Turning the tide

The urbanisation of cities across the globe has seen demand for housing far outstrip supply. It’s led to an explosion in property values and rents, as well as exacerbating shortages.

With modest wage growth in many countries simply unable to keep up, this has created an undesirable situation that stands to entrench inequality.

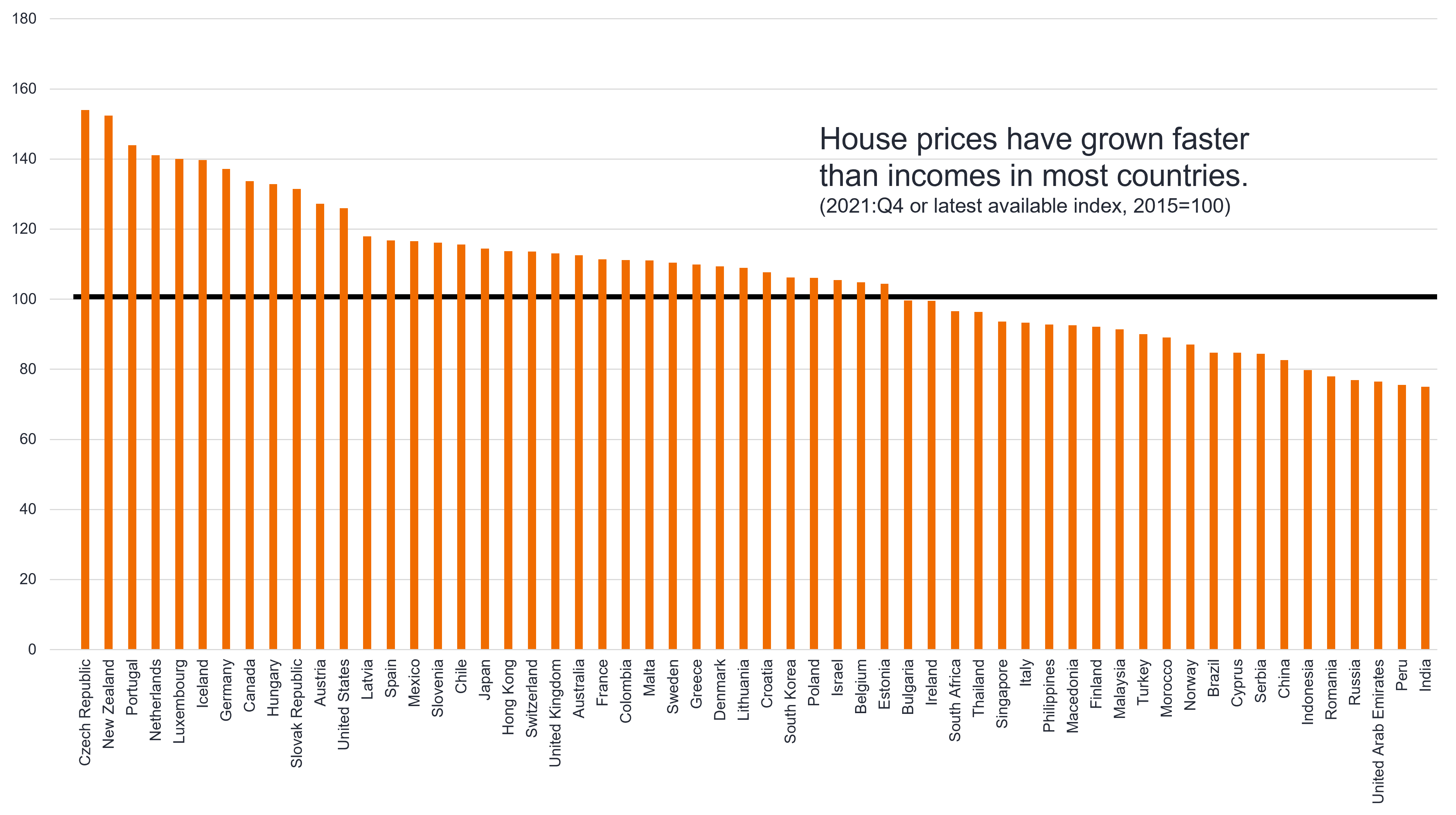

Chart 1: House price-to-income ratio around the world

Source: Bank for International Settlements and World Economic Outlook. As at 22 September 2022.

While tailored solutions for each location will be required, social, sustainability, and sustainability-linked bonds stand to play a pivotal role in alleviating some pressure.

Housing affordability: by the numbers

|

How bonds support Australia’s housing market

In Australia, housing affordability is felt acutely across the country, especially in capital cities like Sydney and Melbourne. This has prompted the Federal Government to recently announce a $10 billion Housing Affordability Fund to help address the issue.

If passed by Parliament, the Fund will bolster the Government’s existing support measures which already include funding for the National Housing Finance and Investment Corporation (NHFIC) and providing credit for loans issued by the Affordable Housing Bond Aggregator (AHBA).

These low-cost and long-term loans are provided to registered community housing providers with lower interest rates. Discounted rates can only be offered because the NHFIC issues bonds to raise the capital needed to fund the AHBA’s loans.

In 2021-22 alone, the NHFIC approved $509.3 million of new loans to community housing providers, saving them an estimated $96.2 million in lower interest and fees and enabling the construction of 3,296 social and affordable homes3.

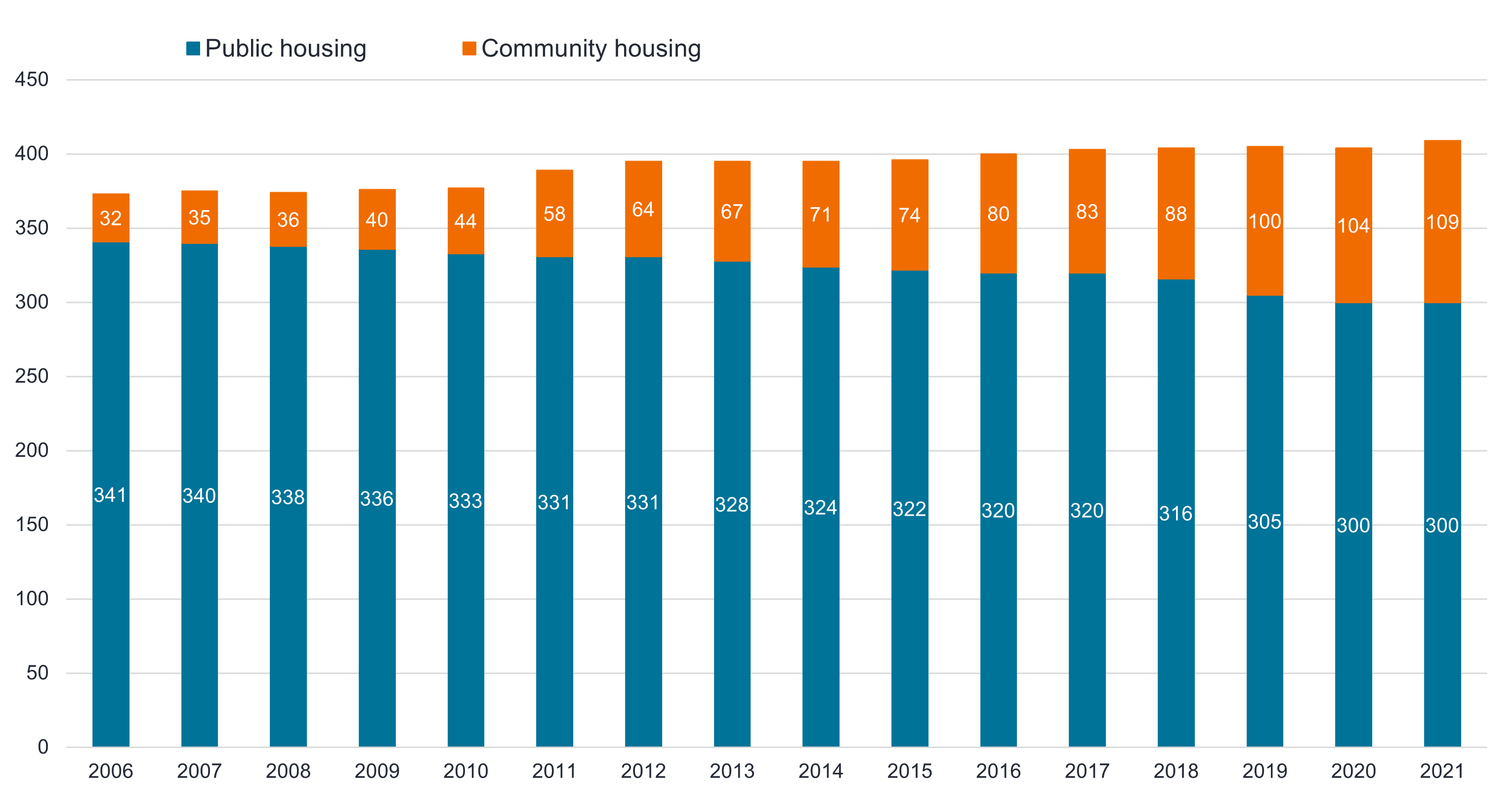

Chart 2: Australian community and public housing stock

Source: Australian Institute of Health and Welfare. As at October 2022.

Pacesetters reveal growth pathway

While the Australian subsidised housing sector is nascent, it is growing in line with other markets, including the UK and US, where large institutional investors are driving activity.

In the UK, approximately 70% of the capital to build affordable housing is currently sourced from private financing, up from 30-40% in the 2000s. In the US, annual transaction volumes are approximately $US36 billion in 2021, up from $US1.3 billion in 20114.

Building dreams: The case for social bonds

Affordable housing is a basic human need that has become increasingly difficult to access for many. While more investment is flowing into subsidised housing, substantially more is required to keep pace with demand. With issuers increasingly turning to sustainability bonds to create affordable housing supply, it presents an opportunity for investors of all kinds to participate in a growth area.

Introducing Sustainable CreditOur new active ETF, the Janus Henderson Sustainable Credit Active ETF (ASX:GOOD) is poised to capitalise on this growing segment of the fixed income market, which can deliver financial returns, while also seeking to do some good in the world. |

For important product information and disclosures such as PDS and TMD, please visit: https://www.janushenderson.com/en-au/investor/product/sustainable-credit-fund/

- What has caused the global housing crisis – and how can we fix it – WEF

- Demographia International Housing Affordability – Urban Reform Institute

- NHFIC Social Bond Report 2021-22 – NHFIC

- International Capital Flows Into Social and Affordable Housing – NHFIC

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.