Global bonds navigator: piloting a soft landing

Sustaining growth while taming inflation is the navigation challenge facing central banks. The Global Bonds Team model how different fixed income sectors could fare in various scenarios.

8 minute read

Key takeaways:

- Our inaugural report follows the worst start to a year for fixed income markets and comes amid continued uncertainty about the pace at which central banks will raise interest rates to address inflation.

- We expect near-term inflation outcomes to be tied in part to the conflict in Ukraine, which has the potential to trigger a deeper global recession should Russia cut off its gas supply to Europe.

- On the other hand, its resolution would provide the ‘goldilocks’ scenario that would see the global economy continue to grow without the prospect of need for drastic monetary intervention from central bankers looking to tame inflation.

Welcome to the first edition of our bond market forecast analysis. This report is based on the scenario analysis run by the Global Bonds Team to guide asset allocation decisions. Each report tries to assess the expected returns potentially delivered by the major fixed income sectors based on a range of modelled outcomes (see appendix for a full description of our methodology).

Treading a fine line between policy error and soft landing

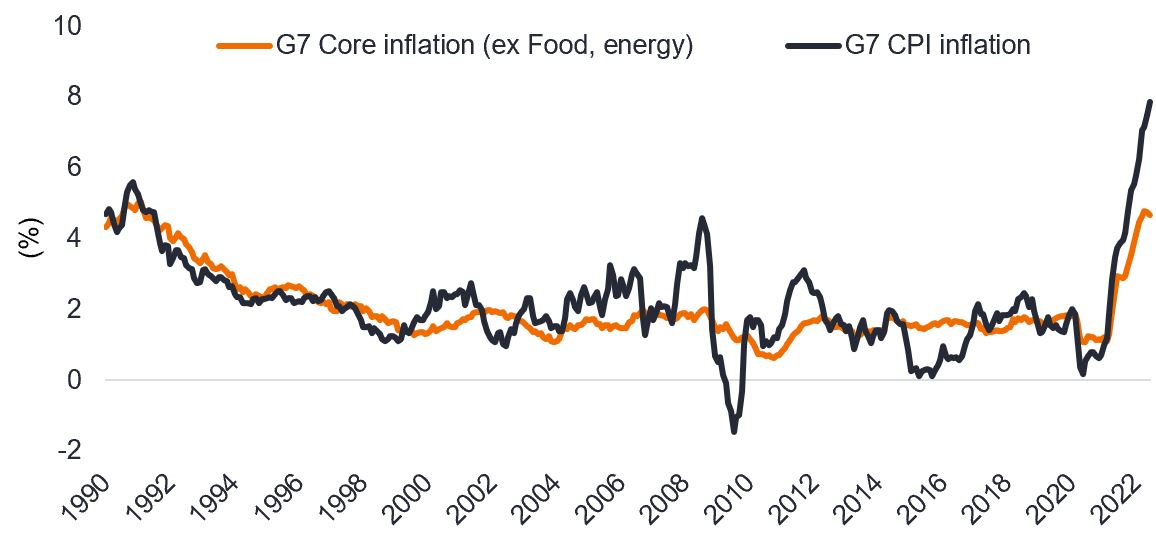

After the worst start to the year in history, things can only get better. Right? But with more hawkish language from central banks and growth starting to fade, the global economy is now treading a very fine line between policy error and soft landing. The chance of policy error has grown over recent months as central bankers have had to aggressively hike rates to try and tame inflation. But have we forgotten monetary policy usually works with a lag? Although inflation has continued to beat expectations, there are now numerous indicators signalling a reduction of the supply/demand imbalance that had stoked prices since the pandemic. Freight rates are falling dramatically – with new ships and capacity all expected to step up next year – while commodity prices are in decline, and finally, the PMI and ISM surveys have started to indicate economic output is slowing around the world.

Figure 1: Inflation remains stubbornly high with energy and food as key drivers

Source: Janus Henderson Investors, Bloomberg, as at 30 June 2022. Notes: OECD major seven economies CPI.

The conflict in Russia continues to cloud the economic outlook, however. Should Russia follow through on threats to cut off gas to Europe, the resulting chilling effect on growth would be felt globally.

Scenarios considered

We adopt a scenario-driven approach to identify the relative attractiveness of fixed income sectors. Our aim is not to perfectly forecast returns to the nearest basis point (as that is not possible), but to understand the range of return outcomes and gauge the resilience of that performance across probable growth scenarios.

Our base case over the next 12 months to end of June 2023 is that the global economy enters a recession largely due to the conflict in Ukraine and weakening consumer spending as real incomes are eroded by inflation, with labour market pressures moderating. In the US for example, we model core inflation peaking in September and falling to around 3.3% at the end of the period, limiting the need for additional rate hikes in 2023.

Overall, the chances of more growth lengthening this current growth cycle are looking increasing unlikely. To put this in context, we only see a one in three chance of either of our two growth scenarios materialising.

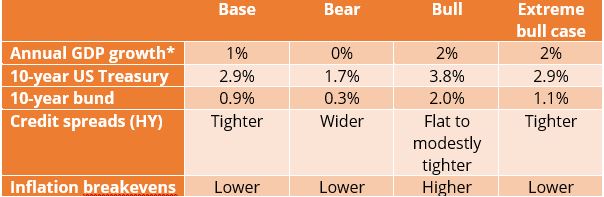

Base case (shallow recession):

- Growth slows to a standstill as consumers curtail spending due to falling real incomes.

- Inflation (core personal consumption expenditure) peaks in the third quarter of 2022 and starts to taper off to 3.3% at the end of the period.

- Unemployment starts to pick up near the end of our 12-month forecast horizon.

- After continuing to hike over the third quarter, central bankers start to dial back their hawkish tone in the face of slowing growth. While risk assets perform in this scenario, default rates and liquidity premia have been lifted. Much of the positive returns for risk assets is a function of the wide starting point for spreads.

Bear case (deeper recession):

- Global recession that hits Europe especially hard (-1% for EU and 0% for US over the year) due to energy market supply shocks triggered by the Russia-Ukraine conflict.

- Unemployment rises much higher than our base case.

- Markets roll back their interest rate expectations as central bankers pause hikes and quantitative tightening to head off slowing growth. Credit spreads are volatile and defaults rise, especially in the high yield sector.

Bull case (high pressure economy):

- Growth continues to remain buoyant, which puts upward pressure on wages and causes inflation to settle higher at the end of our forecast horizon.

- Strong labour markets and resilient inflation forces central banks to continue to raise rates.

- Elevated market volatility transpires as more hikes are priced in, while risk asset performance is mixed. Investment grade (IG) assets underperform on a higher rate scenario, but high yield (HY) and lower duration-sensitive assets perform on better growth.

Extreme bull case (armistice):

- Growth picks up and the global economy largely avoids falling into a recession, as Russia-Ukraine conflict settles down, triggering some sanction relief on specific commodities.

- Inflation moderates as commodity prices fall from recent highs.

- Central bankers initially continue to raise rates but back off from tightening due to less inflationary pressures. Risk assets benefit from the fall in conflict-driven uncertainty.

Figure 2: Expected fair values and key economic variables by scenario

Source: Janus Henderson Investors, 21 July 2022. *Average for US/EU GDP growth over the 12-month period. There is no guarantee that past trends will continue, or forecasts will be realised.

Significant lift in forward-looking returns

2022 has been the worst start to any year on record for fixed income total returns. Nevertheless, rate hikes and wider credit spreads have significantly improved forward-looking returns (as shown by the positive expected returns in the base case scenario). Moreover, there is currently no single asset class that particularly stands out as being particularly mispriced. As such, we see benefits in asset diversification at this point in the economic cycle, not least given the uncertainties around economic outcomes and central bank policy.

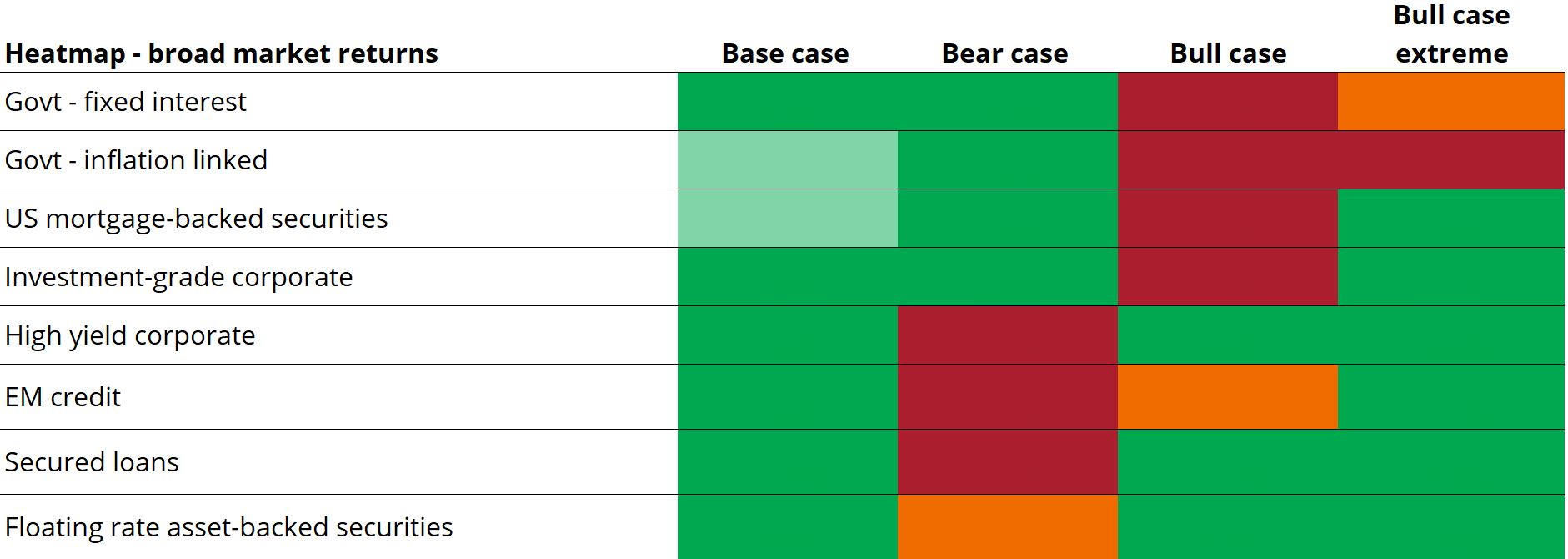

Figure 3: 12-month fixed income sector return outlook

Legend: 1-year sector return estimates (%) in each scenario

Source: Janus Henderson Investors, as at 21 July 2022. Note:*Bull (bear) refers to a positive (negative) outturn for economic performance. Expected returns for a US dollar-based investor, based on index returns before allowance for alpha. Any differences among portfolio securities currencies, share class currencies, and your home currency will expose you to currency risk. The above are the portfolio managers’ views and should not be construed as advice and may not reflect other opinions in the organisation. There is no guarantee that past trends will continue, or forecasts will be realised.

Key findings:

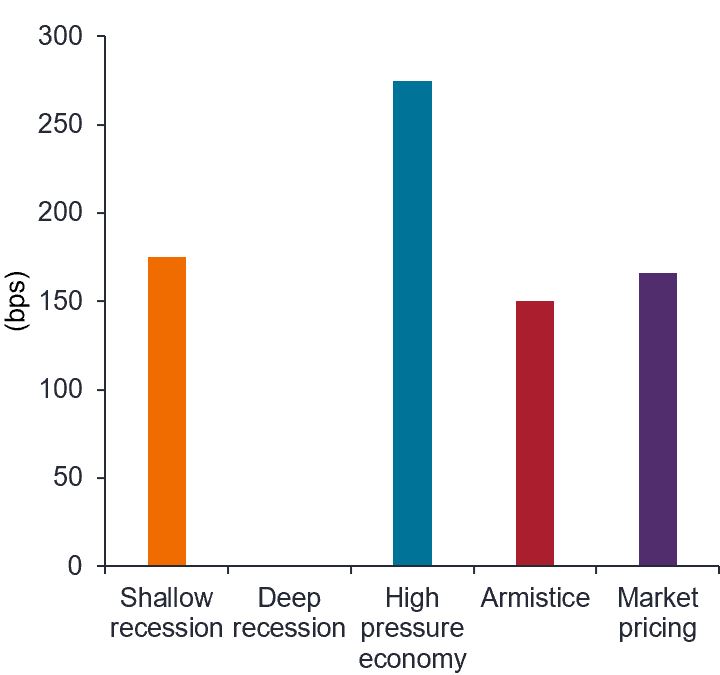

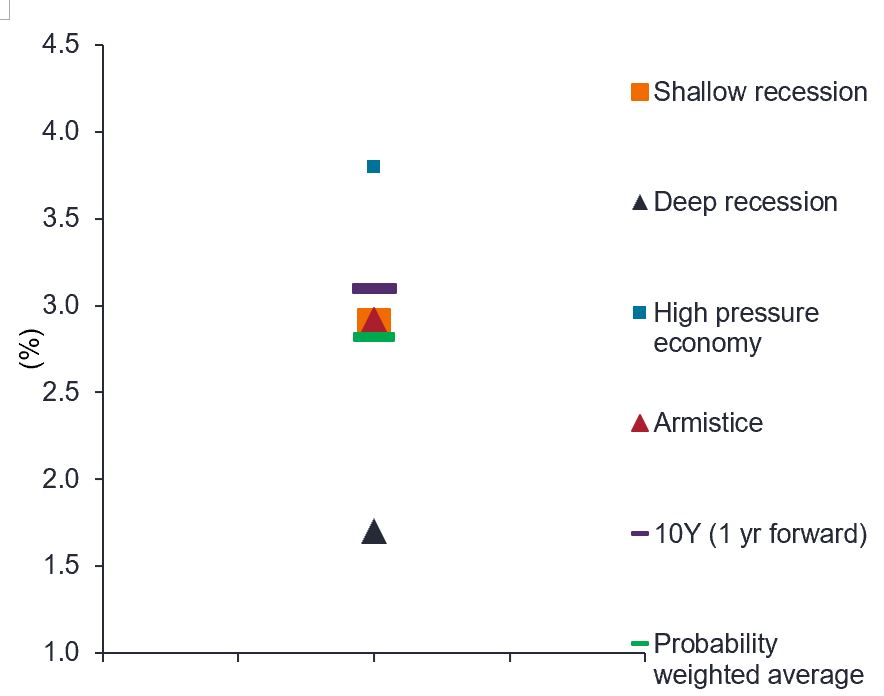

- Core government bond duration has a greater role to play in portfolios. In three out of four scenarios, central bank rate hikes are at or below what is priced in over next 12 months, as shown for the US in figure 4 (except for extreme bull case scenario). This suggests that on balance, there is room for shorter-term bonds, in particular, to outperform as aggressive rate expectations fail to materialise. On a probability weighted basis, the weighted average yield for the 10-year Treasury is 2.8% in the US (figure 5) and 0.9% in Germany, which is lower than what is priced into the swap markets at time of writing1.

Figure 4: US Fed rate hikes over next 12 months (bps)

Note: no rate hikes are expected in the ‘Deep recession’ scenario.

Source: Janus Henderson Investors, 21 July 2022. There is no guarantee that past trends will continue, or forecasts will be realised.

Figure 5: US 10‑year Treasury yield forecast by scenario (%)

Source: Janus Henderson Investors, 21 July 2022. There is no guarantee that past trends will continue, or forecasts will be realised.

- Higher quality assets – such as Agency MBS, investment grade assets and government bonds – are beneficial in a slower growth environment (in both a shallow and deep recession), providing resilient returns in all but the bull case, the more severe inflation scenario (where the longer duration of some of these markets continues to act as a drag).

- On a regional basis, European investment grade, government and high yield bonds are on average more likely to outperform US counterparts in the modelled scenarios (on a currency hedged basis) due to the wider starting level of spreads and lower neutral level of interest rates2.

- Senior floating rate asset-backed securities (ABS) continue to offer resilience across the scenarios, but less upside in returns overall; so can continue to play a role as a defensive ‘carry’ asset.

Diversification is key

Considering the recent sell-off, our base case favours a broad investment mix, predicated on the yields now on offer and the benefits of diversification to mitigate risk and enhance potential returns. Although we think returns will be more challenging should the global economy fall into a deep recession, we see potential for corporate and government bonds to deliver mid-single digit returns in our base case.

What we are watching for:

- Inflation trends: the Fed will not pivot towards looser policy, in our view, until we see a clear and persistent change in inflation. The August CPI print will be critical given the downside surprise in the July print.

- Growth trajectory: leading indicators of economic activity (eg, PMIs) to provide a gauge on the speed of the growth slowdown; whether in the US, the ISM services PMI (July = above trend growth of 56.7) will ‘catch down’ to the S&P services PMI (July= a recessionary 47.3). Further yield curve inversion at the front end of the yield curve (a recessionary signal).

- Market behaviour: measures of market volatility such as VIX and MOVE3, to subside over the third quarter, which provides some period of stability in credit spreads in the second half of the year in the base case.

Footnotes

1 Source: Bloomberg, according to the US Treasury Actives Curve and EUR German Sovereign Curve as at 12 August 2022.

2 This is the rate that supports the economy at full employment while keeping inflation constant.

3 VIX is a measure of the stock market’s expectation of volatility based on S&P 500 index. MOVE measures Treasury rate volatility through options pricing.

Quantitative easing (QE): A form of monetary policy used by central banks to restrict the economy by reducing the amount of overall money in the banking system.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Mortgage-backed securities (MBS) may be more sensitive to interest rate changes. They are subject to extension risk, where borrowers extend the duration of their mortgages as interest rates rise, and prepayment risk, where borrowers pay off their mortgages earlier as interest rates fall. These risks may reduce returns.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Carry is the excess income earned from holding a higher yielding security relative to another.

A yield curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

Credit spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Volatility measures risk using the dispersion of returns for a given investment.

Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics.

10-Year Treasury Yield is the interest rate on U.S. Treasury bonds that will mature 10 years from the date of purchase.

Methodology – asset class level projections

We use a scenario-based approach to model potential outcomes over a 12-month horizon. Rather than rely on single point estimates, we think it is important to consider the distribution of potential outcomes based on probable future economic scenarios. This approach helps us better understand the distribution of potential outcomes and avoids biases based on a single-deterministic path.

In each scenario, we define expectations of key economic variables such as GDP growth, inflation, exchange rates, central bank rates and key tenor points on the yield curve, for the major economic blocs.

Government bond returns are estimated by calculating a fair value yield, taking into account the expected path of central bank rates and, the neutral rate, for each scenario. The total return is calculated by combining the coupon income and the likely price impact of the scenario yield estimates.

Inflation-linked bond returns are assessed by considering outcomes for breakeven inflation alongside nominal rates (outlined above), which gives an implied change in real yield. This is then used to calculate expected returns.

For credit asset classes, we assume expected issuer default rates in each scenario. We project returns by combining nominal rates (at the appropriate maturity) and the estimated change in credit market spread, adjusted for expected default losses and liquidity premia.

Returns are projected on a currency hedged basis, assuming 12-month forward FX hedging to base.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall. High yielding (non-investment grade) bonds are more speculative and more sensitive to adverse changes in market conditions.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- Emerging markets expose the Fund to higher volatility and greater risk of loss than developed markets; they are susceptible to adverse political and economic events, and may be less well regulated with less robust custody and settlement procedures.

- The Fund may invest in onshore bonds via Bond Connect. This may introduce additional risks including operational, regulatory, liquidity and settlement risks.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- CoCos can fall sharply in value if the financial strength of an issuer weakens and a predetermined trigger event causes the bonds to be converted into shares/units of the issuer or to be partly or wholly written off.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

8 minute read

Key takeaways:

- Our inaugural report follows the worst start to a year for fixed income markets and comes amid continued uncertainty about the pace at which central banks will raise interest rates to address inflation.

- We expect near-term inflation outcomes to be tied in part to the conflict in Ukraine, which has the potential to trigger a deeper global recession should Russia cut off its gas supply to Europe.

- On the other hand, its resolution would provide the ‘goldilocks’ scenario that would see the global economy continue to grow without the prospect of need for drastic monetary intervention from central bankers looking to tame inflation.