Key takeaways:

-

- The conflict has triggered a near-term energy security shock that is prioritising supply, inflation management and resilience over climate and health objectives.

- Short-term disruption may support fossil fuel use, but medium-term policy and investment incentives still reinforce the case for renewables, storage, electrification and EV adoption.

- For investors, the ESG effects extend beyond emissions to include fuel security, food inflation, public health and governance resilience, including defence and strategic preparedness.

Echoes of the 1970s: Energy shocks, security and ESG

The US-Iran conflict has triggered a 1970s-style energy shock, with energy security taking precedence over climate and health objectives in the near term. Longer term, it reinforces the case for renewables, electrification and greater domestic resilience.

As is widely reported, the impact of the Middle Eastern conflict is far-reaching, with first-round impacts causing price rises across multiple commodities and transport channels. These effects include higher prices for oil and gas, fertilisers and freight, which flow through to food, manufactured goods, and construction inputs across the economy.

Market focus has been on inflationary pressures and asset-price implications. Less immediately visible, but equally important, are the Environmental, Social and Governance (ESG) implications that may persist long after supply routes normalise.

Environmental factors

The immediate environmental damage arises from missile attacks on oil, gas and transport infrastructure, increasing pollution risks and military-related emissions. More enduring, however, is the energy price shock and resulting reliance on fossil fuels driven by security concerns.

Increased demand for coal – a short-term impact

With around 20% of global liquefied natural gas (LNG) trade normally passing through the Strait of Hormuz, attacks on regional gas fields have pushed gas prices higher and increased coal demand in power generation.

No country has formally extended coal terminal operations because of the conflict, but higher demand has lifted coal exports and utilisation in Australia, Indonesia and South Africa. While the conflict strengthens the case for renewables, it may also delay coal terminal closures where rollout has been slower than expected.

An accelerated rollout of renewables in the medium term

Unlike past oil shocks, this conflict is unfolding when solar, wind and battery technologies are already cost-competitive. Energy security concerns are still likely to accelerate investment in renewables, storage, and electrification, as Europe’s post-Ukraine response showed.

That trend appears to be continuing. EU policymakers are reassessing oil and gas dependence and considering more renewables, storage, and nuclear capacity, while China has called for faster renewable deployment and larger energy reserves. In Australia, the Federal Government has created a National Fuel Supply Taskforce to address energy security risks.

Transportation

As petrol prices rise, households have responded through behavioural responses such as greater working-from-home adoption, carpooling and public transport use, with regional rail demand reportedly lifting.

The appeal of electric vehicles (EVs) is also likely to increase, particularly where households can charge using rooftop solar. The prospect of fuel rationing could shift preferences further.

This shock has clear parallels with the oil crises of the 1970s, triggered by the OPEC embargo and the Iranian Revolution. Then, oil prices rose by around 400%, supply was rationed, and consumers shifted to smaller, more fuel-efficient vehicles, carpooling and public transport. The period also favoured Japanese manufacturers over larger domestic models such as the Holden Kingswood and Ford Falcon. Today, lower-cost EV manufacturers may benefit.

While EVs were not viable in the 1970s, the argument now extends beyond emissions reduction to energy sovereignty. In the 1970s, Australia produced around 60–70% of its oil, limiting exposure to global shocks. Today, domestic production has fallen sharply and Australia imports around 85–90% of refined fuels, reflecting depletion, refinery closures and a long policy focus on export-oriented coal and LNG rather than domestic oil security.

Social impacts

Fuel standards rollback: reversing recently addressed health risks

Burning higher-sulphur petrol raises emissions associated with asthma, lung cancer, chronic respiratory disease, cardiovascular disease and stroke.

Australia tightened fuel standards in mid-December 2025 to align with Europe, the US and Japan. The temporary rollback has allowed output from the Ampol Lytton refinery to remain in Australia rather than be exported, easing near-term supply constraints but increasing local pollution and health risks.

Energy, fertiliser and food prices: a social risk

Around one-third of global urea production originates in the Gulf region and transits the Strait of Hormuz. Because urea is critical for fertiliser production, any disruption quickly feeds through to reduced availability, higher farm input costs and, ultimately, higher food prices.

This is especially relevant for Australia, which imports a large share of its urea from the Gulf, with the disruption occurring just ahead of the April-to-June winter-cropping window.

Energy and food price shocks hit vulnerable households hardest because lower-income consumers spend more on essentials. While Australia has stronger safety nets than many countries, sustained increases in fuel and grocery prices still erode real incomes, particularly in regional areas. Elsewhere, the same pressures can contribute to food insecurity and social unrest.

Governance issues

Energy security as a governance risk

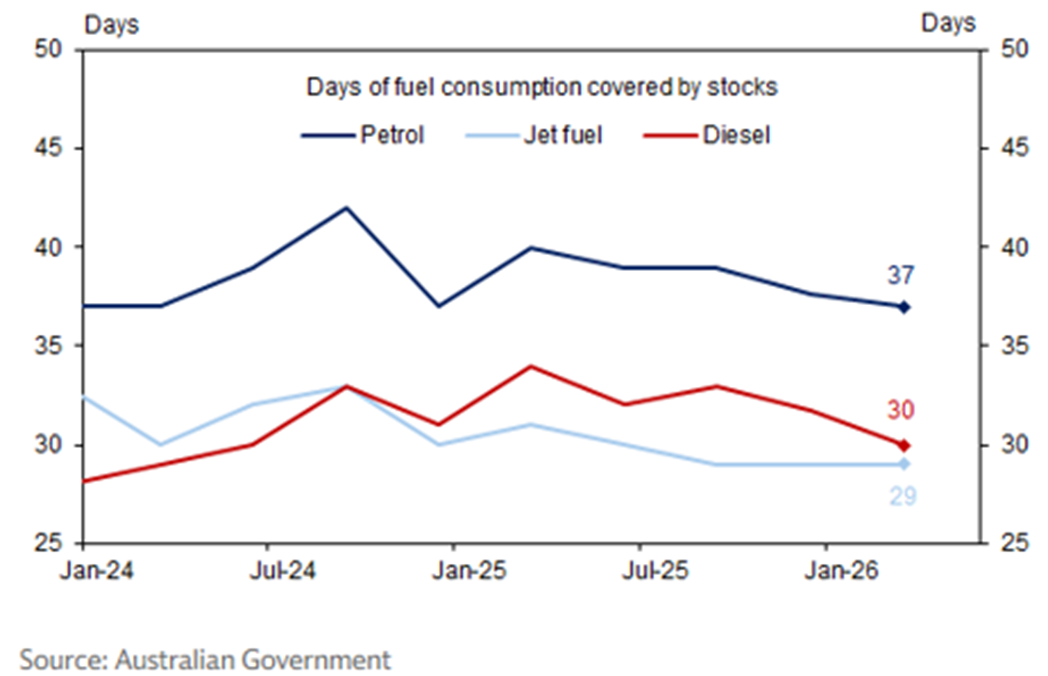

As at 10 March 2026, Australia held approximately 37 days of petrol, 29 days of jet fuel and 30 days of diesel, well below international benchmarks of 90 days.

This highlights dependence on imported refined fuels, limited domestic buffers and reactive rather than embedded resilience. While the government has coordinated supply and market stabilisation, the episode raises broader questions about preparedness and the strength of Australia’s energy security framework under prolonged disruption.

The argument for defence spending

This conflict underscores how national security increasingly intersects with the Governance and Social pillars of ESG. Effective defence capability underpins national stability, protection of critical infrastructure and governments’ ability to manage shocks affecting households, supply chains and energy security.

As a result, defence spending is increasingly being viewed as part of responsible governance, centred on resilience and civilian protection rather than military ambition alone.

Conclusion

While markets remain focused on inflation, growth and asset-price implications, the conflict is also influencing ESG outcomes for investors in less immediate but equally important ways. In the short term, energy security concerns have driven pragmatic responses that sit uneasily with climate objectives. At the same time, the shock has reinforced the longer-term case for EVs, renewables, electrification and reduced reliance on imported fuels.

Within our fixed income portfolios, we remain cautious on issuers with an over-reliance on fossil fuels, which has contributed to more defensive portfolio positioning in the current environment. Companies that are further advanced along their decarbonisation pathways should be better placed to navigate the headwinds of the current crisis. We also continue to seek selective investment opportunities in renewable energy where they align with portfolio objectives.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.