Key takeaways:

- 2025 thus far has been characterised by a clear shift in focus from the US to Europe for investors, influenced by President Trump’s protectionist policies, following a long period of US outperformance, and improving economic indicators in Europe.

- Positive regional reforms, such as Germany’s fiscal policy changes, and expectations of lower interest rates compared to the US, have prompted investors to look at reallocating to European small caps.

- More broadly, despite sustained global uncertainties and concerns about growth, small caps are less impacted by international tariffs due to their domestic focus and ability to adjust prices.

How quickly things can change…

Amid a wave of US exceptionalism at the start of 2025, investors were being cajoled to give up on Europe on the view it would be tariffed into extinction under new US President Trump’s ‘America First’ strategy. Few voices were brave enough to argue that this might be the year that European stocks finally outperform their US counterparts.

That all changed in April, when markets saw sharp corrections after Trump’s Liberation Day efforts to reshape global trade sent a shockwave around the world. While valuations have since rallied on backtracking, negotiations and tariff pauses, it prompted many investors to look hard at their portfolio and question if they have become too reliant on the US to generate returns. Flows have matched that uncertainty, with many investors choosing to diversify into other regions and asset classes. Europe has been a particular beneficiary of this diminished trust in the US.

Expectations are high for further volatility as the US continues to push for global realignment, adding uncertainty over the direction of monetary policy from central banks, and with downside risks to economic growth forefront in investors’ minds. In this environment, we expect increasingly frequent regional (and sectoral) swings like this to be an increasingly frequent occurrence. But are there any clear trends that we can identify?

Trump 2.0

US President Trump’s second term was expected to be lively, and it has certainly proved to be the case thus far. Markets entered 2025 with the consensus view that the Trump administration would front-load the trade/tariff discussion, but to do it in conjunction with a more business-friendly agenda.

Instead, the focus has been exclusively on tariffs, trade negotiations, immigration and a startling realignment of US foreign policy, albeit one that seems determined to secure peace in Ukraine. On the former, uncertainty over the GDP impact of tariffs (and consequent retaliatory tariffs) represent a metaphorical sword of Damocles. The noise around tariffs could dissipate during these initial 90-day pauses as negotiations continue, but as we saw between the US, it could easily escalate once more. The outcome or impact is unsurprisingly difficult to forecast. More recently, we have seen House Republicans in the US pushing ahead with sweeping tax cut plans – the “Big Beautiful Bill” – via Budget Reconciliation, with potentially significant ramifications across industries, sparking debate over the potential impact of higher debt.

European renaissance?

The uncertainty that has taken hold in markets provides some context to investors’ decision to address their portfolio positioning. While tariff shocks provided the push that investors needed to pay closer attention to the attractive valuation case for European equities, there are other catalysts on the horizon that could see the current discount (relative to the US) narrow in a more sustained way:

German fiscal reform

There are still constitutional hurdles in the way for new Chancellor Merz, but Germany has upended decades of fiscal convention in its decision to release its debt brake, unleashing a large package of spending on defence and infrastructure. We would expect this to benefit more economically-sensitive domestic names, including small caps.

Potential peace (of sorts) in Ukraine

A start to rebuilding Ukraine and greater stability in the political climate would support lower energy prices and provide a strong platform for construction and materials names listed in western Europe. Defence stocks and banks with eastern European exposure are also likely beneficiaries from the accompanying rearmament and credit cycle.

Interest rates likely to come down more in Europe than the US

The European Central Bank cut its main interest rate (from 2.5% to 2.25%) in April – it’s third cut thus far in 2025 – in part aimed at offsetting the potential hit to exports from tariffs. The Bank of England followed in early May, with a 0.25% cut to 4.25%. This contrasts with decisions from the US Federal Reserve, which has pushed back against calls for rate cuts, given near-term inflation concerns.

What does this mean for small caps?

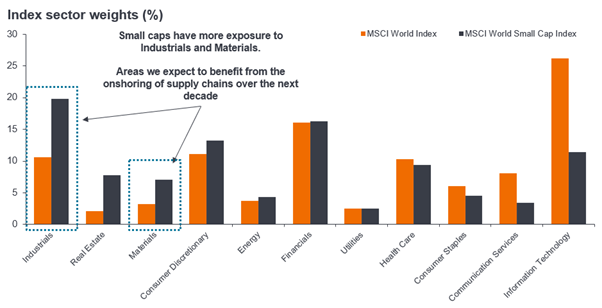

Rather than trying to guess the outcome of various tariffs, retaliatory tariffs, or their potential impacts, we believe it is more important to take a more practical view of what it could mean for businesses. Geopolitical uncertainty and the risk of tariffs has seen businesses actively seeking to shorten supply chains by moving production and processes closer to home. This could favour small caps, which have much more domestic exposure than their larger peers, particularly in Japan and the US, where domestic revenues are 75% and 78% respectively1. Small caps also have more exposure to sectors like industrials and materials, areas we expect to benefit from the onshoring and near-shoring trend (Exhibit 1).

Exhibit 1: Global small caps provide investors with exposure to different market dynamics

Source: Bloomberg, Janus Henderson Investors analysis, as at 31 December 2024.

We expect management teams in the US to try and pass on higher pricing to cover the cost of tariffs, negatively impacting purchasing power, but tariffs could also help domestic firms, filling the gaps created by overseas competitors becoming less cost competitive.

Interest rates are also a relevant factor for small caps, given their higher sensitivity to borrowing costs relative to their larger peers. Our view is that interest rates remain on a downward trajectory, but we will not be returning to ZIRP (zero interest rate policy), given the risks of tariff-inflicted inflationary pressures. This would not be a bad environment for small caps, given their significant valuation discount versus large caps. Particularly given the number of small cap stocks at present that are in a net positive cash position (46%, as at 30 March 2025, compared to 30% for large cap stocks)2.

In the event tariff-led inflation resurfaces, forcing central banks to reverse their course, higher rates have not always led to small cap underperformance in the past. It is worth keeping in mind that the last time we had higher rates was in the early 2000s, a period of strength for global small caps. If we look back to the 1970s, a period of consistently higher rates, US small caps outperformed large peers meaningfully.

We think current uncertainty offers the opportunity to increase exposure to global small caps at attractive levels. Smaller companies remain priced at a significant discount relative to their larger peers (Exhibit 2), a level that will take time to redress. As always, our focus is towards those stocks identified as attractively priced given their structure and return on cash.

Exhibit 2: Global small caps remain discounted versus their larger peers

Source: Bloomberg, Janus Henderson Investors analysis, as at 15 May 2025. Chart shows the relative valuations between global small cap stocks and global large cap stocks over time, using the forward price-to-earnings (P/E) ratio.

Note: Indices used: MSCI World Small Cap, MSCI World. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

We are in a period where investors are under pressure to assess how specific policies can affect demand and supply, inflation, monetary policy, individual sectors and companies. This is where active management and stock selection can add value, distinguishing between good quality business well positioned to benefit from the changing environment, and lower-quality businesses that have gained with the tide.

Debt brake: Germany’s balanced budget fiscal rule; strict limits that prohibit the federal government and states from taking out extra loans (focusing on balancing their books).

Discount: Refers to a situation when a security is trading for lower than its fundamental or intrinsic value. The opposite of trading at a premium.

Forward price-to-earnings (P/E) ratio: A version of the price-to-earnings (P/E) ratio, used to value a company’s shares, that utilises forecasted earnings in its calculation.

GDP: Gross domestic product is a measure of the size and heath of a country’s economy over a specific period, usually three months or one year.

Inflation: The rate at which the prices of goods and services are rising in an economy. The Consumer Price Index (CPI) and Retail Price Index (RPI) are two common measures.

Interest rates: The amount charged for borrowing money, shown as a percentage of the amount owed. Base interest rates (the Bank Rate) are generally set by central banks, such as the Federal Reserve in the US, or Bank of England in the UK, and influence the interest rates that lenders charge to access their own lending or saving.

Net cash/debt: The net cash/debt of a company is calculated by subtracting its total cash and cash equivalents from its total short-term and long-term debt.

Onshoring / reshoring: The process of bringing business operations back in-house, or relocating them within domestic (or regional, in the case of the EU) borders. While it can be more expensive to run local operations, due to higher wages or the cost of regulation, it offers more control and helps to reduce the impact of geopolitical uncertainty or currency changes.

Premium: When the market price of a security is thought to be more than its underlying value, it is said to be ‘trading at a premium’. The opposite of discount.

Price-to-earnings (P/E) ratio: A popular ratio used to value a company’s shares, compared to other stocks, or a benchmark index. It is calculated by dividing the current share price by its earnings per share.

Purchasing power: This refers to how much you can buy with a specific amount of money. It goes up and down over time according to various economic factors, such as inflation.

Tariffs: A tax imposed by a government on goods imported from other countries.

Valuation metrics: Metrics used to gauge a company’s performance, financial health and expectations for future earnings, eg. price to earnings (P/E) ratio and return on equity (ROE).

Volatility: The rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility the higher the risk of the investment.

1Source: Bloomberg, Factset, Janus Henderson Investors Analysis, as at 30 September 2024.

2Source: Bloomberg, Factset and JP Morgan calculations, as at 30 March 2025.