Key takeaways:

- The global market environment has become less predictable, with higher volatility, geopolitical uncertainty and shifting economic regimes driving frequent changes in leadership across regions and asset classes.

- Portfolios built around static allocations can struggle to keep up during periods of heightened volatility and shifting correlations, reducing both return potential and defensive qualities.

- A trend following allocation can improve portfolio flexibility and resilience by reducing reliance on traditional market relationships, utilising disciplined, rules based signals to rotate across assets to capture opportunities as leadership shifts.

Investor expectations often set the tone for markets, but 2025 served as a reminder that consensus is not certainty. Entering the year, confidence was high that US equities would again lead global performance, supported by a compelling narrative: a resilient domestic economy, strong corporate earnings, and continued enthusiasm for AI‑driven innovation. As 2025 unfolded, however, outcomes diverged sharply from expectations.

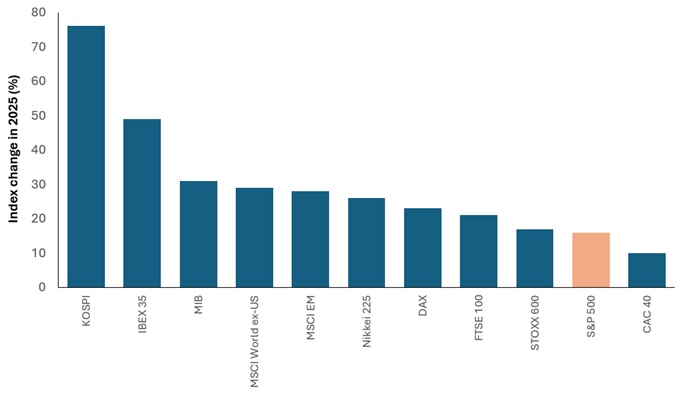

Despite a strong rally following the shock of ‘Liberation Day’ on 2 April, when US President Trump announced ‘reciprocal’ tariffs, US equities lagged almost all other major markets in 2025, both in local currency and US dollar terms (Exhibit 1).

Exhibit 1: Nearly all major global equity markets outperformed the US in 2025

Source: FactSet, Janus Henderson Investors, 1 January 2025 to 31 December 2025. Past performance does not predict future returns.

Note: Major indices – South Korea’s KOSPI Composite Index; Spain’s IBEX 35 Index; Italy’s FTSE MIB Index; Germany’s DAX Index; STOXX Europe 600 Index; MSCI All-Countries World ex-US Index; MSCI Emerging Markets Index, Japan’s Nikkei 225; UK’s FTSE 100 Index; US S&P 500 Index; France’s CAC 40 Index.

When the environment is shaped by political shocks, shifting capital flows, and rapid narrative rotation, strategies that rely on a static allocation between asset classes (eg. 60/40) can become a bet on yesterday’s regime. This raises a practical question for investors: how can portfolios remain resilient when leadership changes quickly and assumptions no longer hold?

There is always a market trending somewhere

Markets have exhibited trends throughout history, reflecting shifts in economic growth, inflation, policy, technology, and investor behaviour. While the timing, direction, and duration of trends are unpredictable, few markets remain static for long. Most experience sustained upward or downward movements at some point.

When equities or bonds are volatile or directionless, commodities may be trending. When commodities mean‑revert, currencies may see sustained moves, while regional dispersion can create clearer leadership elsewhere. Expanding the opportunity set increases the likelihood of identifying durable trends, even when headline markets appear unsettled.

This was evident in 2025. Europe and emerging markets attracted significant inflows. Precious metals such as gold and silver responded strongly to shifting real‑rate expectations, and currency markets reflected diverging growth and policy paths.

What drives trends in markets?

- Behavioural biases and slow diffusion of information: Anchoring, confirmation bias, herding and underreaction can delay price adjustment.

- Institutional capital constraints: It takes time for large capital flows to deploy or reallocate, particularly in markets with liquidity or regulatory limitations.

- Impact of price-insensitive trading: As trends build, price-insensitive investors begin to rebalance their exposure, eg. passive strategies, risk-parity entities, exchange-traded funds (ETFs).

- Macro regimes and cycles: Markets reflect slow-moving economic forces, such as business cycles, interest rate and inflation regimes, commodity supply dynamics, technological adoption and geopolitical changes.

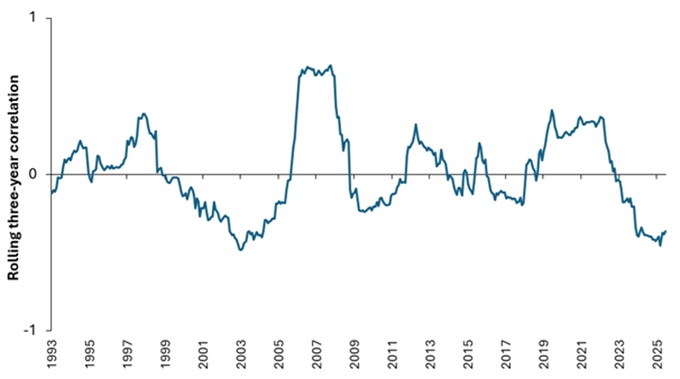

A strategy designed to identify and capture trends – wherever they emerge – can therefore remain relevant across changing market regimes. Trend-following strategies focus on observable price behaviour rather than forecasting which region, sector, or asset class will outperform next. They also seek to generate returns that are not dependent on a single market or outcome, displaying a history of low/variable correlation to equities and other traditional asset classes (Exhibit 2).

Exhibit 2: Trend-following strategies vs global equities (correlation)

Source: Bloomberg, BarclayHedge, Janus Henderson Investors, 31 January 1990 to 30 June 2025. Chart shows the rolling three-year correlation between the BTOP50 Index, an equally weighted trend-following index, and the MSCI World Index. Past performance does not predict future returns.

When equities or bonds are volatile or directionless, commodities may be trending. When commodities mean‑revert, currencies may begin to establish sustained moves, while regional dispersion can create clearer leadership elsewhere. Expanding the opportunity set increases the likelihood of identifying durable trends, even when headline markets appear unsettled.

This was evident in 2025. Europe and emerging markets attracted significant inflows. Precious metals such as gold and silver responded strongly to shifting real‑rate expectations, and currency markets reflected diverging growth and policy paths. Cash also played an important role – acting as a volatility buffer for some investors and as dry powder for others.

How does trend following work?

- Trend following is a systematic investment approach that seeks to capture sustained price movements across global financial markets. These strategies typically operate as multi‑asset portfolios, aligning exposure with prevailing momentum across equities, fixed income, commodities, rates, and currencies.

- Implementation is commonly achieved through futures contracts, which allow efficient access to markets, the use of leverage, and daily liquidity. Trend-following strategies aim to ‘ride’ market trends by increasing exposure to assets that are showing a directional trend, and reducing or reversing exposure during ‘trendless’ periods.

- Rather than forecasting economic outcomes, trend following relies on observable price behaviour, seeking diversification benefits and resilience across different market environments.

Trends are multi-dimensional

Shorter‑term trends can emerge around policy surprises, positioning shifts, or abrupt changes in risk appetite. Longer‑term trends tend to reflect structural forces such as deglobalisation, energy transition dynamics, demographic change, or sustained cycles of technological investment.

Good trend-following strategies think deeply about how to allocate, emphasising the importance of portfolio construction and risk management. In practice, trend signals can add exposure to risk assets in rising markets, while reinforcing themes through cyclical commodities or pro‑growth currencies. During falling or trendless markets, exposure can be reduced, shorted, or redirected towards assets perceived as more defensive, such as the US dollar, Treasuries or gold.

In this way, trend-following strategies offer a systematic framework for navigating uncertainty, with the potential to generate performance in both up markets and down.

Key benefits of a trend-following strategy:

- Adaptability, diversification, and potential downside resilience: By responding to observable price behaviour, trend following can participate in sustained market rallies while reducing or reversing exposure during prolonged declines.

- Differentiated drivers of performance: Because the opportunity set spans multiple asset classes, trend-following strategies are not dependent on the performance of any single market to generate returns. This has historically resulted in low correlation to both equities and bonds, particularly during periods of market stress.

- Asymmetric return profile: Trend strategies typically seek to limit losses when trends reverse while allowing gains to compound during extended moves, contrasting with the negatively skewed return profile often associated with equities.

Trend is your friend… if you blend

Today’s markets are characterised by higher volatility, unstable inflationary pressures, persistently higher interest rates and increased geopolitical risk. These conditions have challenged the diversification benefits between equities and bonds that have underpinned portfolio construction since the latter part of the 20th Century.

In practice, trend following can help address some of the structural limitations of traditional multi‑asset portfolios, such as the widely used 60/40 equity-bond allocation.

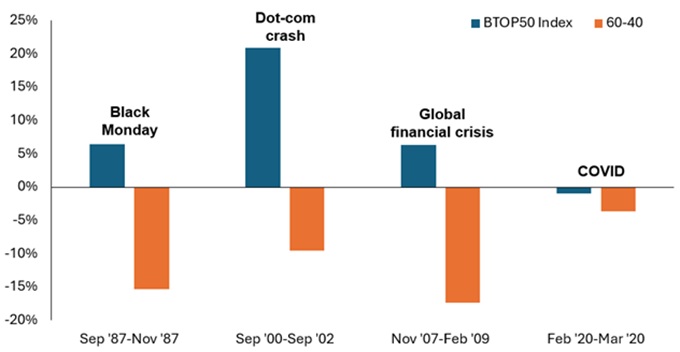

History indicates that trend-following strategies exhibit valuable defensive characteristics. During episodes such as the Dot‑Com collapse of 2000–2002 and the onset of the Global Financial Crisis in 2008, these strategies demonstrated notable resilience.

Exhibit 3: Trend following offers diversification benefits during crises

Source: Bloomberg, Janus Henderson Investors, 31 January 1987 to 28 February 2026. Chart shows monthly returns during periods of notable market distress, comparing the Barclay BTOP50 Index, a widely used, equal-weighted trend-following benchmark that measures the performance of the top 20 largest managed futures funds, with a simple 60/40 strategy allocated 60% to the S&P500 Index and 40% to the Bloomberg US Treasury 7-10 Year Index. Past performance does not predict future returns.

Following trends, not narratives

As markets move through 2026 and beyond, we expect leadership to remain susceptible to rapid shifts – not only within equities, but across asset classes and regions. Liquid, systematic trend‑following strategies, operating across assets and within a long/short framework, offer a way to respond to these evolving conditions.

Trend following is also a fraction of the market cap of single stocks like Apple or NVIDIA, making it an area with huge growth potential, given how little exposure many investors have to this segment of the market.

Crucially, trends are not confined to rising markets. They can emerge during periods of stress, transition, or consolidation, and across multiple time horizons. For investors seeking greater resilience in an uncertain world, the ability to adapt systematically as conditions change is arguably a very valuable attribute for any portfolio to have.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.