Key takeaways:

- The benefits accruing from stable trade arrangements, the peace dividend for governments, companies and consumers and historically low cost of capital are behind us.

- It’s possible to remain well invested but important to have a strong defensive bias and utilise cheap insurance.

- Navigating markets priced for perfection in a less perfect world demands considerable thought and preparedness.

Investors are fast becoming attuned to growing risks stemming from several sources including, but not limited to, geopolitical uncertainty, cracks in private credit markets and potential displacement caused by Artificial Intelligence (AI).

Priced for perfection

It is well understood that the steady state market environment investors had become accustomed to over some four decades leading up to the pandemic is firmly in the rear-view mirror. This included the ‘peace dividend’ for governments, companies, and consumers from relative geopolitical stability, falling cost of capital, well established global trade arrangements, and cost-effective reliable energy systems. Several market cycles have presented within this environment.

Market valuations meanwhile commenced 2026 with near-perfect pricing buoyed by ‘relative’ geopolitical stability, economic resilience post evolving newer trade arrangements and the excitement of productivity enhancing AI technology. A combination of robust fundamentals, favourable technicals with growing capital provision by confident investors within both public and private segments, banking systems and supportive regulatory and government settings further promoted strong performance.

Several asset classes experienced new peaks in recent valuations albeit dispersion became more apparent. Specifically for fixed income, bond markets were further supported by expectations of easing by the Fed, multi-decade tight credit spreads and ample liquidity from public and private markets.

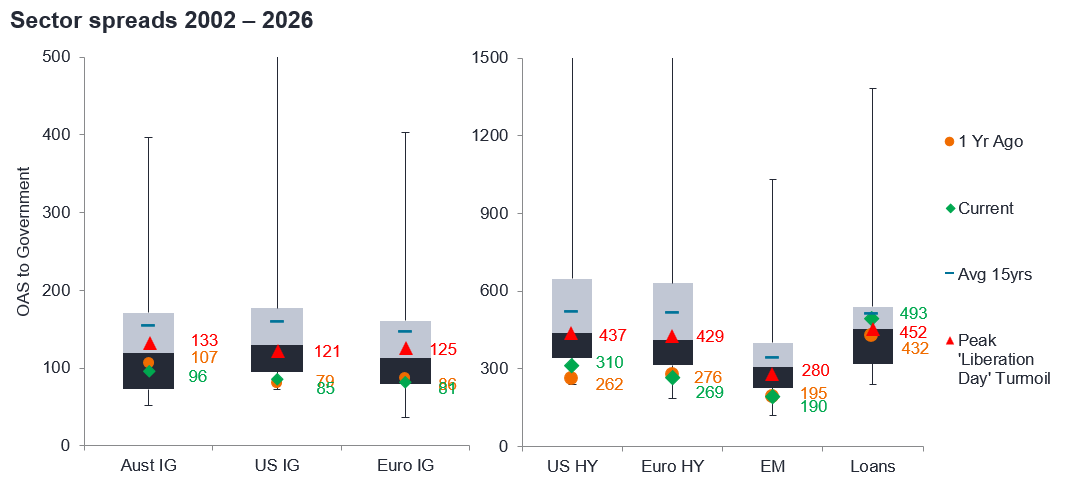

Global Credit

Australian IG starting point provides investors better cushioning.

Source: ICE BofAML Indices. Australian Corporate index: AUC0, US Corporate Master index: C0A0, US High Yield Master II: H0A0, Euro High Yield Fund Constrained: HE0C, Global High Yield Constrained: HW0C, JPMorgan Corporate Emerging Market Broad Diversified: CEMBI Broad.(inception date 31/12/2001).

Note: Box-Whisker: Spreads relative to 20th and 80th percentiles, as well as high and low end of the date range (31 December 2001 through 27 February 2026), 1 Year ago = 18 February 2025, Peak Liberation Day Turmoil = 9 April 2025.

Assessing credit valuations globally, barring a couple of areas such as Australian investment grade credit and loans, credit sectors are trading at multi-decade tight valuations.

Vulnerabilities being underappreciated

Observing today’s markets within the context of longer-term history, an appreciation of economic and business cycles and the inevitable left field risks that present from time to time, market participants today appear to underappreciate the need for risk compensation. Complacency is most evident not just in risk pricing but observable ultra-low levels of volatility and by extension cheap portfolio insurance.

Vulnerabilities are fast becoming evident in several areas including businesses not built for changing circumstances (be they trade, migration, higher cost of capital, augmented consumer demand, or the advent of AI). This coupled with less visible and sometimes indiscriminate lending to these real-world businesses through opaque financing structures and simple mispricing of risk potentially sets the scene for the perfect storm.

Recent high-profile examples of failures in this cycle broadly fit into this category including Tricolor (US), First Brands (US) and Market Financial Solutions (UK). Specifically, the underlying businesses were setup for a yesteryear environment. They were reliant on ease of re-financing but fraud motivations presented under pressure. Typical traits of demise in every cycle.

Then there remains many companies that continue to exist without producing sufficient revenues to cover costs (‘Zombie’ companies) who have continued to be propped up by ever flexible financing arrangements including low covenant loans and utilisation of amend and extend features. It is perplexing then that markets and valuations are so complacent.

The million-dollar question is whether this time is different.

Early indicators of defaults

An objective observation and assessment would suggest that not all episodes of complacencies and vulnerabilities eventuate in a crisis. In fact, history would suggest the opposite is more often the case. Typically, mis-valued markets and vulnerabilities self-adjust before they become systemic in nature. The combination of factors that typically lead to most major market corrections usually includes:

- Weak or unsustainable business fundamentals including poor cashflows,

- high leverage,

- poor ability to re-finance and elevated interest costs, and

- a loss of confidence by ultimate financiers (investors).

Whilst left field events are often the trigger for a crisis, some of the above can represent early indicators. Others are harder to observe until after the fact but one can monitor closely.

It is fair to observe that some of the indicators suggest at least a modest pickup in defaults should be expected from ultra-low levels. At the very least investors should be compensated adequately for this.

Key to healthy credit markets

Ongoing provision of credit to businesses is critical to the smooth functioning of economies. Through a circular feedback loop via employment, consumption is critical to businesses’ financial success.

For developed economies, credit to the private sector is provided by the banking system, public debt markets (investment grade, high yield, loans and securitised) and private debt markets including Business Development Companies (BDCs). Healthy credit markets typically exhibit the following characteristics:

- Robust underling business fundamentals (earnings, modest leverage, healthy interest coverage),

- strong technicals (ability to borrow, re-finance from several diverse sources, supply/demand well matched), and

- fair valuations to attract debt capital from investors and banks.

Reregulation in the post global financial crisis (GFC) environment has broadened the provision of private sector credit away from traditional banking channels. This has seen dramatic growth in public and private credit markets. Some of these funding sources, especially private debt, which is less regulated, have also had less ‘lived experience’ through cycles and are top of mind for investors whenever markets become concerned about defaults.

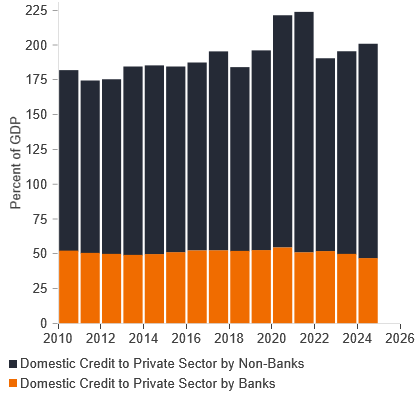

US private sector domestic credit, US debt outstanding

Source: Janus Henderson Investors, BIS, World Bank and Macrobond as at 3 March 2026.

However, private markets have brought more patient capital to the otherwise public and more observably volatile funding pools. The relationship between private equity participants (sponsors) with private debt has contributed to this. The ultimate capital providers sitting behind private markets are similarly patient with structures that support more permanent capital including insurers, pension funds, sovereign wealth funds and alike.

So, the question is whether private markets are the problem or the solution?

The answer depends on which part of the economic cycle businesses and markets are traversing. During recession style downturns with sharply rising unemployment and fast falling consumer demand environments private markets are likely to exacerbate the challenges as permanent loss of capital changes investor behaviour. Especially in their appetite for amend and extend requests and re-financing as well as general flow of credit to businesses. However, during other market environments including even soft economic growth periods, challenged or volatile times, private markets are likely to provide a further diversification in funding source and more patient capital that can work through challenges if required without overly disrupting businesses.

What’s different in this cycle

Most investors are well accustomed in navigating the well-known, slower burning economic and credit challenges. However, investors are facing some newer and faster moving risks including geopolitical uncertainty, key commodity price spikes such as oil and supply chain disruptions coupled with trade challenges. The mooted fast adoption of AI and potential displacement of labour along with traditionally strong technology segments such as Software as a Service (SaaS) provide further challenges. Some of these risks are potentially overestimated by markets and some risks will naturally subside. However, all of these have the potential to collide with near-perfect credit valuations and vibrant liquidity conditions.

Confidence can be fickle and liquidity is there until it isn’t.

Newer debt structures

One area of heightened focus at present is the fast growth of private credit, redemption status of BDCs like Blue Owl, Apollo and the prolific Collateralised Loan Obligation (CLO) market which in turn funds some 70% of the whole US leveraged market nowadays. Whilst these debt structures and product providers have been explicit with their less liquid and restrictive investor features, they haven’t been fully tested. The investor base whilst initially institutional such as pension funds, insurers and sovereign wealth funds now include the ‘democratised’ retail investors. Perhaps the latter may be less patient and surprised when liquidity is tested, even if warnings came with the label on the tin.

Another hidden biproduct of some of these debt instruments which have been constructed with ever weaker covenants and documentation is that they are structured to better preserve the equity investor than traditionally. It wouldn’t take much in the wrong economic and market circumstances for these structures to be tested and potentially deliver debt investors adverse outcomes.

A valid offset to this risk is the lofty war chest of debt capital that’s awaiting deployment with many investors sitting on the sidelines. Uniquely though, under duress, the whole lending structure may not fail as would be the case in traditional corporate bonds, but rather newer capital may be able to achieve stronger terms and better compensation whilst potentially damaging to existing investors.

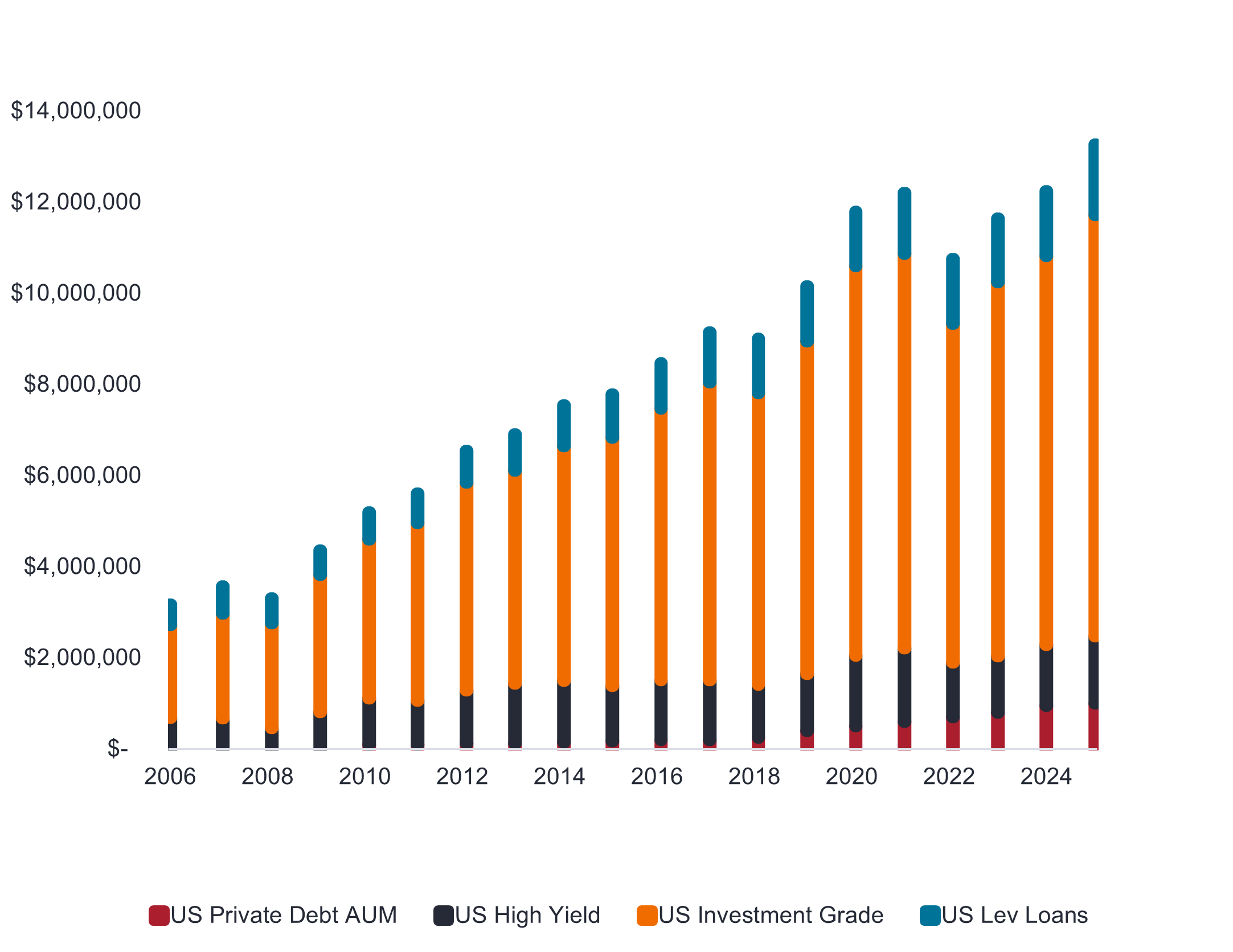

US Debt Outstanding (US$)

Source: Bloomberg, Morningstar, Janus Henderson estimates as at 31 December 2025.

Note: US Investment Grade represented by ICE BofA US Corporate Index, Leverage Loan represented by Morningstar US LSTA Leveraged Loan Index, US High Yield represented by ICE BofA US High Yield Index, US Private Debt represented by Janus Henderson estimates.

Looking ahead – Navigating the uncertainty

Many investors through history have tried to second guess the near-term future direction of markets and for the most part with minimal lasting success. Taking a binary view can often lead to incorrect timing, incorrect allocation but sometimes can get lucky. As they say, a broken clock is correct twice a day! A more prudent investors’ approach combines a through the cycle building approach of a portfolio of sound investments that generate strong yield advantages along with tactical uses of a full spectrum of active tools be they physical securities or derivatives paying attention to the valuations and risks of the day.

Faced with the choice of being fully invested in order to participate in enhanced returns or taking a more dramatic and conservative risk-free stance with either government only or cash exposures, whilst the environment appears uncertain, investors could be better served taking a nuanced active approach in being invested properly in fixed income and credit markets.

Today, perversely, in this risk indiscriminate market where volatility has been low and protection cheap, the following opportunities are available for investors of defensive portfolios which complement yield enhancing exposures:

- Credit protection remains cheap as a left tail hedge through credit default swaps (CDS),

- Government related including sub-sovereign sectors screen as cheap relative to corporate credit,

- supply of debt that are AI related create opportunities due to technical (supply) factors provided fundamentals are robust,

- certain industry and sub-sectors within investment grade remain attractive including the very defensive, regulated issuers,

- high yield markets may prove more resilient than loans markets which is contrary to historical experiences, and

- certain BBB rated corporate debt could outperform some AAA and AA structured debt.

And finally, there’s no substitute for broad, lowly correlated diversification of both market betas and active alpha levers along with ‘rainy day’ liquidity buffers.

A storm brewing can often present great investment opportunities for those well prepared ahead of time.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.