Chart to Watch: How well have AAA CLOs handled interest rate volatility?

Portfolio Manager John Kerschner explains why AAA collateralized loan obligations (CLOs) may be well suited to navigating an uncertain rate environment.

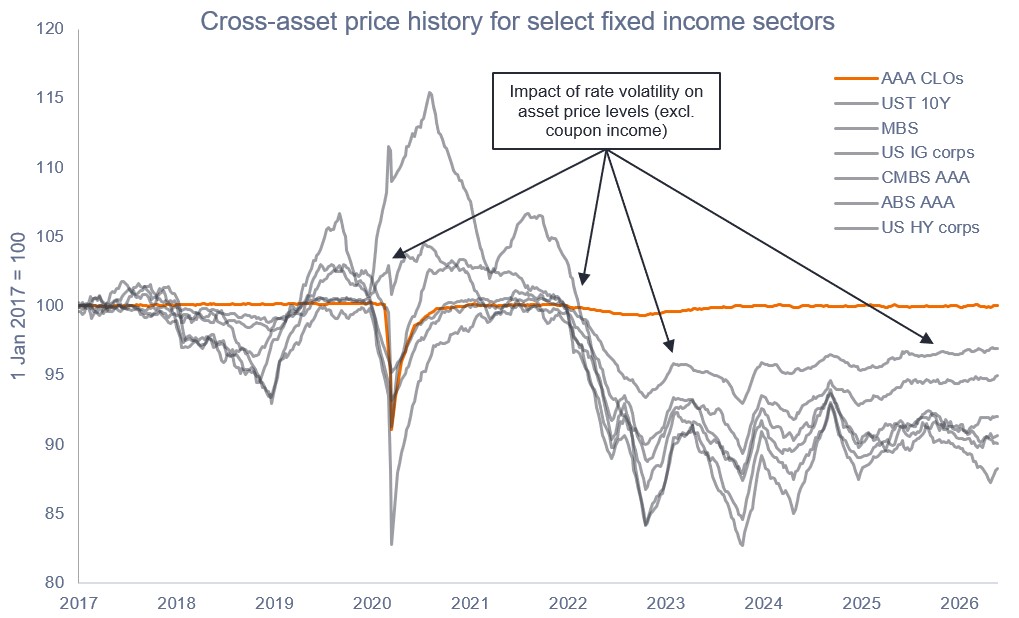

Source: Bloomberg, Bank of America, as of 31 May 2026. Illustrative price-return index levels (excl. coupon income). Indices used to represent asset classes: AAA CLOs represented by JP Morgan AAA CLO Index, 10-year U.S. Treasuries (UST 10Y), agency mortgage-backed securities (MBS), US investment grade (IG) corporates, AAA commercial mortgage-backed securities (CMBS), AAA asset-backed securities (ABS), and US high yield (HY corps) represented by relevant Bloomberg indices. Past performance does not predict future results.

Early this year, markets were predicting the Federal Reserve would deliver two rate cuts in 2026 and that rates would not rise back to current levels until 2030. Following consistently strong employment and growth data, as well as an unwelcome spike in inflation due to higher energy prices, the market now anticipates a hike later in 2026, with rates likely continuing to rise thereafter. This is just the latest chapter in the post-ZIRP economy. We think investors should adapt to the new reality and consider assets such as AAA CLOs, which possess a compelling mix of strong credit quality, floating rate income, and price stability that has performed well as the interest rate regime has shifted.

Key takeaways

- In the six years since mid-2018, fixed income investors have had to contend with a markedly less-certain interest rate environment compared to the 10 years that succeeded the Global Financial Crisis, when the federal funds rate was firmly rooted to zero and talk of shifts in monetary policy was scarce.

- This post zero-interest-rate-policy (ZIRP) environment has required investors to pay closer attention to managing their exposure to rate volatility if they are to realize the diversification and volatility-reducing benefits of their fixed income allocation. And this new rate regime is likely to persist, with a low probability that we revert to the benign ZIRP environment, in our view.

- We believe the key to successfully navigating the new regime hangs on staying up in credit quality and being cautious on taking interest rate risk. More specifically, diversifying exposure to include floating-rate CLOs, which benefit from rate hikes (in contrast to fixed-rate bonds, which fall in value when rates rise) is essential, in our view.

Amid significant shifts to rate expectations in 2026, most fixed income sectors have continued to exhibit price sensitivity and dispersion, yet AAA rated collateralized loan obligations (AAA CLOs) have remained tightly anchored near par.

We believe ongoing developments surrounding inflation, rates, and market volatility, coupled with geopolitical, fiscal, and monetary policy uncertainty, have highlighted how well-suited AAA CLOs are to navigating uncertain environments, as their low-duration, floating-rate structure may help provide stability and capital preservation amid persistent rate uncertainty. The chart shows cross-asset price history for select fixed income sectors and excludes the impact of coupon income.

Credit quality ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest).

A credit spread refers to the difference in yield between two bonds of similar maturity but different credit quality. It acts as a market indicator of credit risk—widening when risk rises and narrowing when it drops—and is typically measured in basis points.

Duration measures a bond’s price sensitivity to interest rate changes, expressed in years. A higher duration means greater price volatility when rates move.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Volatility measures risk using the dispersion of returns for a given investment.

A yield curve is a line that plots the yields, or interest rates, of bonds that have equal credit quality but different maturity dates.

IMPORTAANT INFORMATION

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.