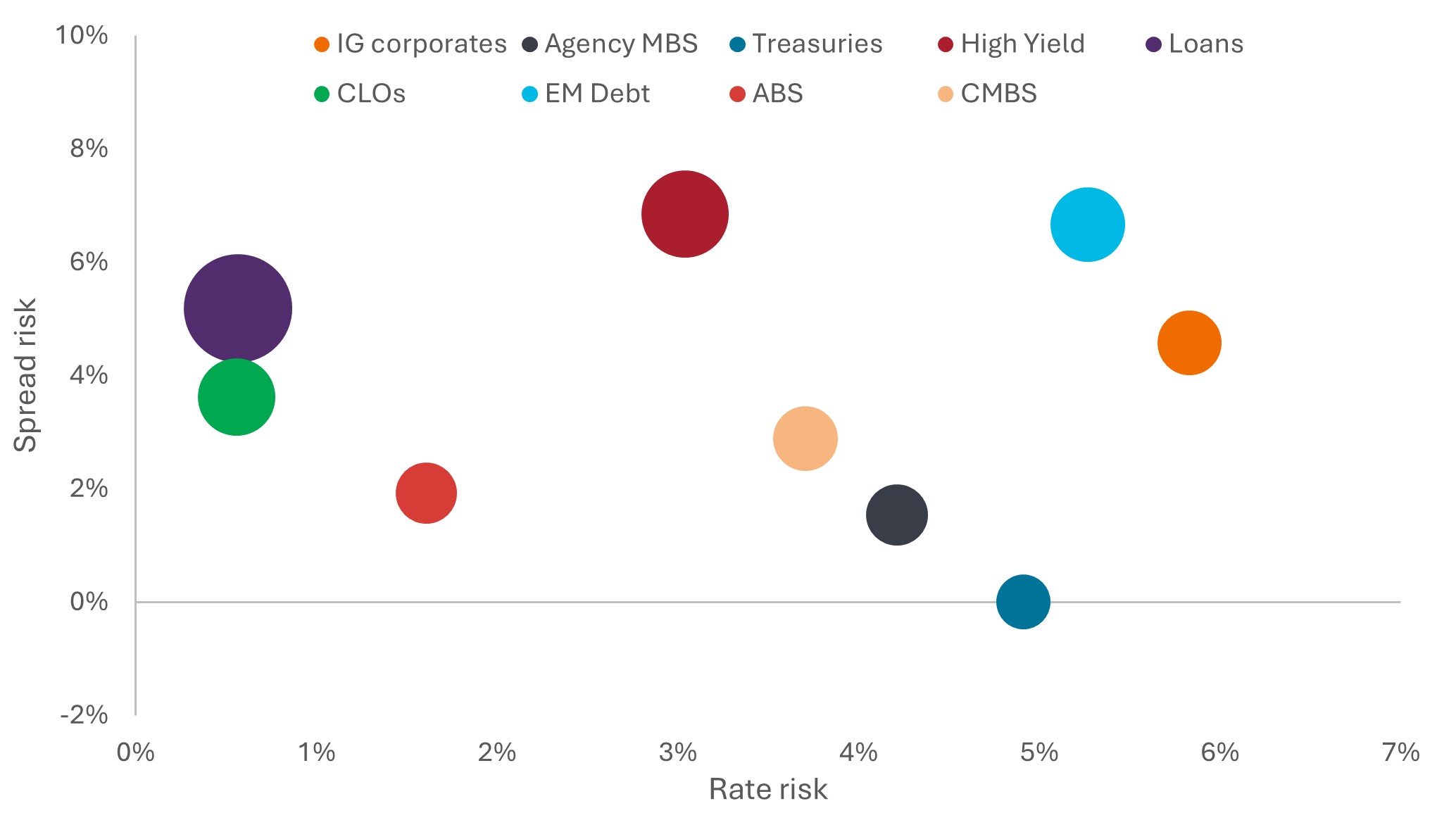

鉴于市场前景不明,广泛的固定收益子资产类别为投资组合构建提供了一个实用的工具箱。图表4显示了不同资产类别受两种不同因素影响的波动性:利率风险(与利率变化相关的波动)和息差风险(与借款人偿债信心变化相关的波动)。寻求降低利率变化敏感度的投资者,可能会持有更多具有浮动利率结构的贷款或贷款抵押债券(CLO)。

另一端,投资级公司债券可能对降息的反应最为积极。担心增长前景的投资者可以通过持有国债或机构抵押贷款支持证券(MBS)来限制息差(信贷)风险。相反,在经济增长具有韧性的环境下,高收益债和新兴市场债务可能更具潜力。

混合资产类别或采用对冲策略可以帮助投资者实现预期的风险状况和结果。我们早前注意到公司债券息差已接近历史低点。但证券化资产并非如此,其息差以及收益率仍处于相对有吸引力的水平,使投资者能够在单位风险下实现收益最大化。图表4中的圆圈宽度代表2026年5月31日的平均收益率规模(例如,美国国债收益率为4.3%,美国贷款收益率为8.6%)。

图表4:固定收益领域包含广泛板块,可通过组合实现更佳的风险调整后收益

资料来源:彭博、摩根大通、骏利亨德森投资,截至2026年5月31日。利率风险和息差风险基于截至2026年5月31日止10年期间的利率和息差波动。圆圈大小代表收益率。代表各资产类别的指数:投资级公司债 = 彭博美国投资级公司债券指数;机构MBS = 彭博美国抵押贷款支持证券指数;美国国债 = 彭博美国国债指数;高收益 = 彭博美国高收益债券指数;贷款 = 摩根大通杠杆贷款指数;贷款抵押证券 = 摩根大通贷款抵押证券指数;新兴市场债务 = 彭博新兴市场美元主权及准主权指数;ABS = ICE BofA美国固定及浮动利率资产支持证券指数;CMBS = ICE BofA美国固定利率商业抵押贷款支持证券指数。 过往业绩并不预示未来回报。

我们一段时间以来一直认为,投资者应跳出传统固定收益领域的狭隘范畴,把握整个资产类别广度所带来的机遇和多元化潜力。

2026年上半年给投资者带来了不少意外挑战。但通过辩证审视,洞悉本质,我们可以理解市场为何会有特定表现,并客观地在投资组合中寻求机遇和对冲风险。

倘若英文版本与中文版出现歧异,概以英文版为准。

1资料来源:FactSet,2026年第一季度标普500指数同比盈利增长。截至2026年5月29日,500家成分股公司中已有97%公布了2026年第一季度业绩。

2资料来源:摩根士丹利估计,2026 年 5 月 12 日。恕不保证过往趋势将会延续,或者预测将会实现。3资料来源:巴克莱估计,2026 年 5 月 21日。恕不保证过往趋势将会延续,或者预测将会实现。

Bloomberg EM USD Sovereign + Quasi-Sov Index measures the performance of fixed and floating rate US dollar denominated debt issued by emerging market governments (sovereign) and government-owned or guaranteed entities (quasi sovereign).

Bloomberg US Aggregate Asset-Backed Securities Index tracks investment grade fixed rate, taxable US dollar denominated asset-backed securities.

Bloomberg US CMBS Investment Grade Index measures the performance of US Agency and non-Agency commercial mortgage-backed securities (CMBS).

Bloomberg US Corporate (Investment Grade) Bond Index measures the investment grade, fixed rate, taxable corporate bond market.

彭博美国高收益企业债券指数量度以美国计价的高收益定息企业债券市场。

Bloomberg US Mortgage Backed Securities (MBS) Index tracks fixed rate agency mortgage backed pass-through securities guaranteed by Ginnie Mae, Fannie Mae and Freddie Mac.

Bloomberg US Treasury Index measures US dollar-denominated, fixed rate, nominal debt issued by the US Treasury.

ICE BofA AAA US Fixed Rate CMBS Index tracks the performance of US dollar denominated investment grade AAA rated fixed rate commercial mortgage backed securities publicly issued in the US domestic market.

ICE BofA Global Corporate Index tracks the performance of investment grade corporate debt publicly issued in the major domestic and Eurobond markets.

ICE BofA Global High Yield Index tracks the performance of USD, CAD, GBP and EUR denominated below investment grade corporate debt publicly issues in the major domestic or Eurobond markets.

ICE BofA US Fixed & Floating Rate Asset Backed Securities Index tracks the performance of US dollar-denominated investment grade asset backed securities publicly issued in the US domestic market.

ICE BofA US Corporate Bond Index tracks the performance of US dollar-denominated investment grade debt publicly issued in the US domestic market.

ICE BofA US Fixed Rate CMBS Index tracks the performance of US dollar denominated investment grade fixed rate commercial mortgage backed securities publicly issued in the US domestic market.

J.P. Morgan Collateralised Loan Obligation Index tracks the performance of broadly syndicated arbitrage US dollar-denominated debt.

J.P. Morgan Leveraged Loan Index measures the investable universe of the USD institutional leveraged loan market.

晨星LSTA美国杠杆贷款指数是一项市值加权指数,旨在衡量美国杠杆贷款市场的表现。

Agency Mortgage-backed Securities (Agency MBS): A type of asset-backed security that is specifically secured by a collection of mortgages. These securities are issued by one of the three government-sponsored enterprises (GSEs): Fannie Mae (Federal National Mortgage Association), Freddie Mac (Federal Home Loan Mortgage Corporation), or Ginnie Mae (Government National Mortgage Association).

Asset-backed Securities (ABS): These are financial instruments that are backed by a pool of assets—typically those that generate a cash flow from debt, such as loans, leases, credit card balances, or receivables.

资产负债表:通常指实体的资产与负债相关的会计参考,无论是家庭还是企业。

Basis point: One basis point (bp) equals 1/100 of a percentage point, 1bp = 0.01%.

资本支出(CapEx):企业为支持业务增长和扩张而推动新项目或投资时,用于重大长期资产支出的资金,此类资产包括不动产和设备(有形资产)或技术、软件、商标、专利等(无形资产)。

Collateral: In a securitisation, collateral refers to the pool of financial assets that are bundled together to form the basis of a security.

贷款抵押证券(CLO)是指不同批次发行的债务证券,风险程度各异,主要以低于投资级别的企业贷款组成的相关投资组合作为抵押。本金回报不获保证,若未能及时支付款项或信贷状况恶化,价格可能下跌。贷款抵押证券须承受流动性风险、利率风险、信贷风险、赎回风险及相关资产违约风险。

Commercial Mortgage-backed Securities (CMBS): A type of mortgage-backed security that is secured by the loan on commercial real estate properties rather than residential real estate.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

相关性 衡量两个变数在变动时的相互关联程度。数值1.0意味同步变动,-1.0表示沿相反方向变动,而0.0表示无相关性。

Credit cycle: The changing availability and pricing of credit that is linked to economic expansion and contraction. It is seen as having four distinct phases: downturn, repair, recovery, and expansion. Borrowing and spending is expansionary and helps sustain economic growth but when lenders restrict lending this can lead to a downturn and businesses and households have to repair their finances until the economy moves back into recovery and expansion.

Credit rating: A score given by a credit rating agency such as S&P Global Ratings, Moody’s and Fitch on the creditworthiness of a borrower. For example, S&P ranks investment grade bonds from the highest AAA down to BBB and high yields bonds from BB through B down to CCC in terms of declining quality and greater risk, i.e. CCC rated borrowers carry a greater risk of default.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

违约:债务人(例如债券发行人)未能在到期时支付利息或归还原始贷款金额。

Duration: Duration measures the sensitivity of a bond’s or fixed income portfolio’s price to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

多元化投资╱分散投资:透过在投资组合中配置不同类型资产/资产类别以分散风险的方法,基于不同资产在任何特定情况下的表现各异。

Fundamentals: In the context of corporate debt, “fundamentals” refer to the essential financial health indicators and characteristics of a company that suggest its ability to meet debt obligations.

财政政策:描述由政府厘定税率和开支水平的政策。

财政政策(Fiscal policy):描述政府厘定税率和开支水平的政策。财政纪律是指政府不会过度借贷,即维持借贷占经济产出的百分比于偏低水平,以免整体债务负担大幅增加。

对冲:一种交易策略,涉及对另一项投资采取抵消头寸。当主要投资获利时,该头寸会贬值,反之亦然。此类头寸用于降低或管理各类风险因素,并限制投资组合整体亏损的概率。

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

超大规模云服务提供商:指提供可动态扩展的信息技术架构、以应对指数级增长的工作负载与数据的技术供应商。除容量外,这些企业还提供企业级云服务、弹性硬件资源和稳定可靠的软件环境,以支撑各类人工智能应用的运行。

Inflation: The rate at which prices of goods and services are rising in the economy.

IPO或首次公开募股:指私人公司首次在证券交易所向公众出售其股份。

Investment grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

发行(Issuance):借贷(发行)公司向投资者发行债券的行为,通常是透过向公众或金融机构出售债券。

杠杆:公司的借贷水平,通常指债务除以盈利。它也可用于描述占经济比例的企业债务水平或公司的资产负债表状况。

Maturity: The maturity date of a bond is the date when the principal investment (and any final coupon) is paid to investors. Shorter-dated bonds generally mature within 5 years, medium-term bonds within 5 to 10 years, and longer-dated bonds after 10+ years.

货币政策(Monetary policy):旨在影响经济的通胀及增长水平的央行政策。货币政策工具包括厘定利率及控制货币供应。

Private credit: An asset defined by non-bank lending where the debt is not issued or traded on the public markets.

Securitisation: The process in which certain types of assets are pooled so that they can be repackaged into interest-bearing securities. The interest and principal payments from the assets are passed through to the purchasers of the securities.

主权债券/政府债券:政府为偿还债务或为支出融资而发行的债券。它们通常以一个国家的征税能力和/或印钞能力作为支撑。

美国国债/美国政府证券:由美国政府发行的债务凭证。国库券和美国政府债券由美国政府的完全信誉作为担保。它们通常被认为没有信用风险,且收益率通常低于其他证券。

Volatility measures risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate.

Yield-to-worst: The lowest yield a bond with a special feature (such as a call option) can achieve provided the issuer does not default.

重要资讯

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

固定收益证券面临利率风险、通胀风险、信用风险和违约风险。 债券市场具有波动性。随着利率上升,债券价格通常会下跌,反之亦然。不保证可退还本金,如果发行人未能及时还款或信用实力减弱,价格可能会下跌。

高收益债券或“垃圾债券” 涉及更高的违约风险和价格波动性,并可能出现突然且剧烈的价格波动。

按揭及资产抵押证券等证券化产品对利率变化较为敏感,牵涉续期及提前还款风险,信贷、估值及流动性风险高于其他固定收益证券。

Yields may vary and are not guaranteed.