Key takeaways:

- Inflation remains a broad market concern; bond markets reacted to fluctuating oil prices.

- Our base case is for the RBA to continue to raise interest rates through 2026.

- Repricing of central bank cycles is well established, before the longer-term implications of events begin to show.

- Economic Focus: Inflation begets inflation

Market review

Inflation remains a broad market concern, and bond markets reacted to fluctuating oil prices through the month. The Australian bond market, measured by the Bloomberg AusBond Composite 0+ Yr Index, rose 0.1%.

The RBA cash rate was unchanged at 4.10% over the month. Short‑term funding markets saw modest upward pressure, with three‑month Bank Bill Swap rates (BBSW) rising to 4.37%, widening the spread to the cash rate to 27 basis points (bps), while six‑month BBSW was little changed at 4.77%. Government bond yields increased across the curve. The three‑year yield rose 11bps to 4.76%, while the 10‑year yield lifted 9bps to 5.06%, reflecting ongoing inflation concerns. 10-year inflation‑linked bonds reflected rising inflation concerns, lifting to 2.54%.

Geopolitical ructions continue to influence bond markets, but there are signs of news fatigue. The re-pricing of central bank hiking cycles is well established, as markets think about the long-term implications of higher energy prices and supply restrictions facing off against rising artificial intelligence (AI) investments.

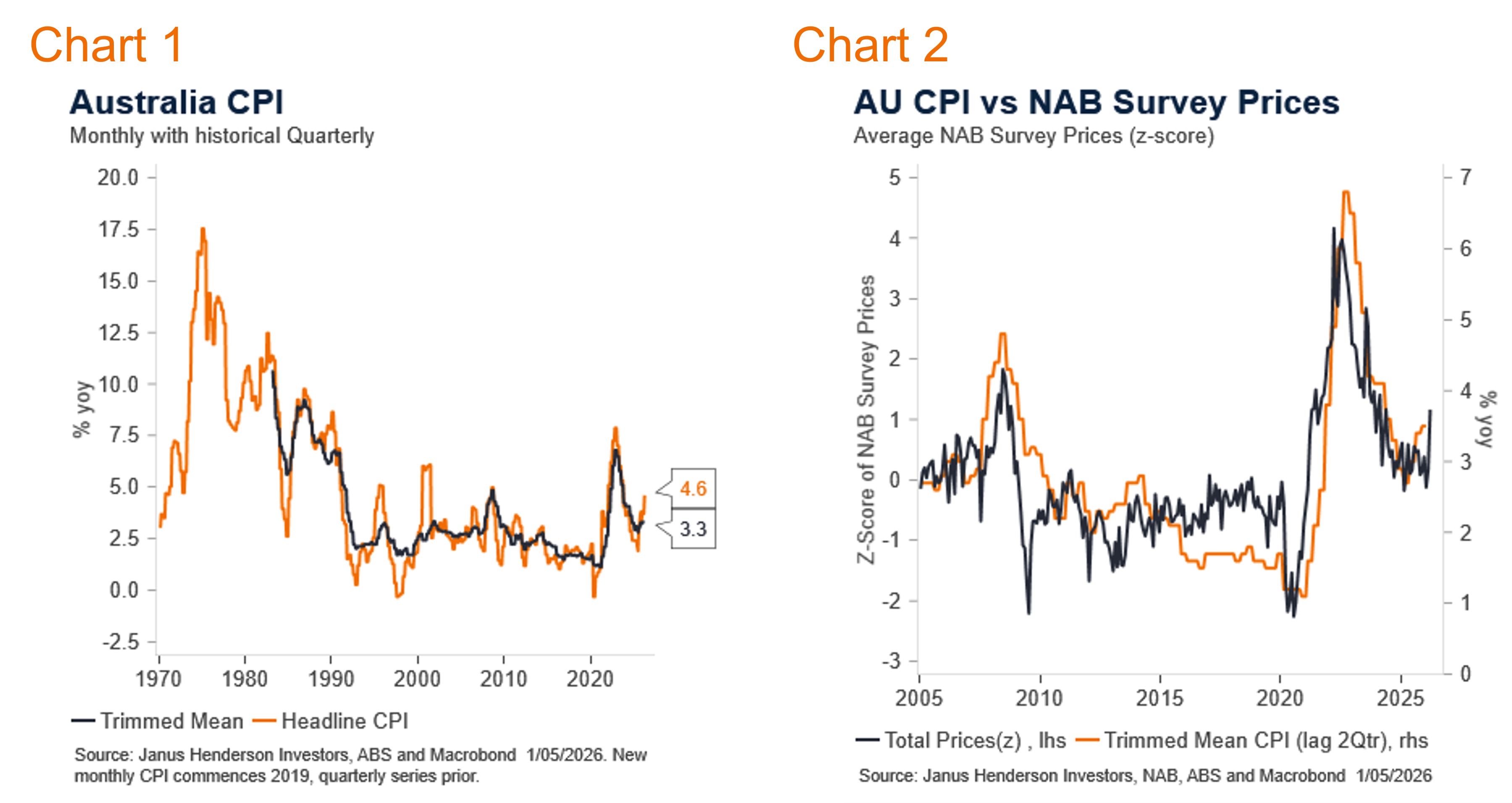

Australian economic data was mixed. The ABS monthly CPI indicator showed a fuel-induced inflation spike, to 4.60%yoy, but not as bad as the market had feared. The trimmed mean measure remained elevated at 3.30%yoy, which will concern the RBA. Labour market conditions remained tight, with unemployment holding at 4.30%, though forward‑looking indicators suggested moderation ahead. Survey data showed plummeting consumer and business confidence, while business conditions remained resilient. This highlights the nature of the immediate price shock versus the lag in the real economic outcomes. These themes were broadly reflected in many of the developed economies.

Market outlook

We see the RBA continuing to raise interest rates to address rising inflation risks, amid tight supply. Our high case is one where inflation remains elevated and the RBA are forced to raise interest rates more than expected into 2027. Our low case reflects a weaker economic outcome, particularly if supply constraints and rising costs act as a tax to subdue growth. We hold no tilt at present, viewing the risk profile as broadly distributed. We adjusted our duration position modestly, taking advantage of mid-month lower yields in targeted tenors. We continue to take advantage of opportunities in volatile markets.

Monthly focus – Inflation begets inflation

Two months after the global energy price shock, we start to gain a more comprehensive picture of the inflationary outlook. We expect headline inflation to rise sharply over coming months, remain elevated for much of the year, before moving back toward target in 2027. The first and second phase should be the impetus for further RBA tightening, while the moderation phase is based on slower demand both locally and globally but is dependent on a confluence of factors.

As we noted last month, the first-round impact of a rise in oil prices is the rise in fuel costs, and a direct translation to headline CPI. This came to pass in the March CPI outcome of 1.10% in the month, raising the annual rate to 4.60%yoy. This was below the market’s expectations, but it is certainly above the (pre energy shock) RBA forecast for inflation. The trimmed mean measure, at 3.30%yoy was as expected, but highlights the sticky and elevated starting point for an inflation cycle.

The March data is too soon to show the full flow through in inflation, but we have seen a few indications suggesting a more rapid pass through this cycle. It is often the case that recent past cycles better inform current economic cycles. Prior to the 2021-2023 period of excess inflation, Australia had an extended period of below target inflation. Given that experience, in the last cycle there was a slow build in response to the global supply shocks of the 2021-2023 period. This time, the pass through is showing faster, as households and businesses are now more accustomed to rising prices.

Part of this should be attributed to the rise in inflation expectations. The RBA are constantly reminding us that they cannot allow inflation expectations to become unanchored. The reason for this is that higher expectations allow for the ability to pass on higher prices rises quickly. If you are used to rising prices, then you are more likely to accept higher prices, even if you don’t like it. Price increases become normalised. These then get pushed through to wage negotiations, as employees see their cost base rise, and seek to recoup some of that erosion in real incomes through higher nominal wage asks.

We have seen the burgeoning evidence of this peaking through. Measures of inflation expectations are rising quickly. The RBA measures of inflation are relatively well contained, albeit the latest measure of consumers is now at 3%yoy. Some of the more frequent surveys are higher than this, such as the ANZ-Roy Morgan weekly survey, which is currently at 6.90% (four week moving average). The NAB business survey also shows a sharp rise in purchase prices, and overall prices lifted to the highest in a year. Not yet in these numbers are the very rapid pass through of global supply chain restrictions in the construction sector, which took longer to be presented to end consumers last time. Plumbing suppliers noted in their recent reporting that they would raise piping prices 36%, for example, timber by 15%, steel by 15-25%1, only a month after the initial price event occurred.

This cycle, we anticipate a faster flow-though of higher energy and supply constrained related pricing, as compared to the 2021-2023 inflation peak. The trajectory lower is dependent on the confluence of; longevity of the energy price peak, rate of decline in real incomes, cost-of-living fiscal policies and the peak in monetary policy. It also hinges on the influence of the concurrent AI boom, which is less interest, and real rate, sensitive than other sectors. At present, we see inflation easing back through 2027, but see risks to the upside in the peak and a more prolonged episode.

Views as at 1 May 2026.

1https://www.afr.com/companies/infrastructure/reece-pushes-36pc-price-rise-on-plastic-pipes-in-building-cost-shock-20260324-p5ts6x

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.