Key takeaways:

- Shipping disruption has raised Asia to Europe trade costs and increased delays, effectively acting as a tariff that favours European chemical producers with regional supply chains and more reliable delivery.

- Reduced Asian competition has supported European high yield chemical pricing and cash flow, which is driving spread tightening and contributing to improving performance from the sector.

- Benefits are uneven, however, and volatility around pricing means it remains important to analyse the fundamentals of each issuer.

The high yield bond market is often viewed through the lens of aggregate credit spreads, but this masks significant dispersion beneath the surface. While much current attention is focused on areas of intense activity, notably artificial intelligence (AI)-linked credits and technology-adjacent capital expenditure themes, opportunities also emerge from exogenous shocks, particularly geopolitical developments that reshape industry economics in unexpected ways. In 2026, persistent disruption to global shipping routes represents one such shock, creating a tactical opportunity within European high yield chemicals.

Shipping disruption has reshaped chemical trade economics

Geopolitical instability has made trade in chemicals between Asia and Europe more expensive and less reliable. Disruptions in the Red Sea and Suez Canal since 2023, intensified in early 2026 by the closure of the Strait of Hormuz, have lengthened transit times and increased fuel and insurance costs.

For bulk chemicals, polymers and plastics, where freight is a key part of delivered cost, exports from Asia to Europe have become less economical. European chemical producers are somewhat shielded from these disruptions. Their supply chains are mostly regional, avoiding long haul shipping risks. Shorter lead times, greater reliability and lower working capital risk have become real competitive advantages, allowing European suppliers to defend pricing and win volumes previously met by imports. In effect, shipping disruption now acts like a tariff, favouring domestic European production.

This advantage exists despite Europe’s well-known issues of high energy costs, regulation and overcapacity. In the current environment, logistics resilience and certainty of supply temporarily outweigh these drawbacks, creating a tactical opportunity for better positioned European issuers.

Credit relevant transmission channels

The benefits have been most visible in commodity chemicals and polymers, where freight intensity is high and substitution is feasible. European customers across automotive, pharmaceuticals and construction have increasingly prioritised local sourcing to mitigate logistics risk, while longer Asia-origin lead times have encouraged domestic inventory rebuilding. At the same time, Asian competitors face difficult choices between absorbing higher shipping costs or passing them through, narrowing their historical cost advantage versus European producers.1

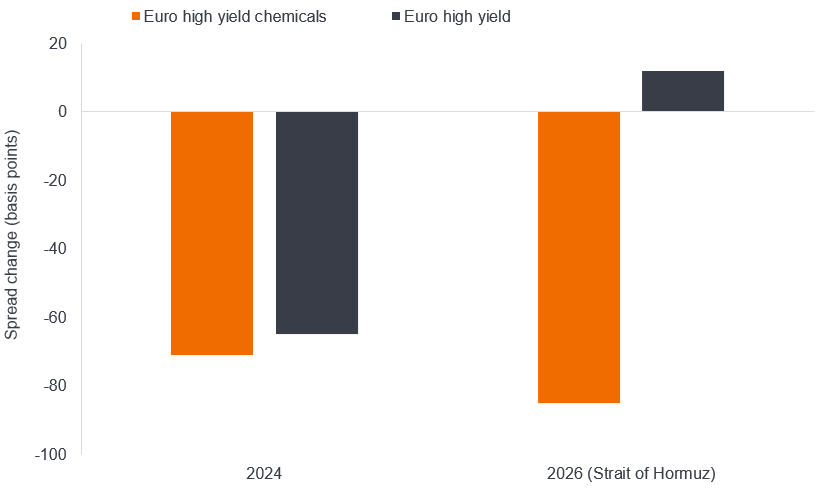

Similar dynamics were already evident during the shipping disruptions of 2024 (Red Sea Houthi attacks, US port disputes), when reduced Asian competition in Europe supported volumes, pricing and cash flow, particularly in aromatics and basic polymers.2 Credit markets responded accordingly, with European high yield chemical bonds generally outperforming the broader high yield index as earnings visibility improved. The outperformance is shown in credit spreads declining.

Spread movements during shipping disruptions (Euro high yield chemicals sector v Euro high yield)

Source: Janus Henderson, Bloomberg, ICE BofA Euro High Yield (Chemical sector), ICE BofA Euro High Yield Index (all sectors). Option-adjusted spread, basis points, as at May 2026. 2024 = calendar year, 2026 (27 Feb 2026 to 31 April 2026). One basis point equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%. Past performance does not predict future returns.

Issuer level outcomes reinforce the dispersion. Distressed bonds such as Synthomer’s have seen partial recovery as import competition has eased and cash flow expectations stabilise.3 Larger players with European asset concentration, including INEOS, may benefit from reduced APAC and Middle East exports into Europe. To put recent developments into context, INEOS management guided that earnings before tax, depreciation and amortisation (EBITDA) is set to be circa €400 million for the month of April 2026 alone, which is almost identical to what it earned over the previous three months (€426m).4

Even diversified producers such as Tronox noted that supply constraints affecting competitors is providing support to European pigment pricing, despite ongoing cost and demand uncertainty.5

European high yield chemical issuers remain structurally fragile6, but relative positioning has improved versus globally-exposed competitors. Sustained shipping disruption has raised the premium investors place on customer proximity and supply chain reliability, creating a temporary but credit relevant earnings buffer for regionally-anchored producers. This is precisely the type of opportunity that is easy to miss at the index level, but powerful when analysed issuer by issuer.

We believe the current disruption, though likely temporary, may spur EU anti-dumping measures to be implemented to help support regional production. A consequence of last year’s tariff war between the US and China was that chemical exports destined for each other ended up diverted to Europe, adding to pressures on domestic European producers. With European producers typically operating in a more regulated environment further protective measures like safeguarding (responding to a surge in imports), should help European chemical producers stay competitive once the environment normalises.

1Source: Bloomberg Intelligence, March 2026

2Source: INEOS, Lanxess earnings announcements, 2024.

3Source: Bloomberg, Synthomer 7.375% 2029 bond price 27 February 2026 to 18 May 2026.

4Source: BofA, INEOS Group Holdings 2026 Investor Day, 18 May 2026.

5Source: Tronox, Q1 2026 results and outlook, 6 May 2026.

6Source: Bloomberg, BofA, Leverage across major names remain elevated at around 2.5x-12.9x, 18 May 2026.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Capital expenditure (capex): Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment or vehicles in order to maintain or improve operations and foster future growth.

Cash flow: The net balance of cash that moves in and out of a company. Positive cash flow shows more money is moving in than out, while negative cash flow means more money is moving out than into the company.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit rating: An independent assessment of the creditworthiness of a borrower by a recognized agency such as S&P Global Ratings, Moody’s or Fit.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Dumping: The practice of exporting goods at prices lower than in the domestic market. It is viewed as an unfair pricing strategy in international trade.

Exogenous shock: An unexpected or unpredictable event that occurs outside an industry or country, but can cause significant change within it.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

Investment grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Issuer: The borrowing (issuing) company that makes bonds available to investors, typically through a sale of bonds to the public or financial institutions.

Polymer: A very large molecule constituted of repeating subunits of monomers joined together. Polymers can be synthetic (man-made) plastics or natural.

Tariff: A duty or tax imposed on goods entering a country.

Volatility: A measure of risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

Working capital: The money needed to finance day-today operations.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For a bond, at its most simple, this is calculated as the coupon payment divided by the current bond price.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.

Specific risks

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- CoCos can fall sharply in value if the financial strength of an issuer weakens and a predetermined trigger event causes the bonds to be converted into shares/units of the issuer or to be partly or wholly written off.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- Emerging markets expose the Fund to higher volatility and greater risk of loss than developed markets; they are susceptible to adverse political and economic events, and may be less well regulated with less robust custody and settlement procedures.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- CoCos can fall sharply in value if the financial strength of an issuer weakens and a predetermined trigger event causes the bonds to be converted into shares/units of the issuer or to be partly or wholly written off.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.