Zentrale Erkenntnisse:

- Dissent at Japan’s latest monetary policy committee meeting could signal a potential policy shift, as structural wage growth compels the BoJ to consider rate hikes to prevent overheating, while helping to sustain economic progress.

- International pressure, particularly from the US, has highlighted demand for Japan to pursue a path of tighter monetary policy to address persistent inflation and support the yen.

- Japanese financial institutions, banks in particular, could be well-positioned to benefit, as rising yields boost profitability by widening net interest margins, enhancing returns on their cash reserves and bond holdings.

In recent years, dissent within the Bank of Japan’s (BoJ’s) Monetary Policy Meetings (MPMs) has emerged as a powerful signal of change. Historically, the BoJ has operated with a high degree of consensus, but when two or more board members have a differing view, it often marks a turning point towards monetary policy.

We saw signs of this in the latest September meeting, where Naoki Tamura and Hajime Takata voted for an immediate rate hike to 0.75%, against the majority’s decision to hold at 0.5%. Although we did not see a hike, the decision was accompanied by a surprise announcement from the BoJ to begin selling exchange-traded funds (ETFs) and Japanese Real Estate Investment Trusts (J-REITs). The immediate market reaction was negative on the news, but when looking at the pace of the new divestment programme it aligns with previous programmes, and the BoJ is focused on minimising the market impact. But more importantly, these ETF and J-REIT sales send a wider signal to markets, that the BoJ is keen to undertake a broader shift toward policy normalisation.

Inflation driven by structural wage growth

Latest inflation data also supports the view favouring a hike. Japan’s inflation is no longer just a transitory phenomenon. It is increasingly underpinned by structural wage growth. Japan is experiencing a long-awaited virtuous cycle of rising wages and prices, and this current cycle is supported by a tight labour market, corporate profitability, and strong domestic demand. This is supportive of a longer term and more sustainable path for inflation.

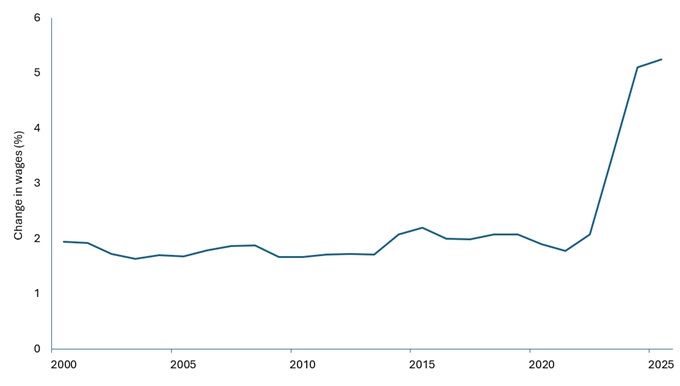

Exhibit 1 illustrates the outcomes of Japan’s annual ‘Shunto’ wage negotiations, an annual discussion held between major labour unions and employers, which highlights a growing corporate willingness to raise wages. The BoJ also uses this information to gauge whether inflation is demand driven and if hikes are justified.

Exhibit 1: Shunto wage negotiations saw a steep rise

Source: Bloomberg, Janus Henderson Investors, 2000 to 2025 Shunto wage settlements.

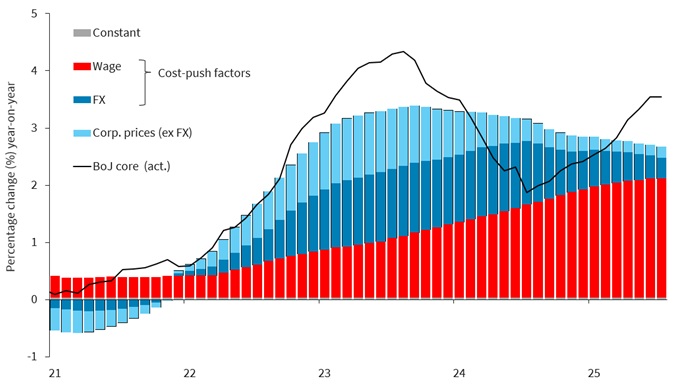

This wage-driven inflation is a departure from Japan’s deflationary past and gives the BoJ a stronger rationale to continue raising rates. With unemployment low and wage negotiations yielding meaningful increases, the central bank is under pressure to act decisively to prevent overheating.

Exhibit 2: A steady increase in wage inflation supports BoJ action

Source: MIC, BoJ, Bloomberg, Barclays Research, 1 December 2021 to 1 July 2025.

International pressure mounts

Adding to the internal momentum is external pressure, particularly from the United States. US Treasury Secretary Scott Bessent has been vocal in his criticism of the BoJ’s monetary policy stance, stating that Japan is “behind the curve” on inflation and will likely need to raise interest rates soon. In recent interviews, Bessent emphasised that Japan’s inflation challenge is both real and persistent. He argues that tighter monetary policy is essential, not only to contain price pressures, but also to support the weakening yen, which the BoJ is keen to prevent from depreciating too far.

Fazit

We believe that Japan’s economy is approaching a point where further tightening is necessary. Since the economy has managed to improve margins through mild inflation, it is crucial for both corporate profits and the capital market that this situation is maintained through appropriate monetary policy. The risk is that delaying action could lead to a bubble and subsequent burst.

So, the pattern is clear. When two or more BoJ members dissent, it often precedes a policy shift. Combined with structural inflationary forces and international pressure, Japan appears to be entering a new phase of monetary policy – one where rate hikes are not just probable, but necessary.

From an investor perspective, Japanese financial institutions are well-positioned to benefit from any tightening in monetary policy. Banks in particular stand to gain as rising yields boost profitability by widening net interest margins (charging more on loans than they pay on deposits) and enhancing returns on their cash reserves and bond holdings.

Cost-push factors: These are conditions that affect the cost of production for goods or services, such as the increased cost of raw materials, higher wages, currency depreciation, or rising taxes.

Exchange traded fund (ETF): A security that tracks an index, sector, commodity, or pool of assets (such as an index fund). ETFs trade like an equity on a stock exchange and experience price changes as the underlying assets move up and down in price. ETFs typically have higher daily liquidity and lower fees than actively managed funds.

Inflation: Teuerungsrate von Waren und Dienstleistungen in einer Volkswirtschaft. Der Verbraucherpreisindex (VPI) und der Einzelhandelspreisindex (RPI) sind zwei gängige Messgrößen für die Inflation.

Real estate investment trust (REIT): An investment vehicle that invests in real estate through direct ownership of property assets, property shares, or mortgages. As they are listed on a stock exchange, REITs are usually highly-liquid and trade like shares. Real estate securities, including REITs, may be subject to additional risks including interest-rate, management, tax, economic, environmental, and concentration risks.

Geldpolitik: Die Summe der Maßnahmen einer Zentralbank mit dem Ziel, die Inflation und das Wachstum einer Volkswirtschaft zu beeinflussen. Zu den geldpolitischen Instrumenten gehören die Festsetzung von Zinssätzen und die Steuerung der Geldmenge. Der Begriff geldpolitische Stimulierung bezieht sich auf die Erhöhung der Geldmenge durch eine Zentralbank und die Senkung der Kreditkosten. Unter geldpolitischer Straffung versteht man Maßnahmen der Zentralbanken mit dem Ziel, die Inflation einzudämmen und das Wirtschaftswachstum durch Erhöhung der Zinssätze und Reduzierung der Geldmenge zu bremsen.

Monetary-policy normalisation: The process by which a central bank returns its policy to a more standard, neutral stance, from a previously expansionary (or unconventional) position. This typically involves moving interest rates back to their long-term average, ending asset purchase programmes, and phasing out extraordinary measures put in place to stimulate or protect an economy during a crisis.

Tight labour market: An environment where there is a scarcity of available workers and a high demand for labour. This kind of market is characterised by low unemployment, where businesses are competing for talent, generally resulting in higher wages and greater bargaining power for job seekers.

Rendite: Die Höhe des Ertrags eines Wertpapiers über einen festgelegten Zeitraum, normalerweise ausgedrückt als Prozentsatz. Bei Aktien ist die Dividendenrendite ein gängiges Maß, das die jüngsten Dividendenzahlungen für jede Aktie durch den Aktienkurs dividiert. Bei einer Anleihe errechnet sich dieser aus der Kuponzahlung dividiert durch den aktuellen Anleihepreis.

Die vorstehenden Einschätzungen sind die des Autors zum Zeitpunkt der Veröffentlichung und können von den Ansichten anderer Personen/Teams bei Janus Henderson Investors abweichen. Die Bezugnahme auf einzelne Wertpapiere stellt keine Empfehlung zum Kauf, Verkauf oder Halten eines Wertpapiers, einer Anlagestrategie oder eines Marktsektors dar und sollten nicht als gewinnbringend angesehen werden. Janus Henderson Investors, die mit ihr verbundenen Berater oder ihre Mitarbeiter haben möglicherweise eine Position in den genannten Wertpapieren.

Die Wertentwicklung in der Vergangenheit ist kein zuverlässiger Indikator für die künftige Wertentwicklung. Alle Performance-Angaben beinhalten Erträge und Kapitalgewinne bzw. -verluste, aber keine wiederkehrenden Gebühren oder sonstigen Ausgaben des Fonds.

Der Wert einer Anlage und die Einkünfte aus ihr können steigen oder fallen. Es kann daher sein, dass Sie nicht die gesamte investierte Summe zurückerhalten.

Die Informationen in diesem Artikel stellen keine Anlageberatung dar.

Es gibt keine Garantie dafür, dass sich vergangene Trends fortsetzen oder Prognosen eintreten.

Marketing-Anzeige.

WICHTIGE INFORMATIONEN

Bitte lesen Sie die folgenden wichtigen Informationen zu den Fonds im Zusammenhang mit diesem Artikel.

- Aktien/Anteile können schnell an Wert verlieren und beinhalten in der Regel höhere Risiken als Anleihen oder Geldmarktinstrumente. Daher kann der Wert Ihrer Investition steigen oder fallen.

- Wenn ein Fonds ein hohes Engagement in einem bestimmten Land oder in einer bestimmten Region hat, trägt er ein höheres Risiko als ein Fonds, der breiter diversifiziert ist.

- Dieser Fonds kann im Verhältnis zu seinem Anlageuniversum oder anderen Fonds seines Sektors ein besonders konzentriertes Portfolio aufweisen. Ein ungünstiges Ereignis, das sich nur auf eine kleine Zahl von Positionen auswirkt, könnte zu einer erheblichen Volatilität oder zu erheblichen Verlusten für den Fonds führen.

- Der Fonds kann Derivate einsetzen, um das Risiko zu reduzieren oder das Portfolio effizienter zu verwalten. Dies bringt jedoch andere Risiken mit sich, insbesondere das Risiko, dass ein Kontrahent von Derivaten seinen vertraglichen Verpflichtungen möglicherweise nicht nachkommt.

- Wenn der Fonds Vermögenswerte in anderen Währungen als der Basiswährung des Fonds hält oder Sie in eine Anteilsklasse investieren, die auf eine andere Währung als die Fondswährung lautet (außer es handelt sich um eine abgesicherte Klasse), kann der Wert Ihrer Anlage durch Wechselkursänderungen beeinflusst werden.

- Wenn der Fonds oder eine währungsabgesicherte Anteilsklasse versucht, die Wechselkursschwankungen einer Währung gegenüber der Basiswährung des Fonds abzumildern, kann die Absicherungsstrategie selbst aufgrund von Unterschieden der kurzfristigen Zinssätze zwischen den Währungen einen positiven oder negativen Einfluss auf den Wert des Fonds haben.

- Wertpapiere innerhalb des Fonds können möglicherweise schwer zu bewerten oder zu einem gewünschten Zeitpunkt und Preis zu verkaufen sein, insbesondere unter extremen Marktbedingungen, wenn die Preise von Vermögenswerten möglicherweise sinken, was das Risiko von Anlageverlusten erhöht.

- Der Fonds könnte Geld verlieren, wenn eine Gegenpartei, mit der er Handel treibt, ihren Zahlungsverpflichtungen gegenüber dem Fonds nicht nachkommen kann oder will, oder als Folge eines Unvermögens oder einer Verzögerung in den betrieblichen Abläufen oder des Unvermögens eines Dritten.