Key takeaways:

- Bubble timing is less critical than portfolio resilience – investors should focus on mitigating drawdowns rather than predicting peaks.

- Equity income strategies offer participation in growth themes like AI while emphasising fundamentals such as cash flow and disciplined capital allocation.

- Diversification and dividend focus reduce concentration risk and provide stability during market corrections, as history has shown in past bubbles.

Debates about market bubbles surface regularly, but when speaking with long term-oriented investors the real concern isn’t pinpointing the top, it is what happens when the downturn comes. Investors worry less about timing and more about the depth, duration, and long‑term impact of drawdowns.

However, sitting out of markets can be as costly as staying fully invested, and history shows that both avoiding a theme and chasing it blindly can hurt returns. Although there isn’t a “silver bullet” way to both avoid bubbles and partake in them, there are strategies that can be utilised to help manage the risks.

Our view

We know we are in a boom period for technology, led by artificial intelligence (AI). But while valuations have risen sharply, the technology itself is not a bubble. Like the internet, it will reshape companies across regions and sectors. The challenge is where and how investors gain exposure.

The dot‑com era showed that investors were right about the transformative potential of the internet, but many early “winners” were not the winners of the future. Valuations ran ahead of fundamentals, and names such as Pets.com or World Com, although touted as the bastions of the internet, ended up as major losers.

Today, sector concentration is again a defining feature of the market. Innovation in AI, cloud and automation has pushed technology to dominate global indices, increasing concentration risk, and becoming a progressively larger part of investor portfolios. But when one sector drives most returns, even a modest correction can have an outsized impact on investors’ portfolios. We saw the impact of this extreme sector concentration on the release of DeepSeek in early 2025, with a shift in the prevailing market trend as investors reacted. If there is an collapse, a large amount of capital might need to find a new home.

One way to protect portfolios is by maintaining sufficient diversification so that no single sector carries an outsized share of the risk.

But importantly being diversified doesn’t mean you are abandoning innovation. Investors can participate in the theme through companies with proven profitability and disciplined capital allocation, rather than chasing speculative names where valuations can outrun fundamentals. Examples of this in the current market could be companies that help enable AI, such as utilities providing power via the grid, or companies and industries that might benefit from the cost savings that AI generates. This is where equity income strategies are particularly effective. They emphasise financial strength and cash‑flow reality, rather than speculative growth.

So, while investors remain optimistic about the long‑term potential of these innovations, many companies behind this growth also appear stretched on near‑term valuations. This leaves the market balancing long‑term confidence with short‑term vulnerability.

What the early 2000s can teach investors now

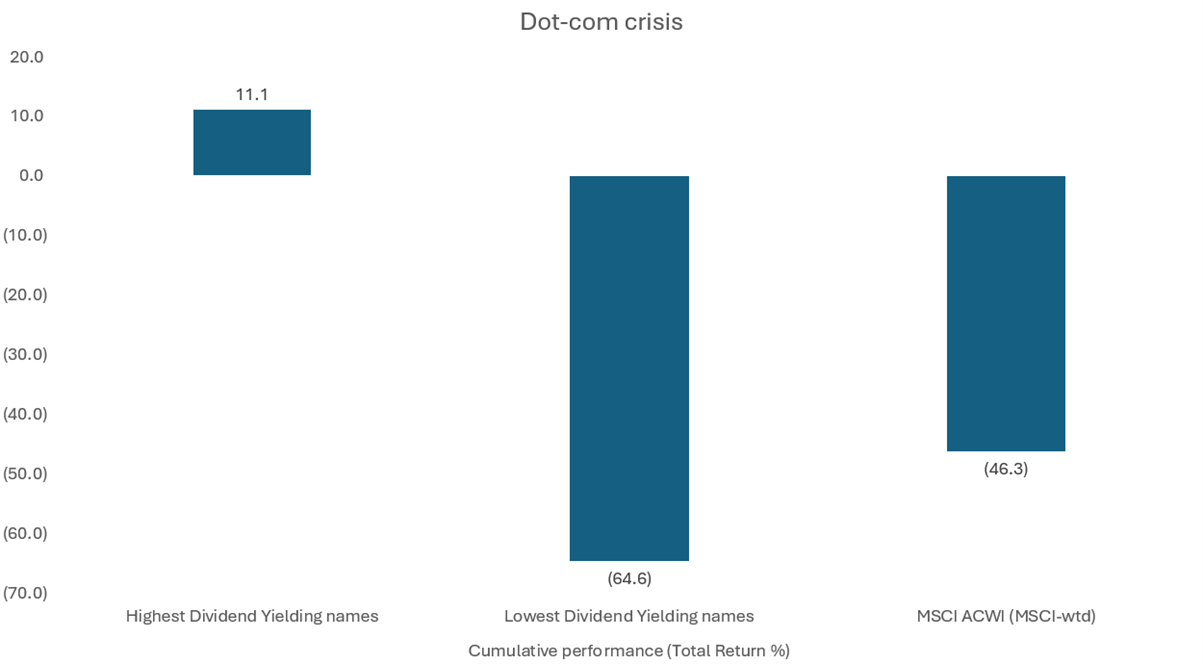

Putting this into an historical context; during the TMT bubble (2000–2002) dividend names proved to be resilient while large parts of the market were not. The MSCI World Index fell -46.3%, the lowest‑yielding stocks fell -64.6%, while the highest dividend‑paying companies, returned +11.1% (Figure 1).

Figure 1: Dividend yielding companies proved resilient to TMT bubble

Source: Jefferies, Factset Alpha Tester. Past performance does not guarantee future results

Note: Time periods in charts showing April 2000 – September 2002.

Why portfolio structure matters more than bubble-spotting

So, what does this mean? Well, it highlights that in periods where there has been a sector-dominated bubble and a subsequent fall, equity income strategies have tended to exhibit more resilient drawdown profiles. We have seen this in other periods too, such as in 2022, when they materially outperformed high‑duration growth assets.

This highlights that portfolio structure, not bubble‑spotting, can often determine resilience. To reiterate the point, equity income strategies do not seek to avoid bubbles entirely, but rather take part in the theme while focusing on companies with structural characteristics that inherently lower volatility such as:

- Steadier cash flows

- More defensive businesses

- Dividends that cushion returns during market stress.

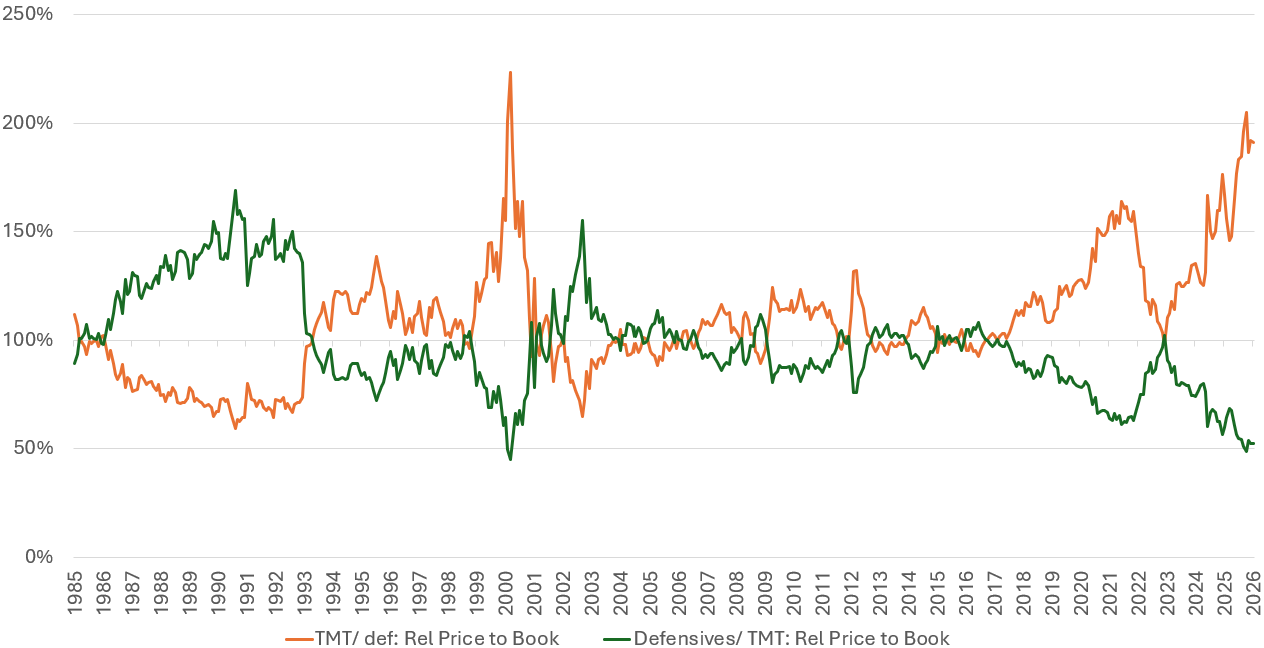

Another interesting chart highlights the relative valuation of U.S. tech versus defensive sectors (Figure 2). While the comparison is U.S. centric, this is reasonable given the U.S. is the epicentre of large‑language‑model and broader AI development, much as it was during the TMT bubble. The chart illustrates that defensive sectors tend to be depressed during periods of valuation expansion, yet they can prove far more resilient when those valuations unwind.

Figure 2: U.S. Relative valuation – tech and defensives

Source: Datastream, BNPP Estimates

Notes: Time periods in chart showing 29 January 1985 – 29 January 2026. Defensives = Consumer Staples, Healthcare, Utilities. Past performance does not guarantee future results.

Staying invested without staying exposed

Equity income strategies allow investors to participate in major themes like AI, while reducing exposure to their volatility by focusing on fundamentals such as cash flow and capital allocation. They offer a way to stay invested, capture long‑term growth, and preserve capital if sentiment turns.

This is especially important for clients withdrawing from their portfolios during a long drawdown, as this can permanently impair future returns. Investors want innovation, but they also want stability. Dividend‑focused global strategies can provide both through:

- Exposure to structural growth themes

- Diversification that tempers drawdowns

- Consistent income supporting total return.

So, the focus shifts: it is less about predicting the next move and more about building resilience and diversification to withstand whatever comes next.

Building portfolios that withstand the next shock

The fear of bubbles is ultimately the fear of deep, prolonged drawdowns that permanently damage capital. With market leadership concentrated in fast‑growing innovation sectors, this risk is particularly relevant today.

Investors are not trying to time the peak; they are trying to ensure the next downturn does not dictate their long‑term outcomes.

A global, dividend‑oriented strategy provides a pragmatic balance: it participates in long‑term growth while emphasising cash‑flow strength, diversification, and valuation discipline. At the same time, it invests in defensive beneficiaries, helping investors to compound returns more steadily over time, with fewer surprises and greater resilience.

Benchmark: A standard (usually an index) that an investment portfolio’s performance can be measured against. For example, the performance of a UK equity fund may be benchmarked against the FTSE 100 Index, which represents the 100 largest companies listed on the London Stock Exchange.

Diversification: A way of spreading risk by mixing different types of assets or asset classes in a portfolio on the assumption that these assets will behave differently in any given scenario. Assets with low correlation should provide the most diversification.

Dividend: A variable discretionary payment made by a company to its shareholders.

Drawdown: A measure of historic risk that looks at the difference between the highest and lowest price of a portfolio or security during a specific period. It is used to evaluate the possible risk and reward of an investment.

Equity: A security representing ownership, typically listed on a stock exchange. ‘Equities’ as an asset class means investments in shares, as opposed to, for instance, bond. To have ‘equity’ in a company means to hold shares in that company and therefore have part ownership.

Equity income strategies are investment approaches focused on generating regular income, primarily through dividends from high-quality, cash-generative companies, while aiming for long-term capital appreciation. These strategies often target stocks with consistent, above-average dividend yields, providing a more conservative alternative to growth-focused investing.

Large Language Models (LLMs): A software tool capable of corpus-based linguistic analysis and prediction, particularly an artificial intelligence system that processes written instructions (prompts) and is capable of generating natural language text.

Low duration/high duration stocks and stocks: Typically, high-value, high-profitability, low-investment, and low-risk stocks.

The TMT bubble (Technology, Media, and Telecommunications bubble), commonly known as the dot-com bubble, refers to a period of intense speculative investment in the late 1990s, particularly between 1995 and 2000. It was characterized by rapidly rising, unsustainable valuations of internet-based companies, largely driven by the adoption of the World Wide Web and the belief that traditional valuation metrics no longer applied to the “new economy”.

Valuation metrics: Metrics used to gauge a company’s performance, financial health, and expectations for future earnings, e.g. P/E ratio and ROE.

Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility, the higher the risk of the investment.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.