Fixed Income

Global active fixed income platform: Architects of fixed income solutions

Why Janus Henderson for active fixed income investing?

Janus Henderson’s global active fixed income platform delivers innovative strategies designed to help clients achieve consistent income and risk-adjusted returns.

Our experienced investment professionals combine rigorous research, advanced analytics, and decades of market expertise to build diversified fixed income solutions that seek to outperform benchmarks.

Guided by perspective. Driven by innovation.

Research-driven perspective

Research-driven perspective

Rigorous fundamental analysis, deep experience, and advanced quantitative tools provide perspective to generate high-conviction ideas and identify relative value.

Client-focused innovation

Client-focused innovation

From pioneering securitized strategies to advancing active fixed income ETFs, innovation is core to our approach.

Foundation of expertise

Foundation of expertise

A platform built on the foundation of more than 40 years of delivering fixed income strategies for our clients.

Our Fixed Income platform

A trusted partner

More than 450 institutional clients across 20 countries invest with us, benefitting from our shared insights and dialogue.

135

Fixed income investment professionals

19

Average years' experience

As at Jun 30, 2026

Fixed Income

Actively managed funds across fixed income asset classes.

Name

About this product

Aiming to access the total return potential of high yield bonds through a portfolio of diversified issuers, sectors and geography.

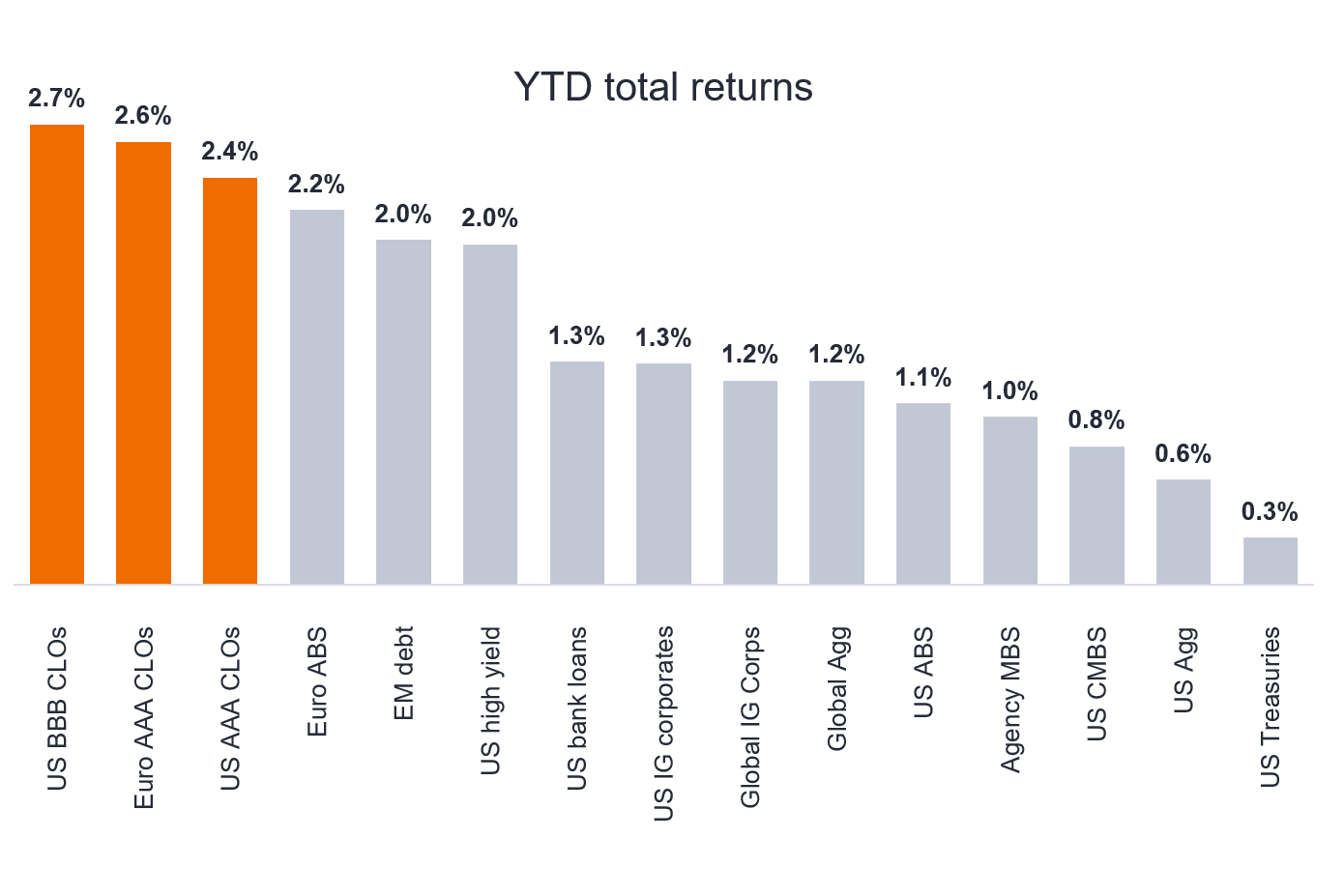

Providing exposure to high-quality, floating rate collateralised loan obligations (CLOs), which are designed to offer diversification benefits and low volatility with low downgrade risk.

Seeking to capture market inefficiencies within emerging markets debt to generate alpha over the long-term.

A fundamentally driven approach seeking to take advantage of situations where market pricing has become misaligned with economic and investment fundamentals.

Connect with our team to explore what's possible

Unlock the full potential of your financial future by speaking with our dedicated professionals today. Let us guide you through tailored solutions and opportunities driven by your goals and our expertise.