Peeling back the onion: A concentric approach to investment decision making

Portfolio Managers Greg Wilensky and Jeremiah Buckley offer a framework for interpreting economic news for investment decision making.

7 minute read

Key takeaways:

- Investors are faced with an overwhelming amount of news and information daily that they often feel compelled to act on.

- Too often we see investors wanting to make big decisions about asset allocation, or whether to get in or get out of the markets, based on economic events.

- In our view, investors can benefit from a concentric approach to investment decision making that helps ensure they don’t allow attention-grabbing headlines to jeopardize their long-term investment success.

The past year has been punctuated by attention-grabbing headlines: The ongoing war in Ukraine, the U.K. pensions crisis, the collapse of Silicon Valley Bank, debt ceiling negotiations, the rise of ChatGPT … and the list goes on.

No society in human history has had access to as much information as we do today. While this access clearly has advantages, it also creates a new challenge: Processing and interpreting the sheer volume of information and using it to make better decisions has become a complex problem.

Investors in particular are faced with waves of new information every day regarding financial markets, the economy, and individual companies. So, the question becomes: What should one do with all this news?

The mistake

Too often we see investors overreacting to major (and minor) economic news by wanting to alter their asset allocation, or worse, wanting to stop or start investing altogether. In our view, one shouldn’t make major decisions about asset allocation, or whether to “get in” or “get out” of the markets, based on current events.

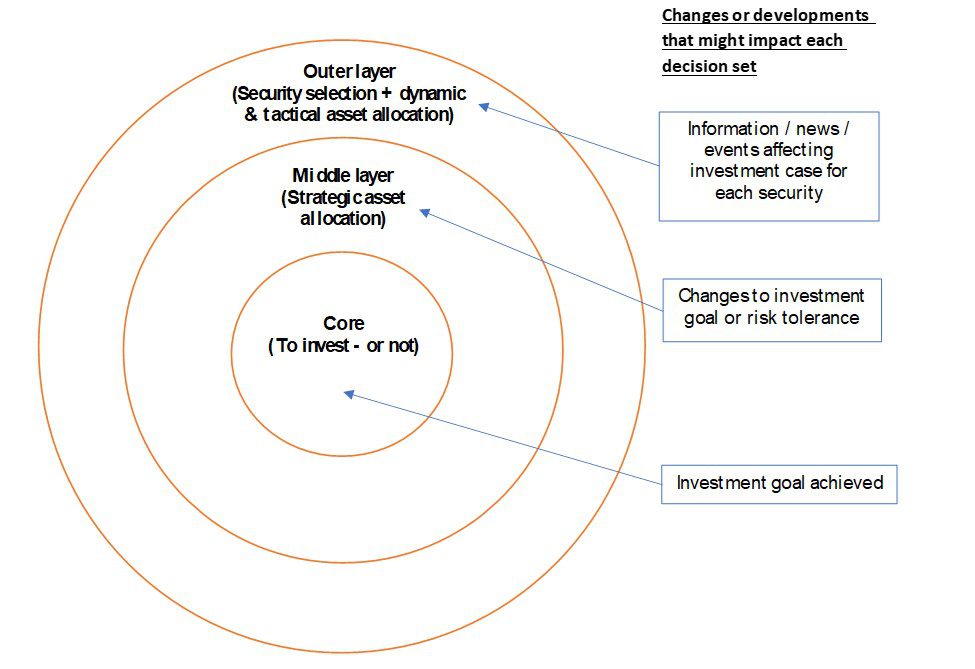

As such, we think investors can benefit from applying a defined framework to their investment decision making. In Exhibit 1, we propose a three-layer concentric approach to the investment decision-making process. Working outward from the center, each circle represents a decision set for the investor.

Exhibit 1: A concentric approach to investment decision making

The core: The decision to invest – or not

Before deciding what to invest in, one must first decide whether to invest – in simple terms, this is the decision to “get in” to the markets.

While this decision is often made tacitly, we think it’s important to consider it explicitly. Most importantly, we believe economic forecasts should not be a factor at this level.

Just as someone might pick a place to live based on its climate rather than its weather on any particular day, investors should base their decision to invest on long-term market assumptions while disregarding the day-to-day “weather” in financial markets. (The proverbial weather will play a role at a subsequent level of decision making, however.)

It follows that the decision to invest should not be modified or questioned due to events taking place in the economy – but all too often we see investors trying to time their entry and exit from markets based on economic projections.

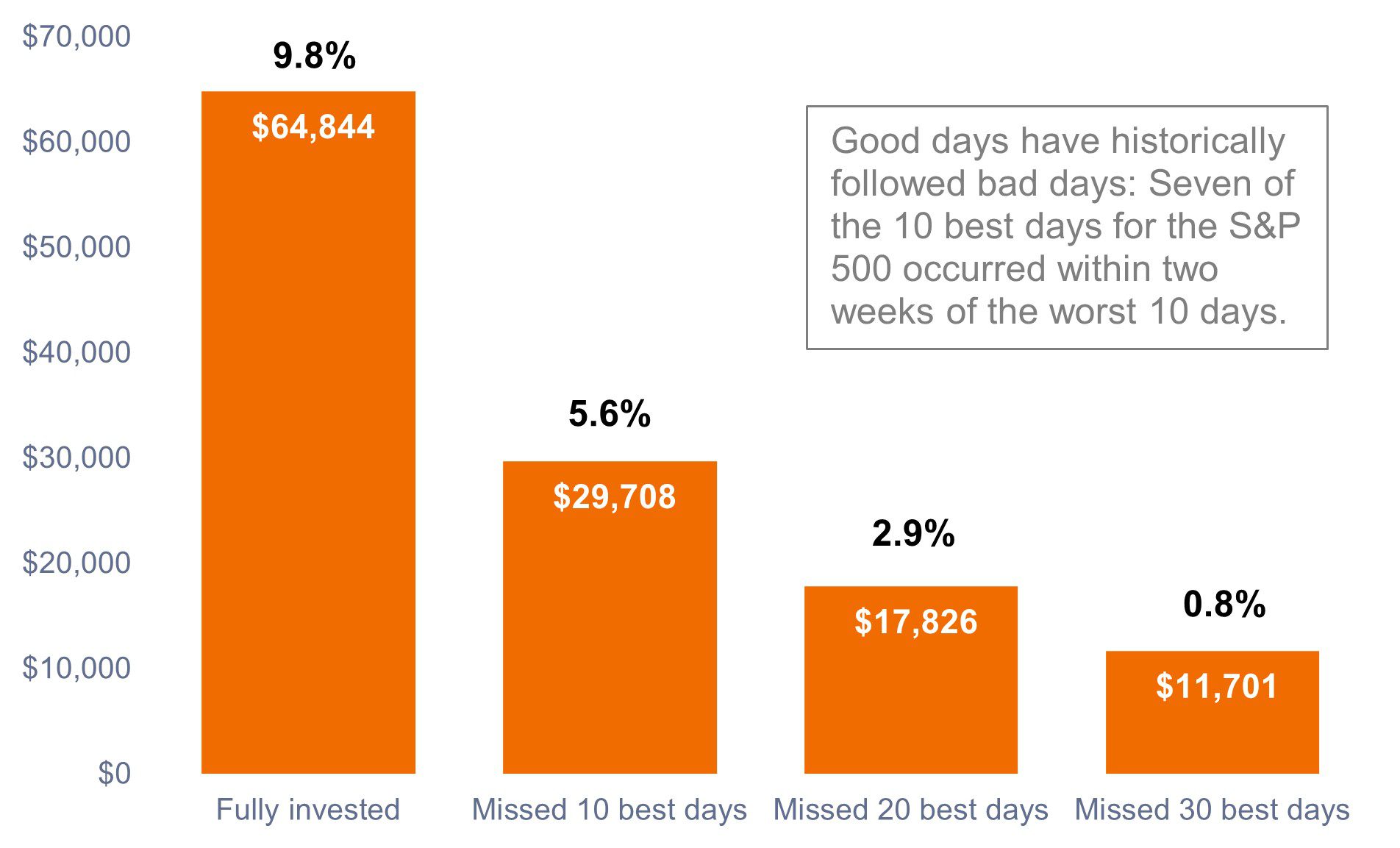

Numerous studies have shown that the average investor misses out on significant returns by trying to time the market. As shown in Exhibit 2, missing out on a handful of the best days over a 20-year period can drastically affect long-term investment returns. Investors should rather think about staying invested until they achieve their investment objective (e.g., child attends college and uses saved capital) to ensure they maximize what markets are offering.

Exhibit 2: The risk of market timing

Cumulative return on a hypothetical $10,000 investment in the S&P 500® Index (Jan 2003 – Dec 2022)

Source: J.P. Morgan, Bloomberg, as of 31 December 2022. Past performance is no guarantee of future results.

The middle layer: Strategic asset allocation

Once a decision is made to put capital to work, one can move to the next level of decision making, which is to decide on an appropriate long-term mix of asset classes – stocks, bonds, cash, real estate, private equity etc.

Determining a strategic asset allocation is a matter of personal goals, and risk tolerance. While this may sound simple in theory, in practice it requires careful planning and consideration. Financial professionals spend much of their time helping clients define their goals and risk tolerance to help ensure their investment allocation meets their objectives.

At this level, too, we often see investors wanting to adjust their asset allocation to be “risk-on” or “risk-off” based on market events or economic projections. We would advise against this form of de facto market timing and would encourage investors to invest in a portfolio they’re comfortable holding through an entire market cycle. When does it make sense to alter a strategic allocation? In our view, only when the investor has realized a change in their investment goal or risk tolerance.

The outer layer: Security selection, and dynamic and tactical asset allocation

The final level of decision making focuses on a) making marginal tactical and dynamic tilts to asset allocation, and b) selecting securities to fill each asset class bucket. In our view, it is at this level that the proverbial weather in financial markets comes into play.

Importantly though, instead of focusing on backward-looking economic data releases, we believe looking at leading and current indicators and anticipating where those economic data points will go in the future is the correct approach. And while there is still much information to process, we can filter it through a single lens, focusing on which companies we think will do better given current and expected future conditions.

Regarding security selection, investors can buy an index – thereby owning all securities in an asset class – or they can hire an active manager to select individual securities. As an active manager, we believe one is inherently buying individual businesses when investing, and we like to know what we own and why we own it.

The case for active management amid higher interest rates

We believe the active approach will be especially crucial as the global economy returns to a more normalized (read: higher) interest-rate regime. While index-based investing has grown substantially in the past decade, it is important to note that it did so under macroeconomic conditions that were utopian for it – namely 15 years of zero interest rates and major quantitative easing by central banks.

Interest rates are to companies what a high-jump bar is to track-and-field athletes – with the bar on the floor, it’s easy for all competitors to clear it irrespective of their athletic ability. But as the bar is raised, only those with the requisite athletic ability to jump can clear the bar. Similarly, a zero interest-rate policy favors all companies in an index being winners, whereas higher rates are likely to result in clearer separation between winners and losers.

We have seen this play out recently in the banking sector, where cracks have started to show in the weaker players as interest rates have risen. We think this trend will continue across industries, and investors will therefore be better served being selective about what they own versus owning every stock and bond in the universe.

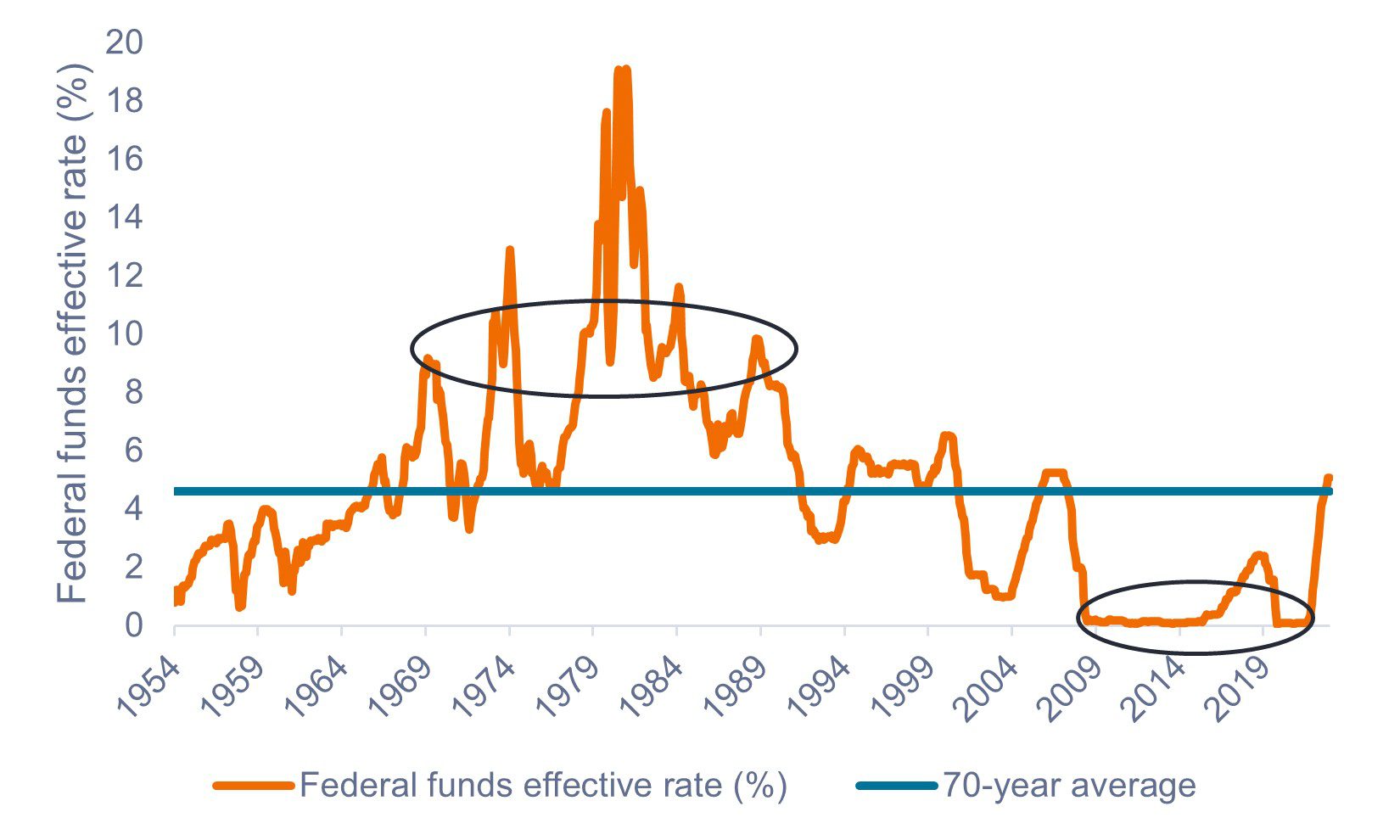

As shown in Exhibit 3, over the last 70 years, there have been a handful of periods where interest rates were either unusually high or low. The period of zero interest rates between 2008 and 2022 and the resulting economic incentives, were, historically speaking, more abnormal than normal. As such, we expect a return to a more normal interest-rate environment with clear separation between winners and losers.

Exhibit 3: Federal funds effective rate (1954- 2023)

Circled areas indicate extended periods of abnormally high or low interest rates, which we consider unsustainable in the long term.

Source: Board of Governors of the Federal Reserve System, as of 30 June 2023.

Source: Board of Governors of the Federal Reserve System, as of 30 June 2023.

Conclusion

With the amount of information that’s thrown at investors every day, figuring out what to do with it all can be an overwhelming task. We believe a concentric framework for investment decision making, coupled with an active approach emphasizing security selection and dynamic and tactical asset allocation, may lead to better long-term investment outcomes.

Furthermore, while current news flow should not impact one’s decision to invest or their strategic allocation, we believe investors should use forward-looking analysis that incorporates news flow to help inform bottom-up security selection and drive moderate dynamic asset allocation shifts with portfolios.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.

Specific risks

7 minute read

Key takeaways:

- Investors are faced with an overwhelming amount of news and information daily that they often feel compelled to act on.

- Too often we see investors wanting to make big decisions about asset allocation, or whether to get in or get out of the markets, based on economic events.

- In our view, investors can benefit from a concentric approach to investment decision making that helps ensure they don’t allow attention-grabbing headlines to jeopardize their long-term investment success.