Key takeaways:

- After largely tracking the U.S. tech sector through much of 2025, international technology stocks decoupled late in the year, meaningfully outperforming U.S. peers.

- The data point to robust earnings growth, not multiple expansion, as the primary driver. Valuations across non-U.S. technology actually compressed as prices rose.

- The technology landscape outside the U.S. is heavily weighted toward firms at the center of the AI infrastructure buildout. With valuations still deeply discounted to the U.S., we think international markets offer good hunting ground for leading tech companies that stand to benefit from accelerating AI investment rather than be disrupted by it.

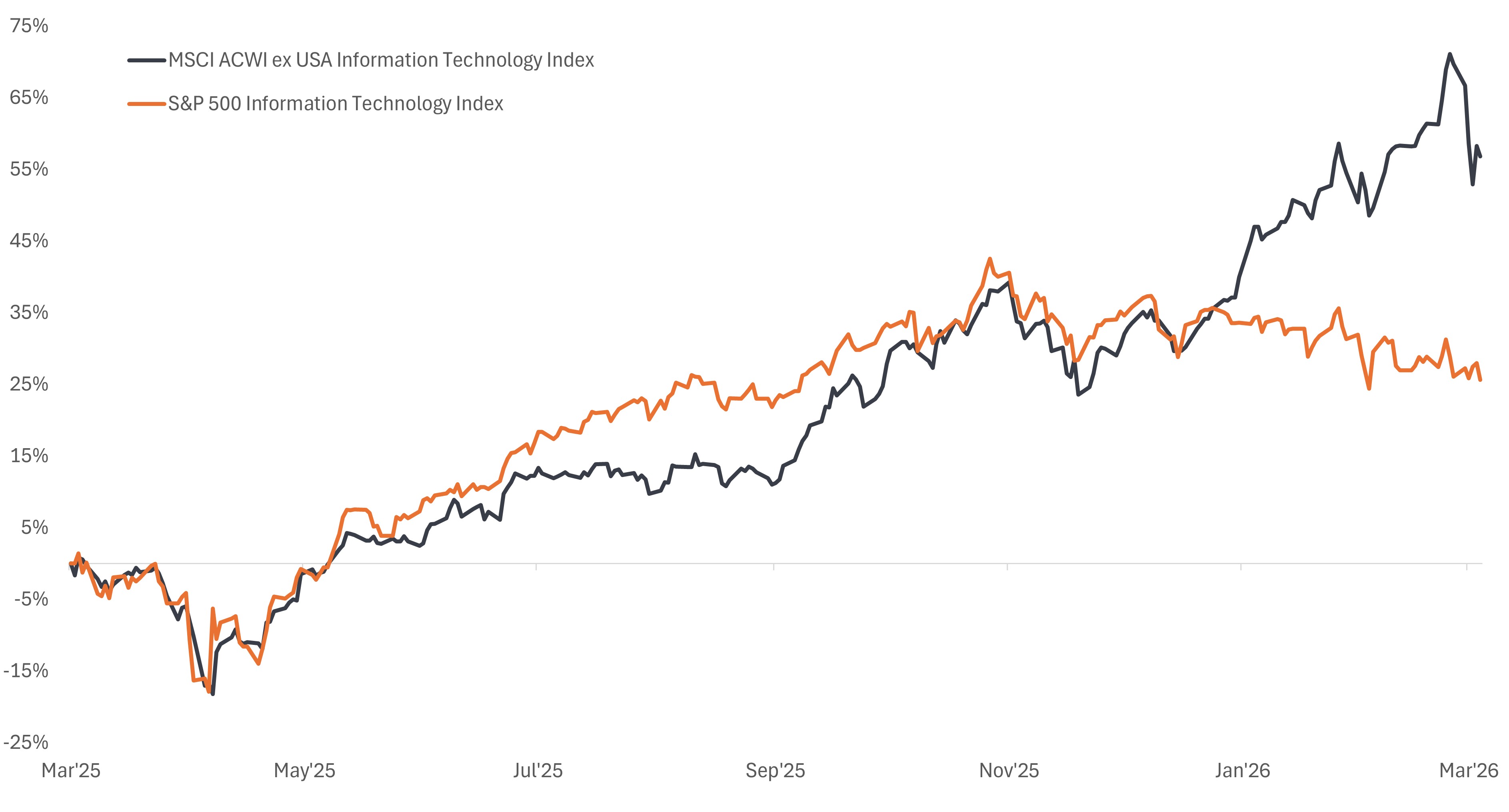

After roughly tracking the U.S. tech sector through much of 2025, international technology stocks staged a notable breakout at the end of the year. While U.S. tech traded sideways-to-lower through February 2026 amid concerns about hyperscaler capital spending (and related funding and monetization scrutiny) as well as the threat of business-model disruption from agentic AI, the MSCI ACWI ex USA Information Technology (IT) Index moved sharply higher (Exhibit 1). For investors used to viewing U.S. mega-caps as the default expression of technology exposure, this divergence warrants a closer look.

Exhibit 1: International technology stocks have decoupled from U.S. peers

Price performance, 3 March 2025 to 6 March 2026.

Source: Bloomberg, data from 3 March 2025 to 6 March 2026. MSCI ACWI ex USA Information Technology Index, S&P 500® Information Technology Index. Past performance does not predict future results.

Strong earnings have underpinned the rally

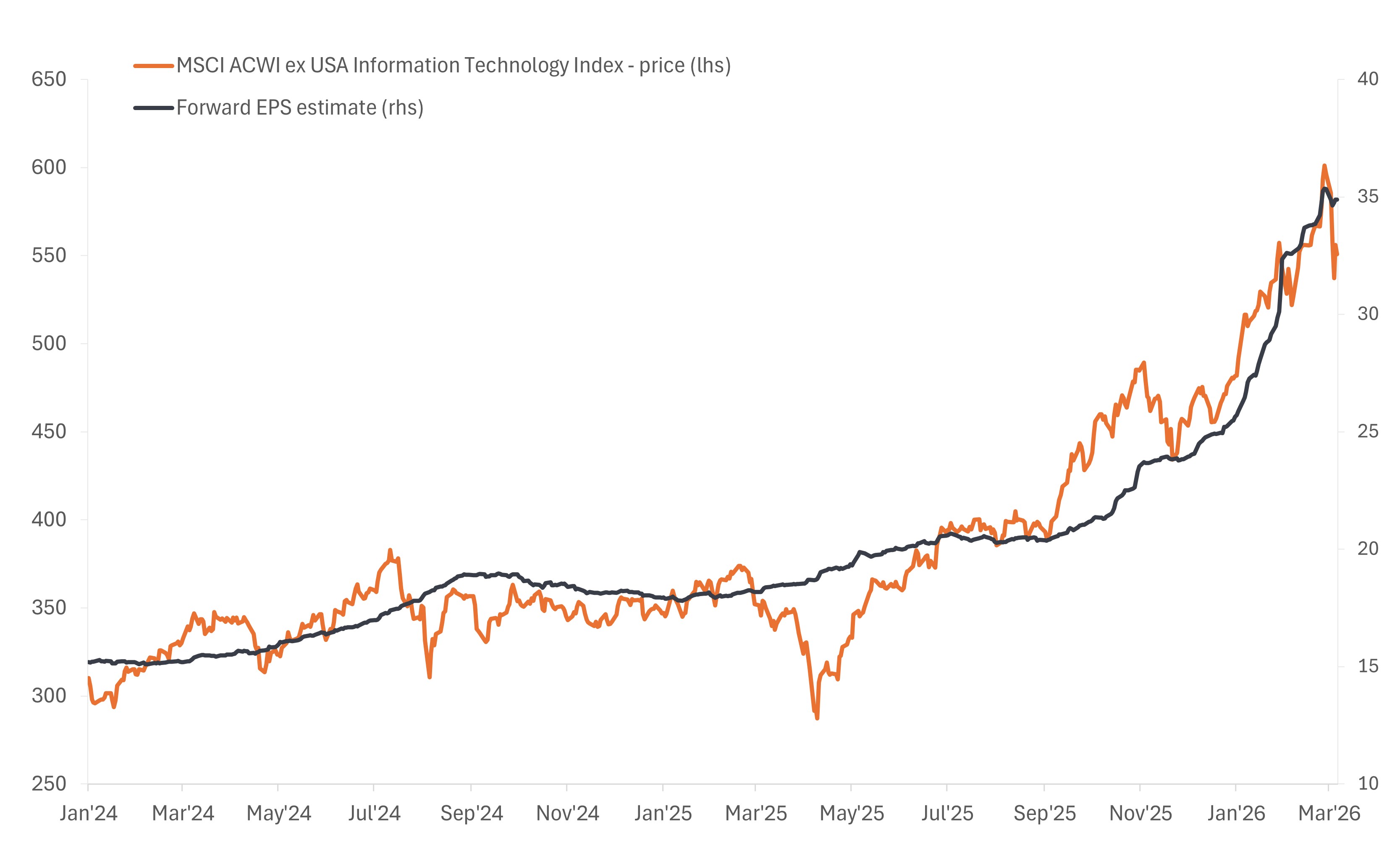

Given the magnitude of the rally, one might assume it had been driven by multiple expansion – share prices getting ahead of fundamentals. However, the data tells a different story: It points to earnings growth as the primary driver, with the rise in stock prices accompanied by an equally powerful move in analyst estimates.

Exhibit 2: Earnings growth has been a key driver behind the recent rally

Next 12-month forward earnings estimates have kept pace with the rise in share prices.

Source: Bloomberg, data from 1 January 2024 to 6 March 2026. Past performance does not predict future results.

These upward revisions have been fueled largely by sustained AI infrastructure investment, which has extended beyond hyperscalers to enterprise customers and sovereign-backed initiatives. The rising demand for computing power has also supported a renewed upcycle in the memory market, where tight supply has pushed prices higher and quickly translated into realized revenues.

Unlike the U.S., where software firms comprise a large share of the technology sector, overseas markets are disproportionately weighted toward the “picks and shovel makers” at the heart of the AI infrastructure buildout. Most of the leading memory chipmakers and many of the most critical semiconductor equipment and wafer manufacturers are listed outside the U.S., predominantly in Taiwan, South Korea, Japan, and the Netherlands.

Earnings growth has kept valuations in check

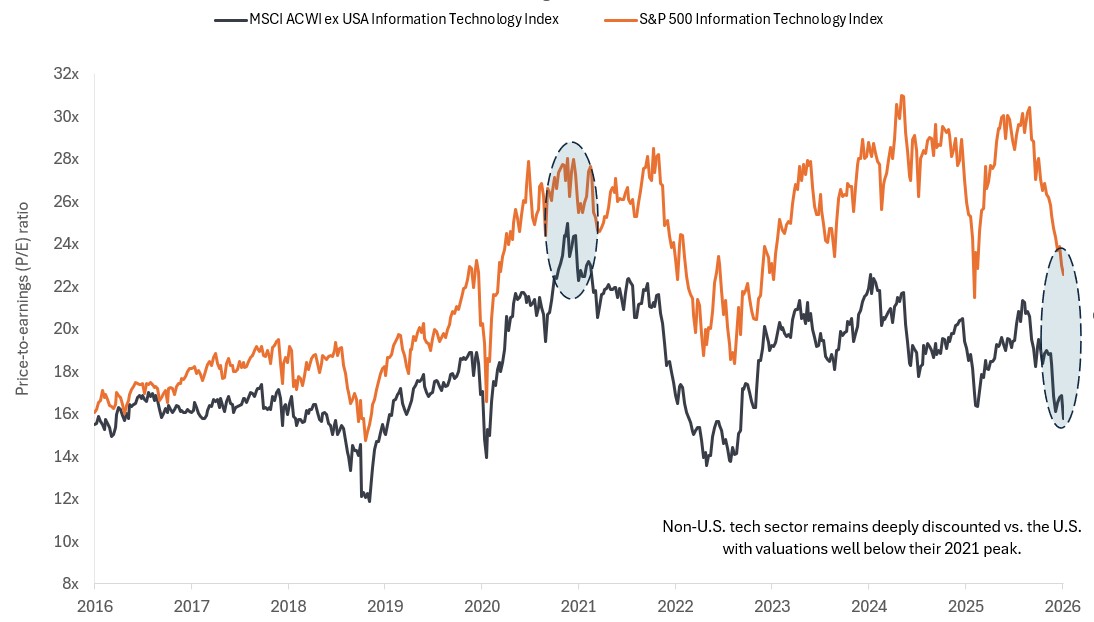

Meanwhile, valuations have become more attractive, and the discount to U.S. tech stocks remains historically wide. In recent months, the forward price-to-earnings (P/E) ratio for the MSCI ACWI ex USA IT Index has compressed, not expanded, as growth in the denominator (earnings per share) has more than outweighed the higher price. By this measure, non-U.S. technology appears cheaper today than before the rally began.

Exhibit 3: Non-U.S. technology continues to trade at a discount to the U.S.

Price-to-earnings (P/E) ratios for international technology stocks have compressed during the rally, with valuations still deeply discounted relative to U.S. peers.

Source: Bloomberg, data from 28 February 2016 to 3 March 2026. P/Es are based on forward 12-month estimated earnings. Past performance does not predict future results.

We highlighted this valuation disconnect in our 2026 outlook and continue to believe the gap between U.S. technology companies and many leading international firms presents a compelling opportunity for investors with a long-term view.

International markets offer fertile ground for discerning investors

As the AI growth story matures, investor scrutiny is intensifying, making selectivity all the more crucial. The turbulence that rippled through software and technology-adjacent sectors in February served as a reminder of how quickly sentiment can turn against companies viewed as being on the wrong end of AI proliferation.

International markets, in our view, offer a deep opportunity set of technology firms whose businesses are poised to benefit from accelerating AI investment rather than being disrupted by it.

Putting macro-driven volatility in context

While the fundamental backdrop remains supportive, an increasingly tense geopolitical environment has the potential to create bouts of volatility. Case in point, the coordinated U.S.-Israeli strikes on Iran – and concerns about a prolonged Middle East conflict – which triggered heavy selling across international markets in early March. The prospect of sharply higher crude prices and knock-on inflation effects weighed particularly hard on oil-importing countries. And with the shift toward “risk-off” sentiment, many Asian technology stocks experienced a sharp pullback as investors sold indiscriminately.

Such knee-jerk reactions to exogenous shocks are not unusual – particularly after stretches of strong outperformance. However, they do not alter our view of the underlying fundamentals for companies that play an integral role in the AI infrastructure buildout. We continue to focus on businesses with differentiated capabilities and durable competitive positions where growth prospects and valuations support room for further upside.

Near-term volatility can create opportunities for active management. In our view, a disciplined approach, grounded in deep fundamental research, will remain essential to identifying long-term winners as the global technology landscape evolves.

IMPORTANT INFORMATION

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

Price-to-Earnings (P/E) Ratio measures share price compared to earnings per share for a stock or stocks in a portfolio.

The MSCI ACWI ex USA Information Technology Index includes large- and mid-cap stocks across 22 of 23 Developed Markets (DM) countries (excluding the U.S.) and 24 Emerging Markets (EM) countries classified in the GICS® Information Technology sector.

The S&P 500® Information Technology Index comprises stocks included in the S&P 500 classified in the GICS® Information Technology sector.

Volatility measures risk using the dispersion of returns for a given investment.