Key takeaways:

- Market returns have been dominated by a narrow group of large-cap stocks, increasing concentration and limiting diversification.

- As market leadership broadens in a period of greater geopolitical uncertainty, smaller companies are responding more quickly to improvements in sentiment, highlighting a shift away from the narrow dominance of mega-cap stocks.

- Global smaller companies are under-owned and under-researched, offering greater potential for bottom-up stock pickers to identify mispriced stocks and earlier-stage higher-growth opportunities.

Markets started 2026 on an uncertain footing, pulled in different directions by geopolitical instability. The conflict in the Middle East, which began at the end of February, brought energy markets back into stark focus. Blocked supplies through the Strait of Hormuz pushed oil prices higher and raised fresh concerns about inflation just as central banks were attempting to stabilise growth.

For investors, this has created a challenging mix of risks and uncertainties. Risk appetite has weakened as attention has become fixed on the conflict and its implications. Meanwhile, expectations for fiscal and monetary policies have shifted. Higher energy prices have complicated the outlook for interest rates. The uncertainty of government policy announcements via social has led to rapid swings in sentiment. The path to a lasting resolution remains obscured.

Despite this backdrop, one notable feature of recent market behaviour has been the resilience of global smaller companies. This is typically the part of the market that struggles when uncertainty is elevated and policy is restrictive. In our view, this reflects modest starting valuations, positive earnings expectations, and a gradual shift in how investors are approaching markets. But even periods of tentative improvement in sentiment have seen investors look beyond the most heavily owned areas, suggesting that attention is no longer as narrowly focused as it once was.

A turning point for market concentration

Over the past decade, market returns have been dominated by a small group of large-cap technology companies (ie. the ‘Magnificent 7’ – Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia and Tesla). At the same time, higher interest rates, macro uncertainty, and a preference for liquidity has favoured larger, more resilient businesses. Combined with passive flows, this has created an increasingly concentrated market, turning investor allocations into a tacit call on technology stocks.

What appears to be changing is not a sudden reversal but a gradual broadening of leadership. The focus is shifting from owning what has worked to reassessing where future returns may come from. It has been driven by a subtle change in behaviour, with investors showing greater sensitivity to valuation, a more questioning approach to crowded trades, and growing awareness of how concentrated portfolios have become, particularly at a time of heightened geopolitical uncertainty.

The dominance of the largest companies has not disappeared, but it is no longer unquestioned. Artificial intelligence remains a powerful structural theme, yet investors are starting to look beyond the most obvious beneficiaries, to smaller companies exposed to adjacent areas of growth.

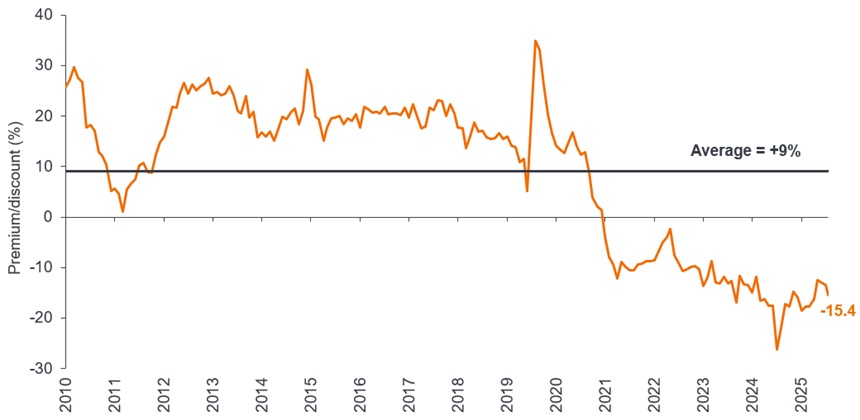

At the same time, the earnings picture for smaller companies is improving. Combined with more modest starting valuations relative to global large caps (Exhibit 1), we believe it supports the conditions for a re-rating, even in an uneven market.

Exhibit 1: Attractive valuations of global small caps relative to large caps

Source: Bloomberg, Janus Henderson Investors Analysis, as at 9 April 2026. Shows global small cap premium/discount versus global large caps (forward P/Es).

Note: Indices used: MSCI World Small Cap, MSCI World. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

Different regions, different strengths

Much like their larger counterparts, global smaller companies provide exposure to a diverse set of local economies and sector opportunities. Unlike large multinationals, however, they tend to be more closely tied to domestic or regional growth, which can be an advantage in a more fragmented geopolitical environment. They also tend to be more entrepreneurial and agile, often driving advances within specialised niches, rather than at scale.

Another defining feature is how little attention they receive. Smaller companies are typically under-owned and under-researched, with materially less coverage from stock analysts. A combination of less scrutiny and more varied outcomes creates opportunity for active investors taking a selective approach. Particularly so, given how strong earnings forecasts are for smaller companies relative to their large-cap peers[1].

But there are also important differences across regions, offering built-in diversification within the small-cap category. In the US, deep capital markets and a strong culture of innovation support a broad pipeline of companies across technology, healthcare, and specialised industrials. In Europe, the market is more weighted towards industrials, manufacturing, and niche export-led businesses. Many of these have strong technical expertise and pricing power, alongside tailwinds from defence and infrastructure spending.

Japan offers another distinct profile, characterised by high-quality industrial and technology businesses. Improving corporate governance and a greater focus on shareholder returns are helping to unlock value in companies that have historically been overlooked.

Market inefficiency equals opportunity for active investors

Global smaller companies remain one of the few areas of genuine inefficiency in equity markets. Limited analyst coverage and the diversity of the opportunity set mean there is real scope to add value through detailed research and engagement.

This increases the value of information in the small cap space, given that outcomes in smaller companies are driven more by stock-level factors than by broad market movements. Sector and stock dispersion is wide, meaning the gap between winners and losers can be significant. This makes a research-led, data-driven approach essential, with a focus on characteristics such as return on equity, balance sheet strength, and the sustainability of earnings.

For investors willing to take a longer-term view, this part of the market offers exposure to businesses earlier in their growth journey. After all, many of today’s dominant companies, such as Nvidia, began as small caps. This is not to overlook the risks; smaller companies can be more volatile and more sensitive to economic cycles. Navigating these risks requires a disciplined, structured approach to stock selection.

Overall, we believe that global smaller companies continue to offer a compelling opportunity set. In a market long dominated by a narrow group of large-cap stocks, they provide diversification, exposure to innovation, and access to domestic growth trends across regions. The macro environment remains uncertain. However, for investors focused on fundamentals, the breadth of opportunities within global smaller companies remains significant.

—–

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

[1] Source: Bloomberg, Janus Henderson Investors, as at 9 April 2026. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

Active investing: An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis, and the investment choices they make.

Asset allocation: The allocation of a portfolio between different asset classes, sectors, geographical regions, or types of security to meet specific objectives of risk, performance, or time horizon.

Balance sheet: A financial statement that summarises a company’s assets, liabilities, and shareholders’ equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders.

Diversification: A way of spreading risk by mixing different types of assets or asset classes in a portfolio on the assumption that these assets will behave differently in any given scenario. Assets with low correlation should provide the most diversification.

Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures.

Interest rates: The amount charged for borrowing money, shown as a percentage of the amount owed. Base interest rates (the Bank Rate) are generally set by central banks, such as the Federal Reserve in the US or Bank of England in the UK, and influence the interest rates that lenders charge to access their own lending or saving.

Liquidity: A measure of how easily an asset can be bought or sold in the market. Assets that can be easily traded in the market in high volumes (without causing a major price move) are referred to as ‘liquid’.

Premium: When the market price of a security is thought to be more than its underlying value, it is said to be ‘trading at a premium’.

Return on equity (ROE): A company’s net income (income minus expenses and taxes) over a specified period, divided by the amount of money its shareholders have invested. It is used as a measurement of a company’s profitability compared to its peers. A higher ROE generally indicates that a management team is more efficient at generating a return from investment.

Returns/return: The total return of a portfolio over a specified period as opposed to its relative return against a benchmark. It is measured as a gain or a loss and stated as a percentage of a portfolio’s total value.