Looking beyond rates to earnings

As companies adapt to higher rates and inflation moderates, Portfolio Manager Jeremiah Buckley explains why he believes earnings will now be key to market growth.

4 minute read

Key takeaways:

- Higher rates will eventually have broad impacts across the economy; however, the correlation between rates and market valuation may not be as strong as some perceive.

- Indeed, we’ve seen multiple expansion this year despite significantly higher rates – albeit driven primarily by a handful of stocks.

- Ultimately, stock prices follow earnings, and we believe several factors can drive earnings growth despite higher rates and a complicated market environment.

Like many others, we believe rates will remain structurally higher over the coming years than over the last decade, which will have considerable effects across the economy. Contrary to the mainstream sentiment, however, we think the correlation between higher rates and valuations isn’t as strong as perceived.

Will rates drive market valuation?

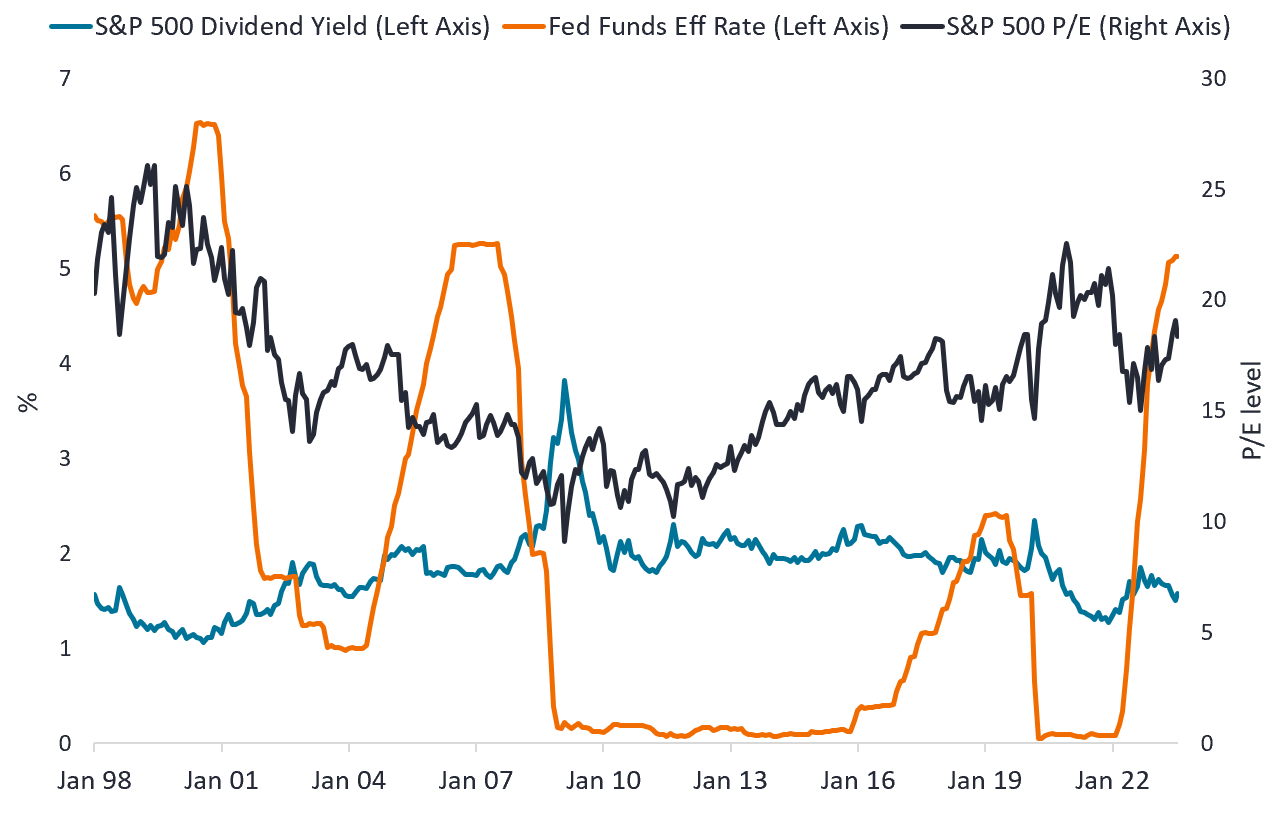

Valuations in the U.S. equity market over the last 25 years have tended to remain consistent, despite significant fluctuation in rates. The price-to-earnings (P/E) multiple on the S&P 500® Index is normally in the mid to high teens with a dividend yield of approximately 1.7 to 2%. As seen in Exhibit 1 below, both the P/E ratio and dividend yield have been in those ranges not only when the federal funds rate was close to zero, but also when it was as high as 4% to 5%.

Exhibit 1. S&P 500 P/E, S&P 500 dividend yield, and Federal Funds Effective Rate

Source: Bloomberg,as at 16 August 2023. Data from 1 January 1998 to 16 August 2023.

Source: Bloomberg,as at 16 August 2023. Data from 1 January 1998 to 16 August 2023.

Higher interest rates certainly impact demand from consumers and corporations, and the increase in financing costs has impacted our earnings estimates for 2023 and 2024. The upshot is that, based on these adjusted estimates, we think equity multiples are still in a normal historical range, despite the target fed funds rate now being much higher than a year ago.

What will fuel earnings growth?

Market performance this year, while strong, has been extremely narrow − dominated by a handful of technology stocks seen to be the likely beneficiaries of artificial intelligence (AI). While most of the market appreciation this year has been due to multiple expansion (typically, when stocks prices rise more than the corresponding movement in earnings), we believe earnings growth will be the key to market movement going forward.

To that end, companies are acutely focused on productivity, which is being enabled by technology investments (including AI) that could help reduce corporate costs. We believe that across all industries, the best companies will be able to use AI to their benefit rather than be disrupted. We see opportunities where market misperception has led to a divergence in value, and we continue to sort through the potential winners and losers related to this long-term theme.

The labor market is still healthy, and we are seeing improving labor force participation, which can help ease labor cost inflation. We see tailwinds for companies as supply chains have begun to normalize and businesses return to more usual ordering and production patterns. These factors, along with decreased material input costs, could help lower companies’ cost of goods sold and contribute to improved margins. This could present opportunity, specifically in otherwise strong long-term businesses that have suffered from recent inventory gluts.

Although we expect a volatile and bumpy ride, we are bullish on earnings growth prospects for the rest of the year and into 2024, even assuming a scenario of slow-to-flat real economic growth. If we eventually enter a recession, it will be one of the most anticipated we’ve ever witnessed, and at least some of that potential scenario is already factored into the market. Policy rates remain above what we would expect to be the long-term normal, and if we do see a material slowdown in demand, central banks have some dry powder to help stimulate growth.

Quality is key in a complex market

With more restrictive monetary policy and likely slower real growth, we believe companies with secular growth advantages will lead equity market performance. In this environment, it is important to focus on higher quality companies – those with strong capital positions and warranted pricing power.

In our view, companies that have flexibility on their balance sheet and consistency in their cash flows have an advantage over competitors that are more reliant on looser financial conditions. Furthermore, we believe companies whose products and services have created incremental value for their customers for years have earned the right to raise prices to cover inflationary costs and maintain profitability.

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

- Le Azioni/Quote possono perdere valore rapidamente e normalmente implicano rischi più elevati rispetto alle obbligazioni o agli strumenti del mercato monetario. Di conseguenza il valore del proprio investimento potrebbe diminuire.

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Il Fondo investe in obbligazioni ad alto rendimento (non investment grade) che, sebbene offrano di norma un interesse superiore a quelle investment grade, sono più speculative e più sensibili a variazioni sfavorevoli delle condizioni di mercato.

- Un Fondo che presenta un’esposizione elevata a un determinato paese o regione geografica comporta un livello maggiore di rischio rispetto a un Fondo più diversificato.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Le spese correnti possono essere prelevate, in tutto o in parte, dal capitale, il che potrebbe erodere il capitale o ridurne il potenziale di crescita.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.

- Oltre al reddito, questa classe di azioni può distribuire plusvalenze di capitale realizzate e non realizzate e il capitale inizialmente investito. Sono dedotti dal capitale anche commissioni, oneri e spese. Entrambi i fattori possono comportare l’erosione del capitale e un potenziale ridotto di crescita del medesimo. Si richiama l’attenzione degli investitori anche sul fatto che le distribuzioni di tale natura possono essere trattate (e quindi imponibili) come reddito, secondo la legislazione fiscale locale.

Specific risks

4 minute read

Key takeaways:

- Higher rates will eventually have broad impacts across the economy; however, the correlation between rates and market valuation may not be as strong as some perceive.

- Indeed, we’ve seen multiple expansion this year despite significantly higher rates – albeit driven primarily by a handful of stocks.

- Ultimately, stock prices follow earnings, and we believe several factors can drive earnings growth despite higher rates and a complicated market environment.