For many UK investors, portfolios are naturally focused on what is familiar – UK companies and well-known US names. Both have clear strengths and play an important role in long-term investing.

But focusing only on these markets can mean missing out on a much wider set of opportunities.

Europe offers a way to build on what you already own – adding breadth, diversification, and new sources of growth.

Across its developed markets, Europe spans 14 countries and is home to some of the world’s most innovative and specialised economies. From German engineering and Swiss healthcare to Nordic technology and Dutch industrial expertise, the region offers exposure to a broad range of industries and end markets.

You’re not just buying more of the same – you’re gaining access to a broader mix of businesses and industries, helping to spread risk and create new opportunities for growth.

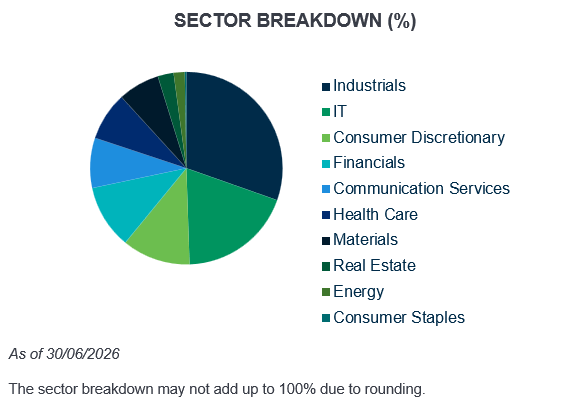

Want to learn how ESCT puts this opportunity set into practice? Explore the trust’s current portfolio holdings and discover the businesses the team believes are well placed to benefit from Europe’s long-term growth opportunities.

Because Europe has a more balanced sector mix, its stock market is not reliant on just a few companies or industries to drive performance.

Because Europe has a more balanced sector mix, its stock market is not reliant on just a few companies or industries to drive performance.

This can matter over time. Markets behave differently depending on economic conditions, and different sectors come into favour at different points in the economic cycle.

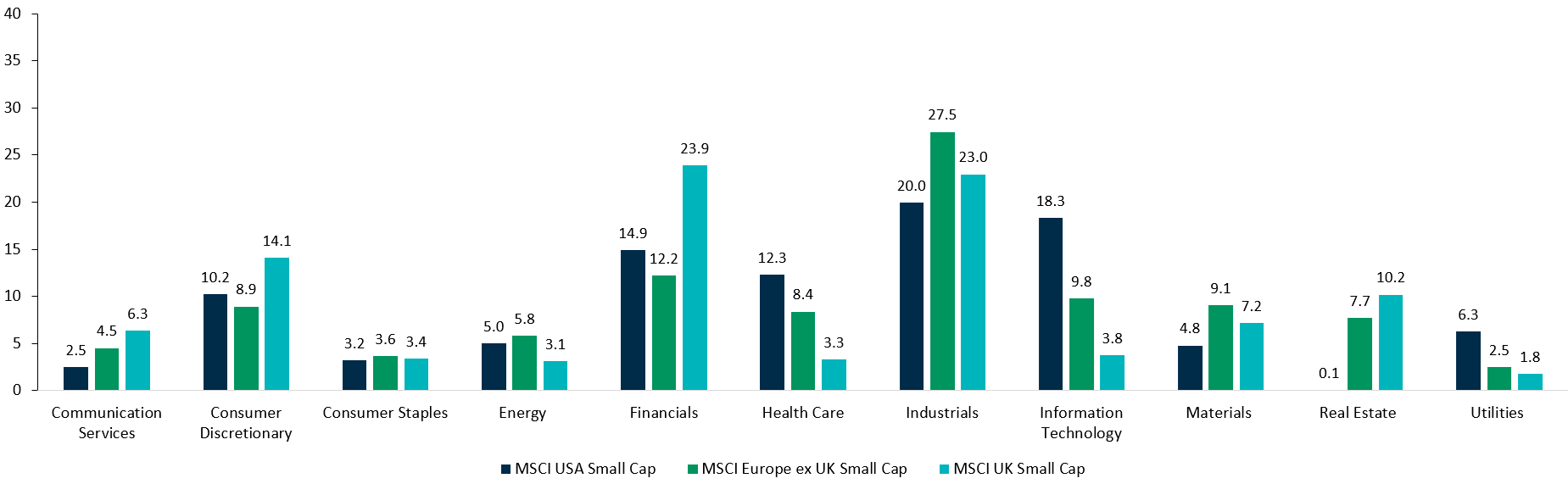

Europe’s smaller-company market offers a different sector profile to both the UK and the US, providing investors with access to a wider range of industries and growth drivers.

Source: Bloomberg June 2026

ESCT builds on this broad opportunity set by investing selectively in the areas where the managers find the most attractive long-term prospects.

Source2: ESCT at: Portfolio | The European Smaller Companies Trust plc

Adding Europe can help smooth the journey of a portfolio, as returns are driven by a wider set of factors.

Europe is sometimes seen as made up of older, more established industries. In reality, many European companies are at the forefront of long-term structural changes.

These include:

- The transition to cleaner energy – companies such as TKH Group and Gaztransport & Technigaz, whose technologies support electrification, improve energy efficiency and enable the shift towards lower‑carbon energy sources

- Advances in industrial automation – SUSS MicroTec, whose technologies help manufacturers automate production and produce the advanced semiconductors needed for next-generation industries

- Modernising digital infrastructure – Smartoptics, whose networking solutions help support the growing demand for high-capacity, efficient data connectivity.

Improving access to financial markets – flatexDEGIRO, which is helping to make investing more accessible to individual investors through its digital brokerage platform.

- Demand for high-quality global brands – companies such as IG Group and Van Lanschot Kempen, whose established platforms and reputations continue to attract a growing international client base

Many of these businesses operate globally, even if they are headquartered in Europe.

You’re gaining exposure to long-term growth themes that are shaping the global economy.

While many investors know Europe’s largest companies, much of the region’s potential lies below the surface.

Smaller companies, in particular, often operate in specialist areas and can be leaders in their niche – yet they may be less widely followed by analysts and investors. Many supply essential products, services or technologies that larger industries rely on while occupying strong market positions. These businesses are often deeply embedded within global supply chains despite their relatively low profile with investors.

Smaller companies, in particular, often operate in specialist areas and can be leaders in their niche – yet they may be less widely followed by analysts and investors. Many supply essential products, services or technologies that larger industries rely on while occupying strong market positions. These businesses are often deeply embedded within global supply chains despite their relatively low profile with investors.

European smaller companies are also typically at an earlier stage of their development than the region’s largest listed businesses. With the average company in the MSCI Europe ex UK Small Cap Index valued at around €1 billion, many are still expanding into new markets, investing in innovation and building long-term competitive advantages.

There is more scope to discover opportunities that may not yet be fully recognised by the wider market.

Find out how ESCT uncovers Europe’s hidden growth engines. Read more about the team’s investment approach and the types of businesses they look for across Europe.

Learn about ESCT’s investment approach

Investing in Europe isn’t about replacing UK or US holdings – it’s about complementing them.

By adding European exposure, investors can:

- Access a wider range of companies and more diversified mix of industries

- Reduce reliance on a narrow set of market drivers

- Tap into global growth trends

- Discover opportunities beyond the most familiar names

- Gain exposure to a part of the market that represents around 14% of Europe’s investable market capitalisation1 but is overlooked by global large-cap indices

Europe complements the UK by adding breadth and new sources of growth. For investors looking to build a more balanced portfolio, it can offer a different way to grow wealth – one that looks beyond what they already know, and towards a broader set of opportunities.

1 Source: MSCI Europe ex United Kingdom Small Cap Index

2 Disclaimer: Exposures and allocations are subject to change without notice.