Key takeaways:

- After years of subdued performance and limited investor enthusiasm following the Global Financial Crisis (GFC), European banks have staged a strong recovery, supported by stronger capital positions, healthier loan books, and improved operating efficiency.

- A more constructive operating environment has lifted profitability to post‑GFC highs, with return on equity (ROE) levels for European banks closing the gap with U.S. peers.

- Despite these improvements, valuations remain modest relative to both history and global peers, suggesting investors may be underestimating the durability of the sector’s stronger fundamental backdrop.

After more than a decade contending with the aftereffects of the Global Financial Crisis (GFC), European bank stocks have reemerged as one of the notable bright spots across the region’s equity markets in recent years. In 2024 and 2025, the STOXX® Europe 600 Banks Index returned an impressive 35% and 77%, respectively, outperforming the broader STOXX® Europe 600 Index by more than 105 percentage points over that span.1

Importantly, this followed a long stretch of relative underperformance as tougher banking regulations and ultra-low interest rates weighed on profitability and loan growth. But while a low starting point and recognition of deeply depressed valuations – and subsequent multiple expansion – may explain some of the rally, improved fundamentals have been an underappreciated aspect of the story, in our view.

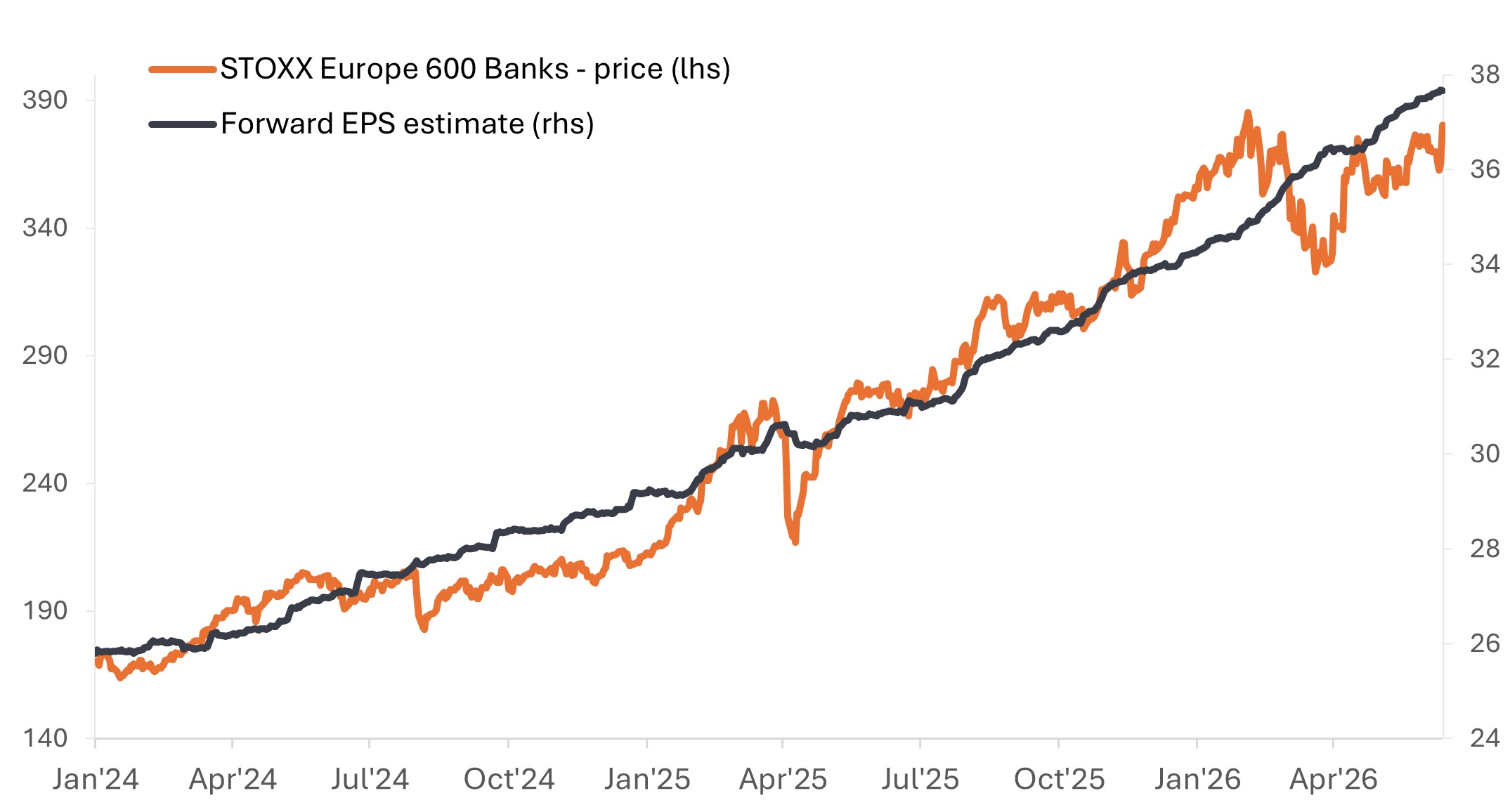

Indeed, the rally over the last two years has been underpinned by earnings growth, as shown in the chart below. And while the Iran conflict injected a fresh dose of macro-driven volatility, valuations across the sector remain modest, and we believe the case for further rerating is firmly intact.

Exhibit 1: Strong 2024 and 2025 performance driven by significant upward earnings revisions and multiple expansion

Next 12-month forward earnings estimates have increased markedly over the past 2.5 years.

Source: Bloomberg, data from 1 January 2024 to 12 June 2026. Past performance does not predict future results.

Emerging from a 15-year post-GFC deleveraging cycle

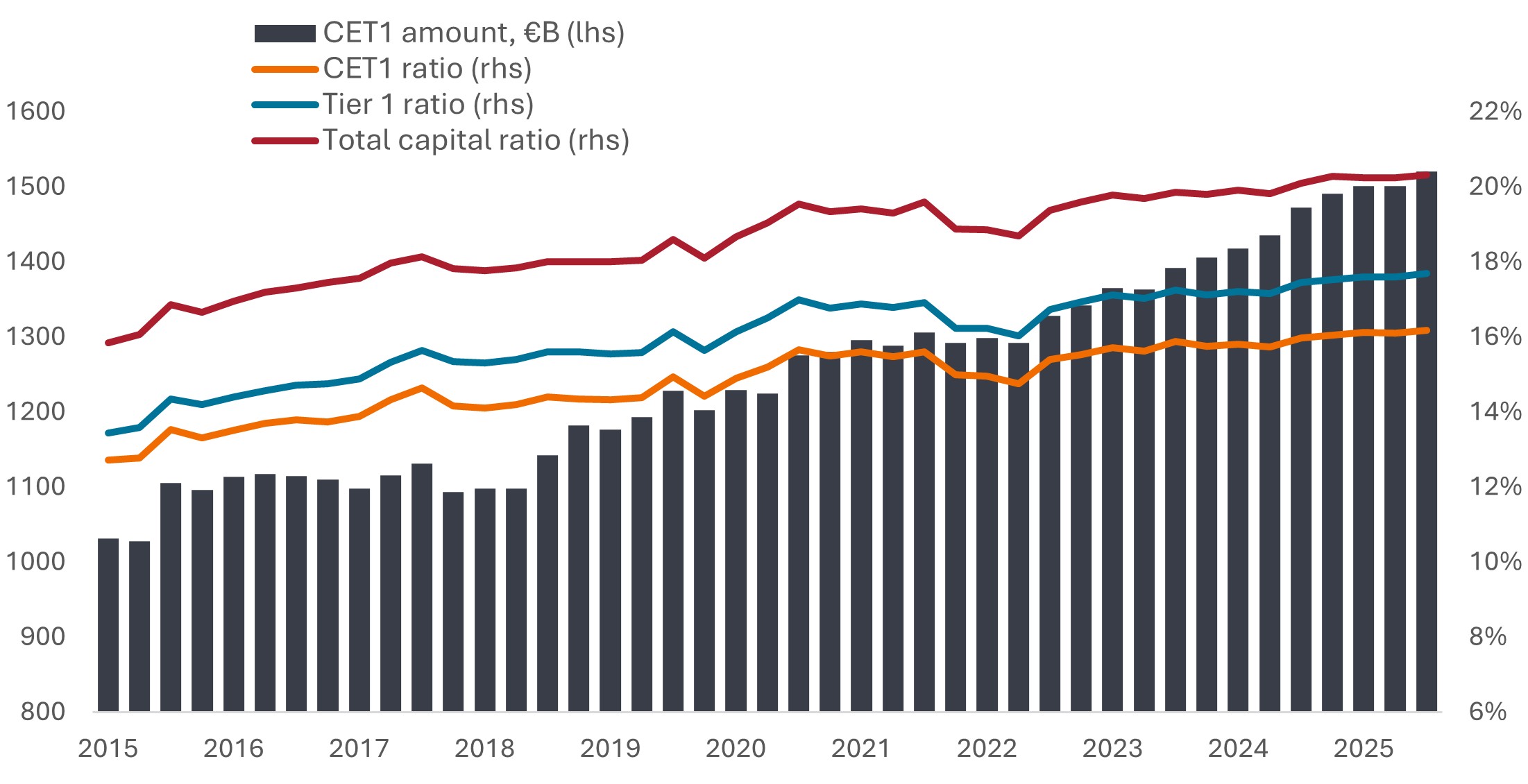

In Europe, banks have spent more than a decade improving the size and quality of their capital reserves, as evidenced by a steady rise in Common Equity Tier 1 (CET1) levels and capital ratios (Exhibit 2). While this has supported banks’ ability to weather exogenous shocks, it has also constrained lending, resulting in a period of muted – and at times, negative – loan growth. This, in turn, weighed on economic growth across the region, as banks provide the majority of financing to the corporate sector.

More recently, there has been growing debate about whether the pendulum may have swung too far toward over-regulation. To date, progress toward deregulation has been limited, but discussions are underway around proposals to free up capital, support lending, and improve the competitiveness of European banks.

Exhibit 2: European banks have built materially stronger capital positions

CET1 amount and capital ratios

Source: ECB, “Supervisory Banking Statistics for significant institutions, fourth quarter 2025”, 18 March 2026.

At the same time, risk controls and cost-cutting measures honed during the days of negative rates have vastly improved many firms’ operating efficiency. Loan books have also been significantly de-risked, with the non-performing loans ratio for significant institutions falling to roughly 2% in recent European Central Bank (ECB) data, down from more than 7% a decade ago.2

The upshot is that European banks have emerged from the prolonged deleveraging cycle as a healthier, more profitable sector, with higher interest rates providing an additional tailwind to earnings.

A more constructive operating environment

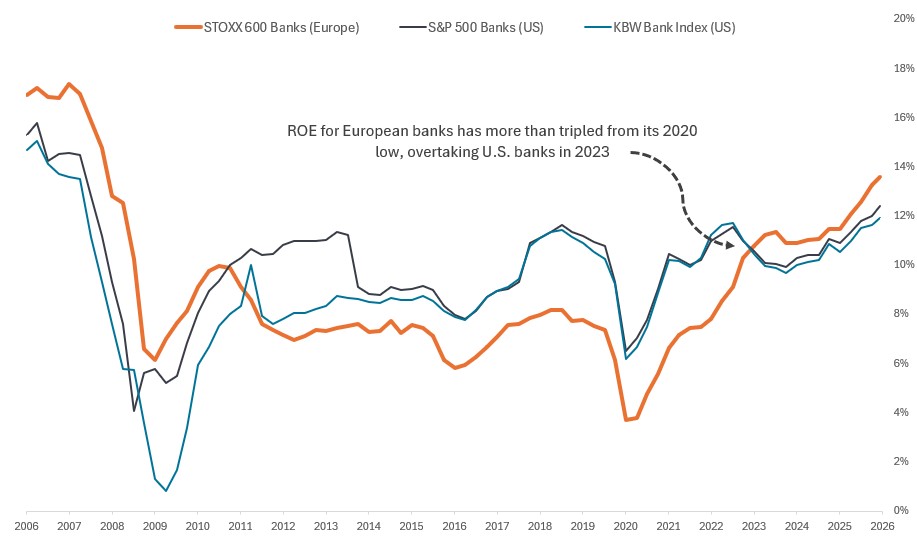

Consequently, the region’s banks have been achieving their highest profitability of the post-GFC era, as measured by return-on-equity (ROE) levels. After bottoming in the mid-single-digits range in the aftermath of the pandemic, European banks have closed the gap with their U.S. peers and, in some cases, moved ahead for the first time in years.

Exhibit 3: European banks have closed the profitability gap with U.S. peers

Return on equity (ROE), rolling 12-month forward estimate

Source: Bloomberg, data as of 12 June 2006 to 12 June 2026. Past performance does not predict future results.

Valuations suggest room for further rerating

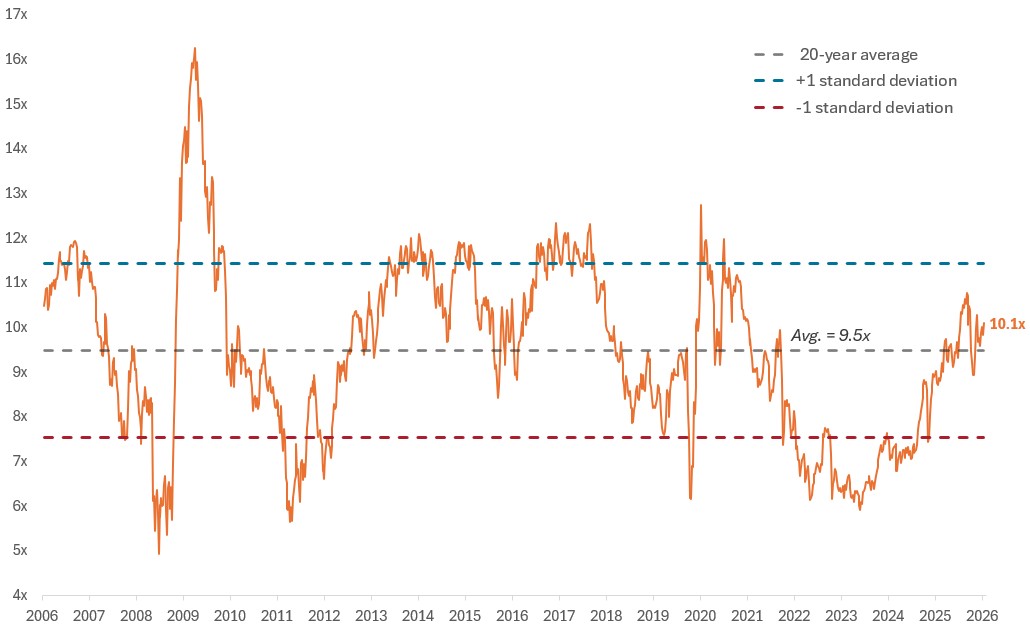

Despite this improved fundamental picture, European bank stocks continue to trade at a meaningful discount to U.S. banks and the broader European equity market. Although valuations have risen from deeply depressed levels, they have only recently returned to their long-term average.

- As of this writing, the STOXX Europe 600 Banks Index has a forward price-to-earnings (P/E) ratio of 10.1, only slightly above its long-term average of 9.5 and still well below peaks seen during the 2010s, when the sector was more fundamentally challenged.

- By comparison, the KBW Bank Index, representative of U.S. bank stocks, trades at 12.8 times forward earnings, while the P/E for the broader STOXX Europe 600 Index sits at 15.0.3

Exhibit 4: European bank valuations are yet to fully reflect improved fundamentals

Price-to-earnings (P/E) ratio, 12-month forward estimate

Source: Bloomberg, data as of 12 June 2006 to 12 June 2026. Past performance does not predict future results.

Meanwhile, European banks have been returning capital to shareholders at a healthy clip in the form of dividends and share buybacks, with the dividend yield on the STOXX Europe 600 Banks Index north of 5%, more than double that of comparable U.S. benchmarks.4

All of this would argue in favor of room for further multiple expansion, in our view. While some discounting to U.S. peers may be warranted, we believe the persistently wide valuation gap also reflects anchoring bias – a tendency among investors to reference past underperformance when making investment decisions.

Longer-term structural shifts and potential implications

Beyond the improved earnings trajectory and still-attractive valuations, a combination of structural shifts and secular drivers is reshaping the investment landscape for European banks and could further support the case for additional upside.

- Pro-domestic growth initiatives: As global realignment pushes Europe to focus more intently on domestic growth, competitiveness, and supply-chain resilience, banks are likely to play a key role in providing capital to the real economy – a potential tailwind for loan growth.

- AI-driven efficiency gains: While Europe’s participation in the AI secular theme is often overlooked, banks stand out as an industry particularly well positioned to benefit from automation and productivity improvements, with potential for structurally lower costs that are not yet fully reflected in expectations.

- Bank mergers / consolidation: Consolidation across the sector has historically been concentrated within national markets, but there are early indications that focus is beginning to shift toward cross‑border opportunities. If regulatory barriers ease over time, this could help reduce fragmentation and support greater scale, efficiency, and competitiveness with global peers.

Navigating an uncertain macro environment

While recent geopolitical turmoil has strengthened the case for European nations to boost defense spending – a potential tailwind that could support lending growth – the Iran conflict and resultant energy shock have cast a pall over the economic outlook for the region. The dual threat of higher inflation and potential demand destruction poses a risk for net energy-importing countries and bears close monitoring.

The ECB responded on June 11 with its first rate increase since 2023, and markets are pricing in expectations for at least one additional rate hike this year, as of this writing. For now, the combination of modestly higher rates and still-resilient, albeit less-robust, economic growth aligns with the sort of environment in which banks typically thrive. That said, even with the recent Iran ceasefire extension, questions remain about how fully the Strait of Hormuz will reopen and the extent to which any lingering supply disruption could weigh on Europe and the broader global economy.

This uncertain backdrop makes selectivity all the more critical. While we believe the case for further valuation rerating remains compelling, it is unlikely to be uniform across the European banking sector. In our view, deep fundamental research and bottom-up stock selection are essential to identifying institutions with strong capital positions, diversified earnings streams, and exposure to attractive markets supported by longer-term secular tailwinds.

1Source: Bloomberg. Data represents total returns in local currency terms.

2 Source: ECB, “Supervisory Banking Statistics for significant institutions, fourth quarter 2025”, 18 March 2026.

3 Source: Bloomberg. Data as of 12 June 2026.

4 Source: Bloomberg, data as of 11 June 2026. U.S. benchmarks include the KBW Bank Index and the S&P 500 Banks Industry Index.

Common Equity Tier 1 (CET1) consists of the highest quality capital a bank holds, primarily made up of ordinary shares and retained earnings, serving as a cushion to support financial stability.

KBW Bank Index tracks the performance of leading banks and thrifts that are publicly traded in the U.S. The Index includes banking stocks representing large U.S. national money centers, regional banks and thrift institutions.

Price-to-Earnings (P/E) Ratio measures share price compared to earnings per share for a stock or stocks in a portfolio.

Return on Equity (ROE) is the measure of a company’s annual return (net income) divided by the value of its total shareholders’ equity, expressed as a percentage. The number represents the total return on equity capital i.e., the profits made for each dollar from shareholders’ equity.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

S&P 500® Banks Industry Index comprises companies included in the S&P 500 that are classified in the Global Industry Classification Standard (GICS®) Banks Industry Group.

STOXX® Europe 600 Index represents large, mid and small capitalization companies across 17 countries in the European region.

STOXX® Europe 600 Banks Index comprises stocks in the STOXX Europe 600 Index that are classified in the Industry Classification Benchmark (ICB) Banks Supersector.

Volatility measures risk using the dispersion of returns for a given investment.

IMPORTANT INFORMATION

Actively managed investment portfolios are subject to the risk that the investment strategies and research process employed may fail to produce the intended results. Accordingly, a portfolio may underperform its benchmark index or other investment products with similar investment objectives.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Emerging markets expose the Fund to higher volatility and greater risk of loss than developed markets; they are susceptible to adverse political and economic events, and may be less well regulated with less robust custody and settlement procedures.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Emerging markets expose the Fund to higher volatility and greater risk of loss than developed markets; they are susceptible to adverse political and economic events, and may be less well regulated with less robust custody and settlement procedures.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.