Key takeaways:

- Bond yields rose sharply in March as global conflict raised oil price and supply concerns.

- Our base case is for the RBA to continue to raise interest rates through 2026.

- We raised our long duration position modestly, taking advantage of higher yields in targeted tenors.

- Economic Focus: Energy shock phases

Market review

Bond yields rose sharply in March as global conflict raised oil price and supply concerns. The Reserve Bank of Australia (RBA) increased the cash rate for the second time this cycle, in an unusual split decision, hiking 25 basis points (bps) to 4.10%. They cited ongoing excess demand and inflation remaining above target. Combined with global events, this led to the 3 month BBSW rising 32bps to 4.31% and 6 month BBSW increasing 46bps to 4.78%. The 3 year yield rose 44bps to 4.65%, while the 10 year yield increased 32bps to 4.97%. Curve flattening continued, with the AU 3–10 year spread narrowing over the month.

Global energy markets were the key source of volatility during the month. Escalating conflict in the Middle East raised concerns around significant disruptions to oil and gas supply, pushing oil prices higher. Central Bank’s main concern is that higher energy prices feed directly into global inflation expectations, alongside the mechanical rise in headline inflation from rising fuel prices. This led to significant re-pricing of the policy path across the G10 economies, including for the RBA.

Australian monthly CPI data showed inflation at 3.7%yoy in February, with underlying measures proving sticky, while labour market conditions remained tight, with unemployment rising to 4.3%. Prior to global ructions, business and consumer surveys softened modestly, with confidence weighed down by higher borrowing costs, though activity indicators remained consistent with continued economic resilience. The weekly measures through March deteriorated sharply.

Market outlook

We see the RBA continuing to raise interest rates to address rising inflation risks, amid tight supply. Our high case is one where inflation remains elevated and the RBA are forced to raise interest rates more than expected into 2027. Our low case reflects a weaker economic outcome, particularly if supply constraints and rising costs act as a tax to subdue growth. We hold no tilt at present, viewing the risk profile as broadly distributed. We raised our long duration position modestly, taking advantage of higher yields in targeted tenors. We continue to take advantage of opportunities in volatile markets.

Monthly focus – Energy shock phases

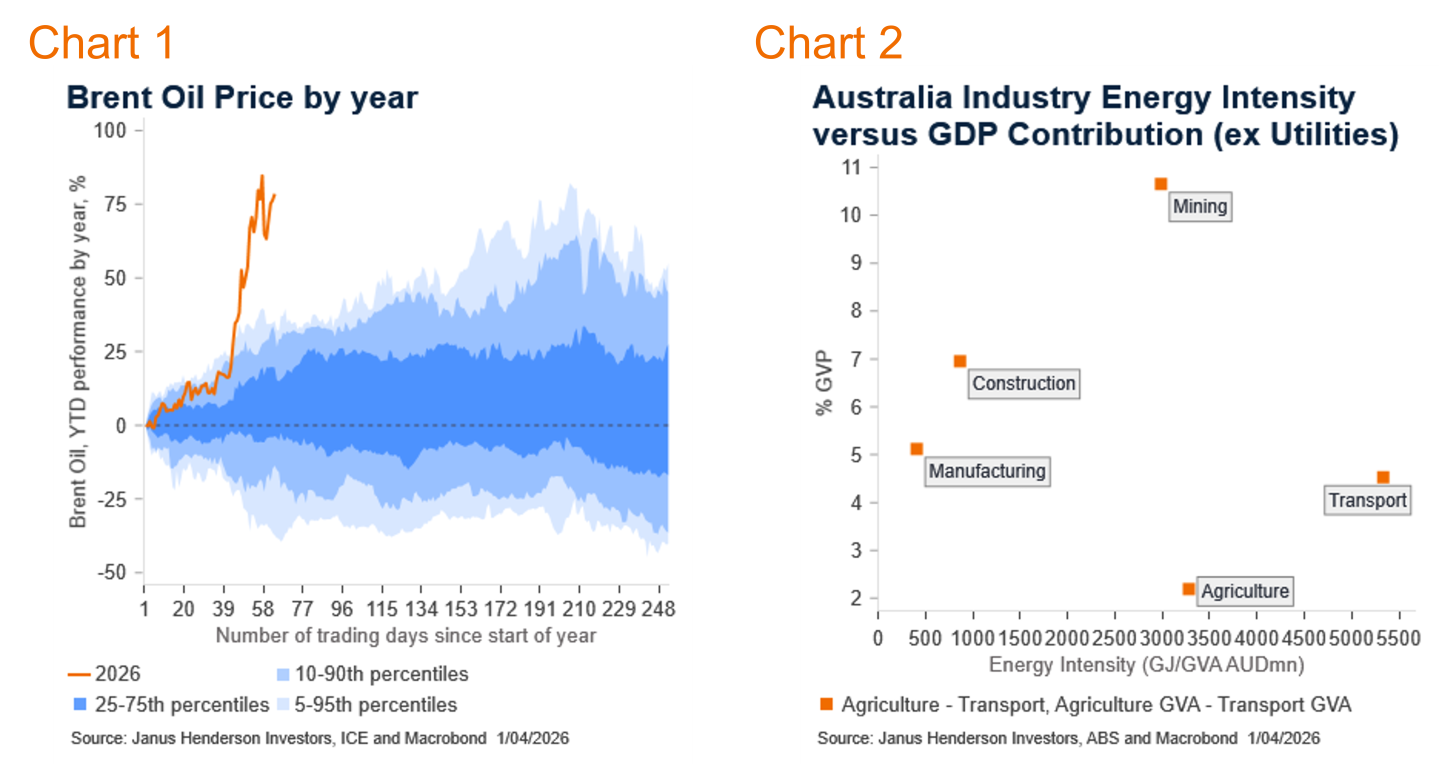

Financial markets are beating to oil’s rhythm, with the justifiable concern that a rise in oil prices has consequences for the real economy. The restricting of global energy supply lines can be thought of in a few different phases. We have seen the impacts of phase one, where there is an immediate rise in fuel prices. For Australia, the initial impact on growth is relatively neutral. Australia is a net energy exporter, and so the ability to provide energy to the rest of the world outweighs the immediate restriction of energy coming in, in an aggregate economy sense.

Critically, the other part of phase one is the inflation aspect. Australians are reliant on transport. Automotive fuel makes up just over 3% of the consumption basket of goods and services determining the consumer price index (CPI). Petrol is up 50% from the start of the conflict, while diesel is up more. A literal translation of a 50% rise in fuel prices, over a quarter, will raise the CPI headline just shy of half a percentage point. There isn’t always a literal translation, but the price impacts are very rapid, real and transparent. This alone is likely to see headline CPI reach 5% year on year though mid-year, double the RBA’s target level.

The conflict in Iran is now a month in, and the initial expectation of a swift resolution is receding. The initial market reaction has been to raise yields, accounting for a wholesale rise in inflation. This comes as the RBA has already raised interest rates twice, for a total of 50bps, to address inflation concerns that were rising before the onset of higher energy prices. That assessment now needs to address the second, and lengthier, phase of the impact of an energy shock.

Fuel and energy inputs have relatively low demand elasticities; demand cannot change much in the face of higher prices. Effectively, the price rises act as a tax. If households and businesses must pay more for a good that is difficult to use less of, or switch to an alternative, then demand for other goods and services needs to adjust lower to accommodate the rise in prices. The first evidence of this is in the sharp drop in consumer confidence. The ANZ-Roy-Morgan measure of consumer confidence, a weekly series, has now dropped to its lowest level since commencing in 1973, despite inflation expectations continuing to exceed record highs.

Supply restrictions and higher prices impact the cost and availability of inputs across a number of industries. This includes, but is not restricted to, mining, transport, manufacturing, agriculture and utilities which have higher levels of energy intensity to inputs. This should act as a brake on business and household demand due to rising costs. Given this, the expected economic growth profile moves lower over time, all else being equal, even with the net positive energy trade balance. This can place near term pressure on the RBA, even with the two rate rises behind them. They need to trade off the near-term rapid rise in prices, against a slower acting but persistent reduction in domestic demand.

These conflicting forces are exacerbated in the event that supply restrictions are increased, in the event of fuel rationing, for example. Fuel excise reductions may alleviate the price impact, but to-date, those adjustments do not override the full price change, and do not address the supply issue.

To weigh up the risk profile for the economy, and therefore for the RBA, means weighing up the probability of price rises and supply constraints driving inflationary impacts versus the growth aspect. The event is still evolving, to-date we see the RBA raising interest rates further to address the inflationary aspect, which builds off an already high base. The longer this present energy shock continues, the higher the domestic demand contraction through time. We currently see the RBA needing to lower interest rates through H2 2027 but will monitor for risks on both sides.

Views as at 1 April 2026.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.