Key takeaways:

- The inflation–growth trade-off was a theme running through markets in May.

- Australian data showed the disparity between households and the AI capex cycle.

- We see the peak in the RBA cash rate at 4.60% later this year.

- Economic Focus: The downbeat consumer

Market review

The inflation–growth trade-off was a theme running through markets in May, with bond markets reacting to higher policy rates and ongoing volatility in global energy prices. The Australian bond market, as measured by the Bloomberg AusBond Composite 0+ Yr Index, rose by 1.6% over the month, supported by strong income carry.

The Reserve Bank of Australia (RBA) increased the cash rate by 25 basis points (bps) to 4.35%, reinforcing its commitment to returning inflation to target. Short‑term funding markets reflected the tighter policy stance, with three‑month Bank Bill Swap Rates (BBSW) rising 8bps to 4.46%, while six‑month BBSW increased 4bps to 4.82%. Government bond yields moved lower across the curve, but not before hitting recent peaks, intra-month. The three‑year Commonwealth bond yield fell 29bps to 4.48%, while the 10‑year yield declined 23bps to 4.83%. Market‑based inflation expectations eased, with 10‑year inflation‑linked yields falling 15bps to 2.38%, suggesting some confidence that tighter policy will ultimately contain inflation.

Global fixed income markets were influenced by a reassessment of the pace and extent of future policy tightening in the US and other developed economies. While geopolitical tensions and supply‑side risks remained in focus, markets appeared increasingly desensitised to incremental news flow, with attention shifting toward growth risks and financial conditions.

Australian economic data were mixed. The ABS monthly CPI indicator showed inflation remaining elevated at 4.2%yoy, driven in part by fuel and services prices, while underlying inflation measures remained uncomfortably high. Labour market conditions were still tight, although unemployment was higher at 4.5%; forward‑looking indicators pointed to some easing in employment momentum. Interest rate sensitive sectors of the economy are showing signs of slowing, including house prices and household spending. However, capital expenditure was strong in the first quarter, with data centre fit outs boosting domestic demand.

Market outlook

We continue to see one last RBA hike, to 4.60% Our high case is one where inflation remains elevated and the RBA are forced to raise interest rates more than expected into 2027. Our low case reflects a weaker economic outcome, particularly if supply constraints and rising costs act as a tax to subdue growth. We hold no tilt at present, viewing the risk profile as broadly distributed. We maintain a modest long duration position and continue to take advantage of opportunities in volatile markets.

Monthly focus – The downbeat consumer

The outlook for households is challenged in the current economic climate. Moderating real incomes, from higher non-discretionary purchases inflation, mortgage payments, rents and taxes all take their toll. It shouldn’t be a surprise that consumer confidence is near its record lows. We anticipate a weakening household sector as the year extends. The RBA takes a whole of economy approach to monetary policy. While the household sector will feel squeezed, rising demand from the capital expenditure cycle, and supply led inflationary pressure, mean that a household reviving easing cycle isn’t coming soon.

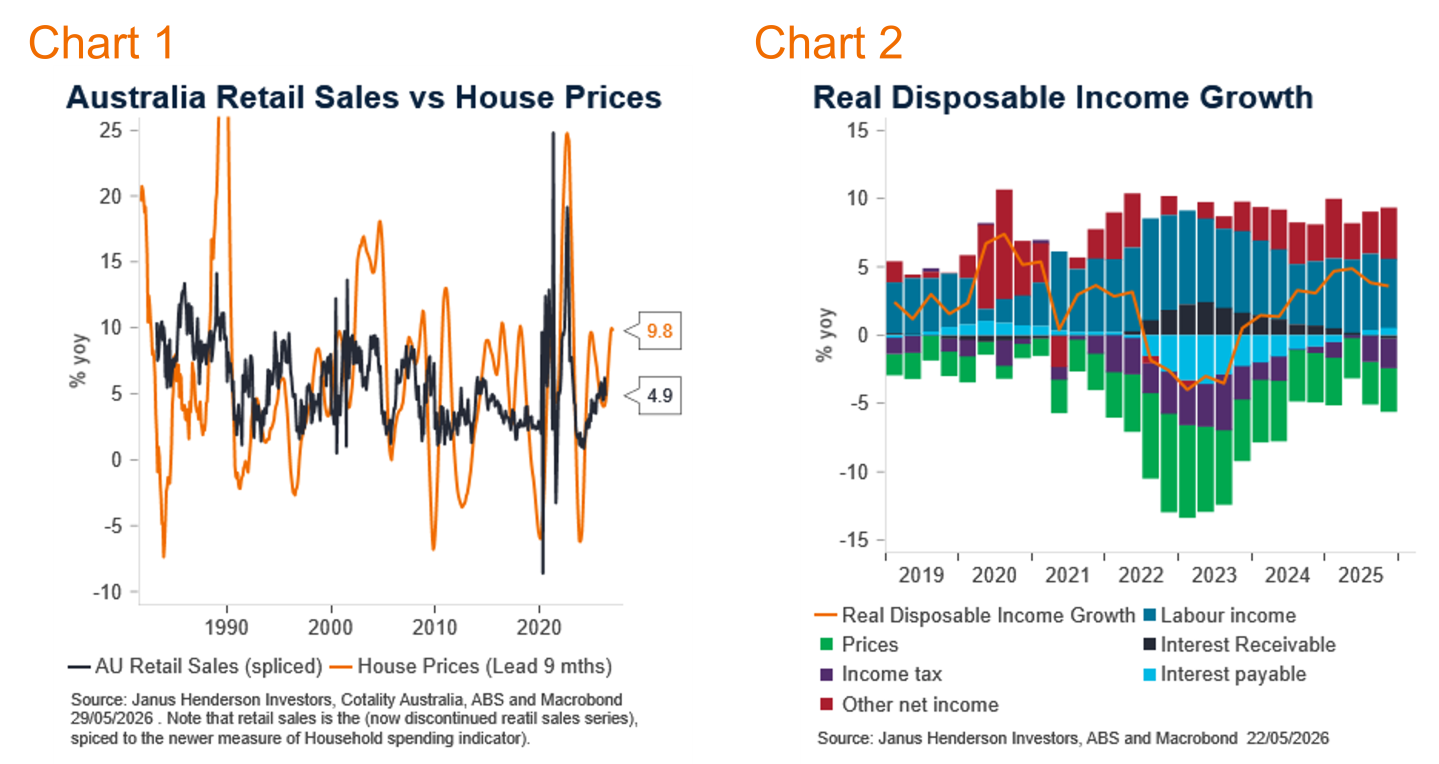

Australia’s new household spending indicator (HSI) has been robust for the last year, maintaining an impressive, steadily rising, annual growth rate; hitting 6.2% year on year growth in March 2026. This optimism flew in the face of increasingly dire consumer sentiment. The Westpac Melbourne Institute consumer confidence index plummeted to near historical lows when fuel prices skyrocketed in March, and they remain low. Despite this, retail sales continued to rise. The relationship between sentiment and actual activity has lessened in recent years, indeed the correlations turned negative. This is a broader phenomenon. In the US, where data is more granular, there is a huge disparity in the confidence data between voting preferences. Confidence data is more representative of the more fractured political environment than actual spending patterns.

Household consumption has had a long-held positive relationship with house prices. This works through several channels. Higher house prices create wealth effects and provide households with the confidence and backing for higher consumption. Secondly, higher house prices often generate higher housing turnover. Moving house comes with a vast number of expenses, often entailing retail purchases, such as whitegoods, carpets and furniture. While house prices have now peaked, they lead retail spending by around nine months. Given this, we may see near term resilience in consumer spending reflecting that past price growth, but moderation is expected through the second half of the year. Trend weakening at this stage would point to a weaker than expected outcome. The soft April HSI outcome hints at downside risks but was distorted by nominal changes in fuel spending.

The labour market is another factor that is likely to weigh on spending. The labour market has been characterised by the RBA as “tight,” even with the near-term rise in the unemployment rate, to 4.5%. Forward indicators of employment have started to soften, such as the NAB business survey of hiring intentions, and household views on future employment. This points to moderation in employment through the second half of the year and a steady rise in the unemployment rate.

With the outlook for the largest individual component of Australia’s GDP growth looking soft, it would be reasonable to start expecting the RBA to respond with policy easing. There are two important reasons why we wouldn’t expect that easing to come until later in 2027. But we do expect it to come. First, is the very fact of cost-of-living pressure. Inflation needs to be addressed, and central to the RBA’s mandate. If supply pressures drive prices higher, the only tool the RBA has is to lift interest rates and supress demand enough to counter supply-led costs. Fiscal, trade and energy policy can play a part in alleviating costs, but these are supplementary to monetary policy and under the RBA’s control. The second is the rise in domestic demand driven by the private capital expenditure cycle. The AI transformation is fully underway, and less sensitive to interest rates than the rest of the economy. The household may point to well below average growth, but overall GDP will be positive, driven by rising capital expenditure on energy infrastructure, data centres and software spend. As we have always known, monetary policy is a blunt instrument. It may feel that way for consumers over the coming year.

Views as at 1 June 2026.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.