Kernpunten

- The outlook for U.S. large-cap equities remains positive, supported by a broad capital investment cycle, productivity gains, and expectations for double-digit earnings growth.

- While market valuations are elevated, earnings growth is strong and the industry mix within major indices has shifted toward faster-growing sectors that typically command higher multiples.

- We believe companies with scale, strong balance sheets, and the ability to invest in productivity-enhancing technologies are positioned to lead as AI adoption broadens across the economy.

As we look toward 2026, we maintain an optimistic outlook for U.S. large-cap equities. This view is supported by a powerful capital investment cycle, a resilient consumer, and broadening productivity gains that have strengthened corporate earnings.

While this environment presents opportunities, navigating elevated concentration and valuations requires a selective, adaptive approach. Our focus remains on companies with scale, strong balance sheets, and the ability to invest in productivity-enhancing technologies.

Capital investment has driven productivity gains

The U.S. economy is benefiting from a historic capital expenditure boom. AI is a primary driver, with technology infrastructure spending now accounting for a meaningful portion of U.S. real GDP growth. Robust demand for cloud services and data center capacity shows no signs of slowing.

However, the capital expenditure story extends beyond technology. Recent tax policies allowing immediate depreciation of investments are fueling a broader spending cycle across the market. This widespread capital investment drives productivity gains, which could support future economic growth.

The shift toward greater efficiency has become increasingly evident. More companies are providing examples of AI applications delivering tangible productivity gains. The last two earnings seasons showcased impressive operating leverage, with companies posting strong revenue growth while controlling expenses. This suggests businesses are already seeing returns on their investments, boosting margins and earnings despite cost pressures.

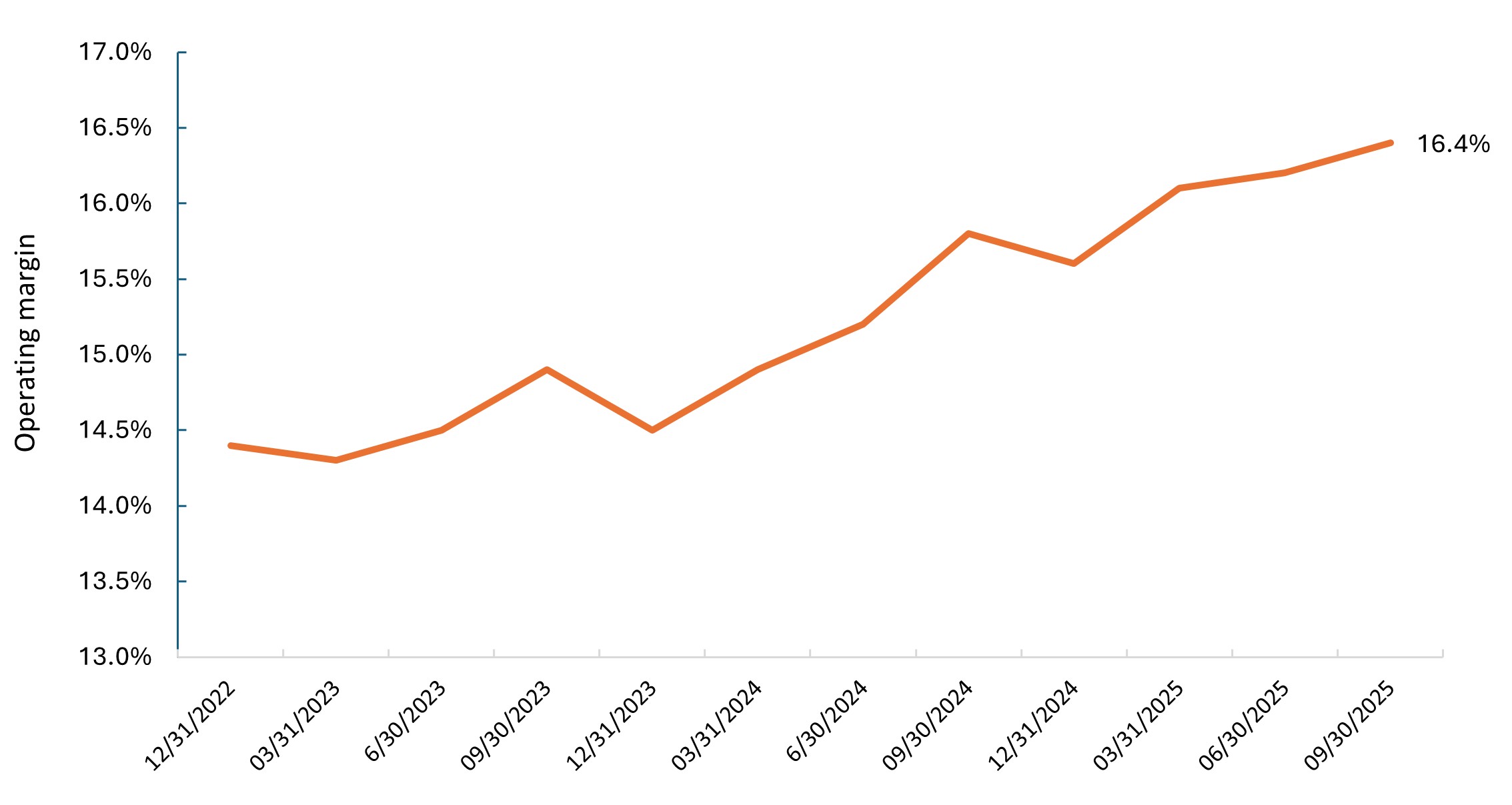

Exhibit 1: S&P 500® Index operating margin (ex-energy)

Outside the volatile Energy sector, the market has benefited from consistent margin improvements over the last two years. Gains have been led by sectors like Communication Services, Information Technology, and Financials where companies can best leverage technology to improve operations.

Source: Bloomberg Intelligence, as of 14 November 2025.

Consumer spending remains resilient

We continue to be optimistic about consumer spending even as labor force growth has softened. Wage growth of around 4.5% continues to outpace pre-pandemic levels, supporting spending. Consumer balance sheets are strong, with the ratio of debt service to disposable income within normal historical range and credit delinquencies remaining low.

However, we recognize consumer spending is always shifting and there will be segments of the economy that contract while others expand. When analyzing credit card data, overall spending is strong, but some segments are flat, such as those more impacted by inflation and moderating job growth. Today, we see that consumers tend to favor experiences over goods, and that there is strong demand for travel.

We see the potential for an additional boost in consumer spending in 2026 from recent tax reforms, which should lead to better refunds during tax season. While spending is strongest among upper-income households benefiting from housing and market gains, the overall picture remains positive.

Market concentration reflects earnings leadership

Market concentration in the U.S. is at a level we haven’t seen in recent history. But when we look at the earnings growth and sustainability of the companies with the largest market capitalization, it’s not surprising because they are leading the technology transformation.

Given AI infrastructure’s importance to the economy, we’re monitoring whether companies achieve appropriate returns, execute on their backlogs, and generate revenue that supports continued investment. Should the AI investment cycle plateau and earnings trajectories change, investors must be prepared to adjust.

While multiples have expanded in the AI infrastructure theme, demand has continued to surprise to the upside, so earnings growth supports the multiples for now, in our view. That said, being adaptive is the right positioning today. Considerable time must be spent assessing balance sheets, cash flow statements, and business sustainability metrics to ensure fundamentals justify market weights.

Putting valuations in context

We acknowledge that the market’s overall multiple is elevated. However, context is helpful. First, the market’s composition has fundamentally shifted. The fastest-growing, highest return on invested capital (ROIC) sectors within the major indices have significantly increased in weight.

Furthermore, strong earnings support current multiple levels. The market delivered more than 12% earnings growth in the second quarter, with similar expectations through 2026. Unlike the 2000 tech bubble, today’s valuation expansion has been matched by a widening profitability premium. We can still find plenty examples of high-quality companies in secular growth industries trading at or below historical multiples.

Where we see opportunity

Within the AI theme, our focus is on both enablers and adopters. Enablers include semiconductor, cloud, and software companies, as well as enterprise platforms developing AI and automation solutions. Adopters are companies across all sectors that have committed to this new technology and are investing aggressively.

Encouragingly, earnings strength has extended beyond AI and technology. Commercial aerospace, capital markets, medical technology, and travel have delivered impressive results. This breadth suggests corporate health is more widespread than some narratives suggest.

Within financial services, investment banking revenues have grown more than 50% based on increased mergers and acquisitions activity and initial public offerings. We think capital markets activity will be strong for the next couple of years as funding continues for the AI capital expenditure investment cycle, potentially benefiting investment banks, ratings agencies, and exchanges. Also, digital payment companies have continued to grow earnings at a 15% annual clip as consumer spending remains strong.

We’re also finding attractive opportunities in industrials focused on automation and electrification. In addition, the need for power and cooling technology for data centers presents compelling opportunities.

Innovation and scale support market leadership

We believe the current environment underscores the advantages of scale, innovation, and access to capital that define leading U.S. large-cap companies. Transformation driven by AI is expensive, requiring strong balance sheets and market leadership to fund the necessary investments and harness the data for effective applications. We believe companies lacking scale or investment capabilities risk falling behind and losing market share.

Overall, we believe environment for U.S. large-cap equities remains positive heading into 2026. Innovation leadership and entrepreneurial culture extend beyond technology into important areas like healthcare devices and diagnostics as well as biotechnology. The U.S. also has a flexible labor force that can be retrained for more productive roles and opportunities as some jobs are replaced by AI. The combination of capital investment, productivity gains, a resilient consumer, and broadening earnings growth provides a durable foundation for continued market leadership.

Belangrijke informatie

Actief beheerde portefeuilles leveren mogelijk niet de beoogde resultaten op. Geen enkele beleggingsstrategie kan winst garanderen of het risico op verlies verwijderen.

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Aandelen brengen risico's met zich mee, waaronder marktrisico's. Rendementen fluctueren als reactie op ontwikkelingen bij de emittent en in de politieke en economische situatie.

Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition.

Groeiaandelen zijn onderhevig aan een verhoogd risico op verlies en prijsvolatiliteit en kunnen hun vermeende groeipotentieel niet waarmaken.

De gezondheidszorg heeft wereldwijd te maken met verschillen in overheidsvoorschriften en vergoedingen, naast verschillen in goedkeuring van de autoriteiten voor producten en diensten die een aanzienlijk effect kunnen hebben op de prijs en de beschikbaarheid, en kan sterk nadelig beïnvloed worden door snelle veroudering en aflopende patenten.

De koers-winstverhouding (K/W) meet de aandelenkoers in verhouding tot de winst per aandeel voor een of meer aandelen in een portefeuille.

Return On Invested Capital (ROIC) is a measure of how effectively a company used the money invested in its operations.

S&P 500®Index weerspiegelt de prestaties van Amerikaanse largecapaandelen en de bredere Amerikaanse aandelenmarkt.

Volatiliteit: de maatstaf voor de beweeglijkheid van de koers van een portefeuille, effect of index. Als de koers sterk op en neer beweegt, is er sprake van hoge volatiliteit.Als de koers licht en langzaam op en neer beweegt, is er sprake van lage volatiliteit.Hoe hoger de volatiliteit, hoe hoger het risico van de belegging.

Dit zijn de standpunten van de auteur op het moment van publicatie en kunnen verschillen van de standpunten van andere personen/teams bij Janus Henderson Investors. Verwijzingen naar individuele effecten vormen geen aanbeveling om effecten, beleggingsstrategieën of marktsectoren te kopen, verkopen of aan te houden en mogen niet als winstgevend worden beschouwd. Janus Henderson Investors, zijn gelieerde adviseur of zijn medewerkers kunnen een positie hebben in de genoemde effecten.

Resultaten uit het verleden geven geen indicatie over toekomstige rendementen. Alle performancegegevens omvatten inkomsten- en kapitaalwinsten of verliezen maar geen doorlopende kosten en andere fondsuitgaven.

De informatie in dit artikel mag niet worden beschouwd als een beleggingsadvies.

Er is geen garantie dat tendensen uit het verleden zich zullen doorzetten of dat prognoses worden gehaald.

Reclame.

Belangrijke informatie

Lees de volgende belangrijke informatie over fondsen die vermeld worden in dit artikel.

- Aandelen/deelnemingsrechten kunnen snel in waarde dalen en gaan doorgaans gepaard met hogere risico's dan obligaties of geldmarktinstrumenten. Als gevolg daarvan kan de waarde van uw belegging dalen.

- Het is mogelijk dat een emittent van een obligatie (of geldmarktinstrument) niet langer bereid of in staat is om de rente te betalen of kapitaal aan het Fonds terug te betalen. Als dit gebeurt of als de markt denkt dat dit kan gebeuren, zal de waarde van de obligatie dalen.

- Wanneer de rentevoeten stijgen (of dalen), zullen de prijzen van verschillende effecten anders worden beïnvloed. In het bijzonder zal de waarde van obligaties gewoonlijk dalen als de rentevoeten stijgen. Over het algemeen wordt dit risico groter naarmate de looptijd van een obligatiebelegging toeneemt.

- Het Fonds belegt in hoogrentende obligaties (onder beleggingskwaliteit). Hoewel dergelijke obligaties doorgaans hogere rentevoeten bieden dan obligaties van beleggingskwaliteit, zijn ze speculatiever van aard en zijn ze gevoeliger voor ongunstige veranderingen in de marktomstandigheden.

- Als een Fonds een hoge blootstelling heeft aan een bepaald land of een bepaalde geografische regio, loopt het een hoger risico dan een Fonds dat meer gediversifieerd is.

- Het Fonds kan gebruikmaken van derivaten om zijn beleggingsdoelstelling te verwezenlijken. Dit kan leiden tot hefboomwerking, wat de resultaten van een belegging kan uitvergroten en waardoor de winsten of verliezen van het Fonds groter kunnen zijn dan de kosten van het derivaat. Het gebruik van derivaten gaat ook gepaard met andere risico's, waaronder met name het risico dat een tegenpartij bij derivaten niet in staat is om haar contractuele verplichtingen na te komen.

- Wanneer het Fonds, of een afgedekte aandelenklasse/klasse van deelnemingsrechten, tracht de wisselkoersschommelingen van een valuta ten opzichte van de basisvaluta te beperken, kan de afdekkingsstrategie zelf een positieve of negatieve impact hebben op de waarde van het Fonds vanwege verschillen in de kortetermijnrentevoeten van de valuta's.

- Effecten in het Fonds kunnen moeilijk te waarderen of te verkopen zijn op het gewenste moment of tegen de gewenste prijs, vooral in extreme marktomstandigheden waarin de prijzen van activa kunnen dalen, wat het risico op beleggingsverliezen verhoogt.

- De volledige lopende kosten of een deel daarvan kunnen aan het kapitaal worden onttrokken, wat het kapitaal kan uithollen of het potentieel voor kapitaalgroei kan verminderen.

- Het Fonds kan geld verliezen als een tegenpartij met wie het Fonds handelt niet bereid of in staat is om aan zijn verplichtingen te voldoen, of als gevolg van een fout in of vertraging van operationele processen of verzuim van een derde partij.

- Naast de inkomsten kan deze aandelenklasse gerealiseerde en niet-gerealiseerde vermogenswinsten en oorspronkelijk belegd kapitaal uitkeren. Kosten, vergoedingen en uitgaven worden ook afgetrokken van het kapitaal. Beide factoren kunnen leiden tot kapitaalerosie en een kleiner potentieel voor kapitaalgroei. Beleggers moeten er ook rekening mee houden dat uitkeringen van deze aard behandeld kunnen worden (en belastbaar kunnen zijn) als inkomsten afhankelijk van hun plaatselijke belastingwetten.