Key takeaways:

- Macro-driven volatility, higher rates and unstable correlations are reshaping asset pricing, shifting how risk and diversification behave. As a result, strategies less reliant on broad market direction can be useful.

- Diversified alternatives provide wide-ranging opportunities across multiple asset classes and strategies designed to capture various drivers of non-correlated performance throughout the market cycle.

- As markets grow more complex and unpredictable, diversified alternatives can complement equities and bonds by reducing reliance on market direction and potentially reducing drawdowns when diversification is most needed.

For much of the past decade, investing took place against a relatively supportive backdrop. With markets rising, investors were often encouraged to add beta, concentrate exposures or take on higher levels of risk in pursuit of incremental returns. In many cases, that approach delivered positive outcomes. But when markets have turned, portfolios with higher beta and limited diversification have frequently experienced sharper drawdowns than anticipated.

This dynamic helps explain why low beta and low correlation strategies can appear unnecessary during extended periods of market strength, yet become valuable quickly when conditions deteriorate. Diversification rarely feels urgent when asset prices are rising broadly. The challenge emerges when markets stall or reverse, correlations increase, and vulnerabilities that were tolerated during benign periods are exposed.

Only when the tide goes out do you discover who’s been swimming naked.

Warren Buffett

Markets at an inflection point

This shift feels increasingly relevant in the current environment. The global investment landscape has become more complex and less predictable. Geopolitical tensions remain elevated, energy security is more central to policy agendas, and industrial strategy, particularly around defence, technology and domestic supply chains, continues to reshape capital allocation. Inflation dynamics remain uncertain and pressured, interest rates are structurally higher than in the prior cycle, and macroeconomic variables exert greater influence on asset pricing than in the post crisis years.

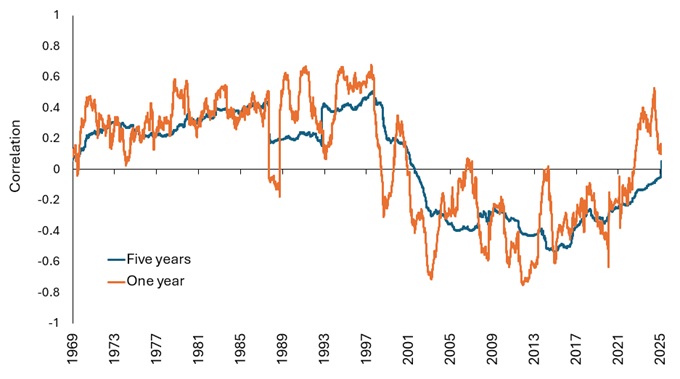

In such conditions, markets tend to be less forgiving of crowded positioning and narrow diversification. Correlations that previously appeared stable can shift rapidly, while macro shocks can overwhelm asset-specific fundamentals. Over the past few years, we have seen a steady erosion of the longstanding negative correlation between equities and fixed income, a foundational rationale for many balanced strategies to hold a strong ‘core’ of these two asset classes. In fact, five-year correlations are now positive for the first time since near the start of the century (Exhibit 1):

Exhibit 1: Correlation between the S&P 500 (equities) and US 10-year treasury rates (fixed income)

Source: Bloomberg, Janus Henderson, 6 February 1969 to 31 March 2026. Past performance is not a guide to future returns.

This does not necessarily signal a dramatic turning point, but rather a regime shift in how risk is rewarded and diversification behaves. In this environment, strategies designed to deliver returns with less reliance on broad market direction can become more relevant. Not as substitutes for traditional assets, but as complements within diversified portfolios.

Fragmented environments suit diversified alternatives

Periods of heightened uncertainty can widen the opportunity set for investors within a diversified alternatives framework. Volatility, dispersion and episodic dislocation can create conditions in which relative value, market neutral and event-driven approaches can find opportunities. A defining feature of these approaches is breadth – allocating across asset classes and investment horizons. Each component contributes differently to portfolio behaviour and carries distinct risks. The objective is not to eliminate risk, but to reduce reliance on any single return driver.

- Equity markets provide an illustration: In recent years, dispersion and correlation have swung between extremes, with periods of concentration followed by macro-driven phases in which stocks moved uniformly. Neither environment is inherently favourable or unfavourable. What matters is flexibility. Opportunities may arise from dispersion across securities or from rising correlations. Market neutral strategies seek to capture these dynamics rather than express directional views.

- Credit markets display a similar duality: Greater focus on liquidity, refinancing risk and credit quality has increased selectivity. In this context, strategies emphasising relative value or optionality, rather than outright credit exposure, can offer a controlled approach to credit exposure. Convertible bonds may present opportunities during higher volatility, provided credit risk is managed appropriately.

- Event-driven strategies may suit uncertain environments: This applies where company-specific developments can be overlooked or mispriced. Elevated volatility can widen spreads around mergers and restructurings, enhancing the risk-adjusted opportunity set.

- Commodities and resources add another dimension: Geopolitical priorities and supply chain shifts can create trends, but commodities are cyclical. Gains in favourable phases can reverse. Selective directional exposure combined with systematic risk management may help moderate volatility while retaining upside.

- Structural demand for capital persists: Investment cycles linked to digital infrastructure, energy transition and industrial capacity continue to generate security issuance, expanding opportunities for investors focused on inefficiency rather than market direction.

What is the role of diversified alternatives within portfolio construction?

Rather than competing with equities or bonds, diversified alternatives strategies address portfolio characteristics that traditional assets do not consistently provide:

- Differentiated sources of return: Equities are driven by earnings, valuation and sentiment, while bonds provide income and, at times, diversification, though effectiveness depends on inflation and interest rate dynamics. Diversified alternatives draw on a broader set of return drivers, such as relative pricing, market structure, optionality or event outcomes, which may behave differently across regimes.

- A considered approach to managing correlation risk: Correlations are not static, and diversification benefits often weaken during periods of stress. Combining multiple low-directionality strategies reduces dependency on historical relationships that may or may not persist.

- Make portfolio risk mitigation an explicit design choice: In prior cycles, bonds often offered diversification during equity drawdowns. In the current environment, that role is less reliable. Strategies such as trend following or systematic volatility exposure are increasingly used for this purpose, responding to sustained changes in market behaviour.

- Mitigate behavioural risk: During periods of market stress, portfolio managers can face pressure to reduce exposure. Strategies that contribute positively or provide mitigation that can reduce pressure elsewhere in the portfolio, supporting disciplined long-term decision making.

The objective is not to eliminate risk, but to reduce reliance on any single return driver.

David Elms, Head of Diversified Alternatives

The next phase for strategic investing

The case for diversified alternatives is not based on the view that traditional assets are obsolete. Equities and bonds remain core portfolio components. Rather, it reflects recognition that the environment in which they operate has become more complex and less predictable.

In this context, strategies designed to be flexible, diversified and less reliant on market direction can play a constructive role. While they may appear less compelling during prolonged calm, such approaches often justify inclusion during stress by moderating drawdowns and supporting portfolio resilience.

As investors place greater emphasis on correlation risk and robustness, diversified alternatives align closely with these objectives. The underlying principle remains consistent: diversification matters most when it feels least intuitive.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.