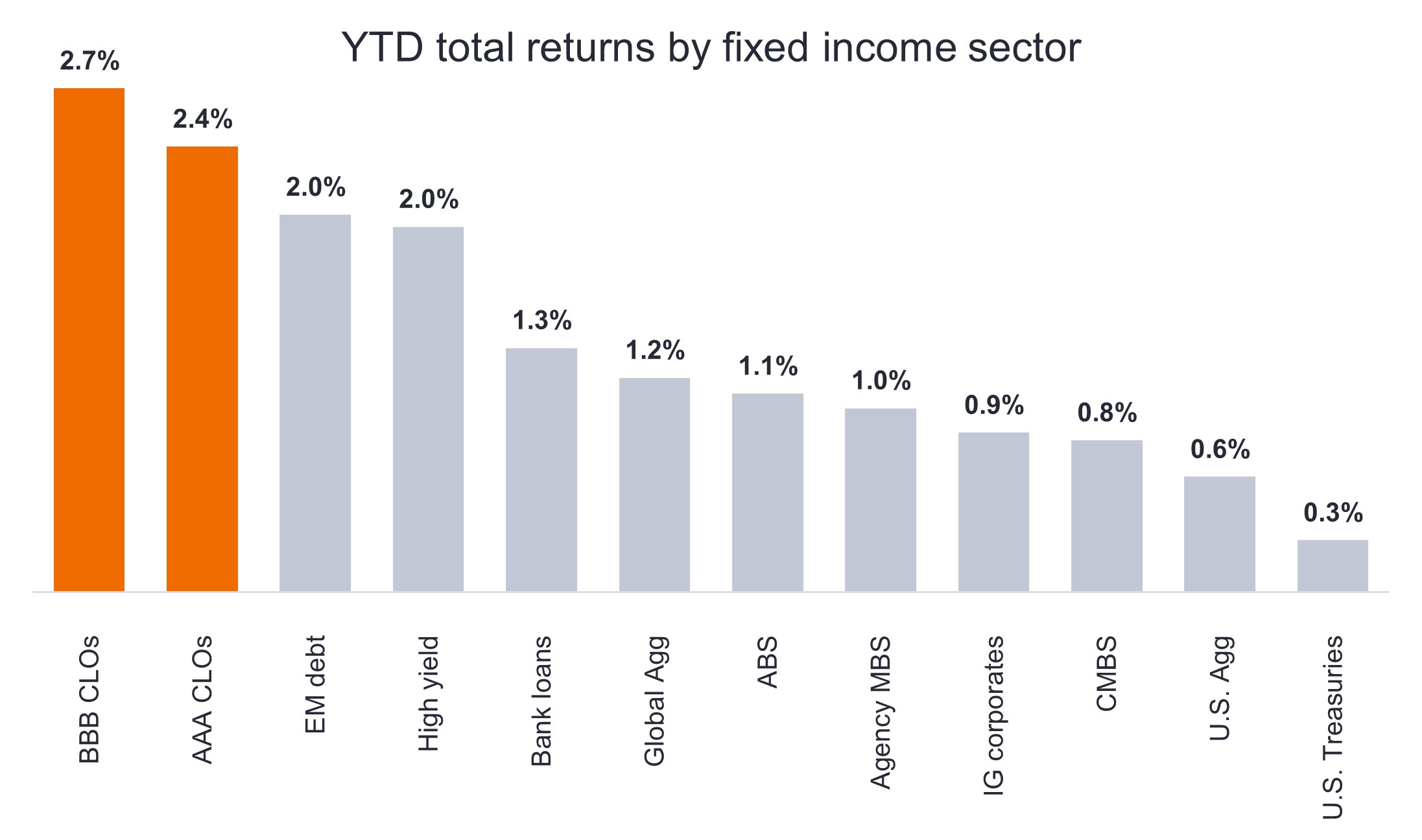

Chart to Watch: CLOs continue to lead the way in fixed income returns

In this 2026 mid-year check-in, Global Head of Securitised Products John P Kerschner explains why floating-rate collateralized loan obligations (CLOs) have continued to be the best-performing assets in global fixed income markets.

Source: Bloomberg, as of 30 June 2026. Indices used to represent asset classes: CLOs represented by JP Morgan CLOIE Indices, Bank loans represented by Morningstar LSTA US Leveraged Loan Index, EM debt, high yield, asset backed securities (ABS), agency mortgage-backed securities (MBS), investment-grade (IG) corporates, commercial mortgage-backed securities (CMBS), Treasuries, U.S Agg and Global Agg represented by relevant Bloomberg indices. Past performance does not predict future results.

Skeptics may argue that the rise in interest rates since 2022 has been a fluke tailwind for floating-rate assets – as if CLOs and other floating-rate bonds got lucky and ‘won the interest rate lottery’ – and that it won’t happen again. Ironically, we concur, at least in part: It IS because interest rates have risen that CLOs have done well (also because credit spreads have tightened), but we don’t see the rise in rates as an isolated event. Rather, we think all signs point to the regime of higher rates being here to stay. And that’s why we believe investors should consider leaning into CLOs instead of writing off their outperformance as a one-time fluke of Covid-induced, outsized inflation.

- Recent outperformance from CLO sectors is no outlier: BBB CLOs have been the best-performing fixed income sector year to date (YTD) in 2026, but also over the preceding 1-, 3-, 5-, and 10-year periods. AAA CLOs have outperformed most other indices on a 5- and 10-year basis, despite their far higher credit quality and very low volatility profile.

- In our view, the only reason to have no allocation to high-quality floating-rate debt is if one believes rates are going to zero (and staying there). For that to happen, inflation would need to virtually evaporate, which appears very unlikely considering the inflationary underpinnings of a strong labor market, robust economic growth, geopolitical tensions, higher oil prices, AI-driven shortages, large fiscal deficits, and deglobalization.

- We believe floating-rate exposure is essential to navigating the post zero-interest-rate-policy (ZIRP) global economy. At the same time, we prefer higher-quality assets: We think the best way to gain floating-rate exposure is through CLOs, which offer credit enhancement over loans and a mechanism for investors to select their desired level of risk.

IMPORTANT INFORMATION

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Credit quality ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest).

A credit spread is the difference in yield between a corporate or securitized bond and a government bond (such as a U.S. Treasury) of the same maturity. It compensates investors for the risk that the borrower might default.

Volatility measures risk using the dispersion of returns for a given investment.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.