An economy expanding at around 8% should not raise too many concerns – particularly when that growth is visible on the ground. Compared with some other fast‑growing Asian markets, Vietnam’s headline numbers (the main growth figures used to describe the economy) feel real. Factories are busy, foreign investment continues to flow in, and many companies are delivering solid results.

During my recent visit, that contrast was clear. Vietnam and India are often talked about together because they are both large, fast-growing Asian economies, with similar headline growth rates. But the experience on the ground is very different. In Vietnam, economic activity feels tangible: businesses are investing, exports are rising, and international companies continue to commit capital. Stronger trade links with the US, and Vietnam’s growing role in supplying electronics components to countries like South Korea, Taiwan and Japan, are helping to support this momentum.

During my recent visit, that contrast was clear. Vietnam and India are often talked about together because they are both large, fast-growing Asian economies, with similar headline growth rates. But the experience on the ground is very different. In Vietnam, economic activity feels tangible: businesses are investing, exports are rising, and international companies continue to commit capital. Stronger trade links with the US, and Vietnam’s growing role in supplying electronics components to countries like South Korea, Taiwan and Japan, are helping to support this momentum.

That said, Vietnam’s growth story has made progress, but it has not been smooth. A political shake‑up and a property‑market crisis in recent years have left lasting effects. While the economy has rebounded, supply of credit from financial institutions is tighter, meaning borrowing is more expensive and harder to access. Mortgage rates are now around 10–11%, which is putting pressure on household budgets. When meeting companies, a clear and consistent message came through: consumers are feeling stretched and are spending more carefully.

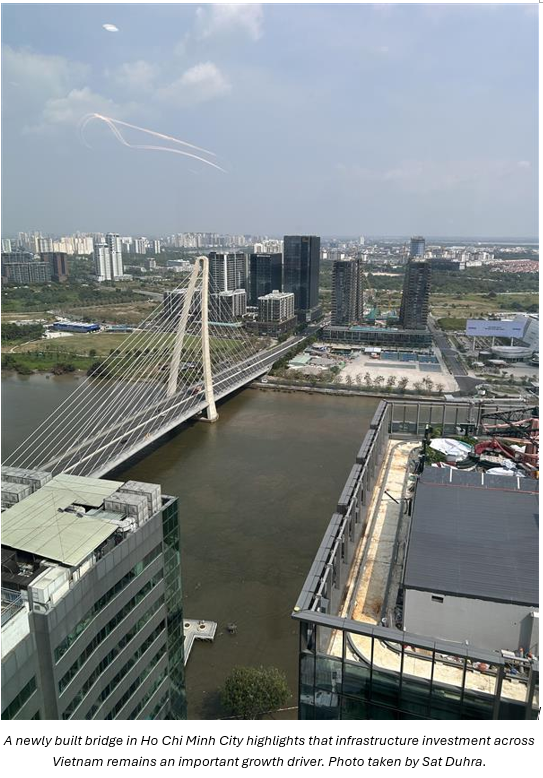

Higher interest rates and tighter controls on bank lending make it more difficult for the economy to grow quickly. As a result, the government is stepping in more actively, increasing spending on infrastructure such as roads, transport and public projects. This is likely to push the budget deficit higher following recent income tax cuts, but the aim is to support growth at a time when consumers are spending less and borrowing is more constrained.

One notable change is how government policy is being carried out. Following a series of anti-corruption measures, decision-making has become more centralised, which has helped policies move from plan to action more quickly. At the same time, there is a clear push to attract higher‑quality foreign investment, improve infrastructure, and shift the economy towards higher‑value areas such as technology and advanced manufacturing, rather than relying on lower-cost production alone.

Foreign investment remains an important support for Vietnam’s economy. The country continues to benefit from global companies looking to spread out their supply chains, particularly in electronics manufacturing. Exports are growing, and trade links with the US remain strong.

Foreign investment remains an important support for Vietnam’s economy. The country continues to benefit from global companies looking to spread out their supply chains, particularly in electronics manufacturing. Exports are growing, and trade links with the US remain strong.

However, Vietnam’s stock market still behaves like a frontier market (an earlier‑stage market) meaning there are fewer large institutional investors, shares can be harder to buy and sell, and day-to-day trading is dominated by individual investors. This means markets can move sharply at times, and overseas investors tend to pull back quickly during periods of global uncertainty. Encouragingly, regulators are making gradual improvements. Access for overseas investors is easing, and foreign ownership limits are being relaxed in some sectors.

Company valuations have also come down to more reasonable levels, making the market easier to approach than in the past. That said, much of the optimism around a potential upgrade of Vietnam’s market status is already reflected in share prices. As a result, Vietnam no longer feels like the clear “must own” destination it once was, and investors are being more selective.

From an investment perspective, there are still plenty of opportunities in Vietnam – but knowing where to look matters. These tend to be found in well-run banks, businesses linked to infrastructure spending, and selected consumer companies that could benefit as conditions improve. That said, caution remains important. Recent political uncertainty and property market problems were a reminder that Vietnam is still a frontier market, meaning it can be more volatile and less predictable during periods of stress.

Vietnam remains an interesting long‑term story, but one that now requires more selectivity and patience. Strong economic growth on its own is not enough to guarantee good investment outcomes. As ever, we will continue to focus on quality businesses, balance sheets, and the sustainability of returns, and keep a close eye on how this fast‑growing economy navigates its next phase.

Important information

Henderson Far East Income Limited (the ‘Company’), is a Jersey domiciled closed-ended investment company (a ‘Fund’), with registered offices at IFC1, The Esplanade, St Helier, Jersey, JE1 4BP. The fund is regulated by the Jersey Financial Services Commission.

Not for onward distribution. Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser. This is a marketing communication. Please refer to the AIFMD Disclosure document and Annual Report of the AIF before making any final investment decisions. Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the law change. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), Tabula Investment Management Limited (reg. no. 11286661), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 78, Avenue de la Liberté, L-1930 Luxembourg, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

Janus Henderson® and any other trademarks used herein are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.