Key takeaways:

- Since April 2025, a meaningful rotation in market leadership has favored small-cap and value stocks over large-cap growth. The rotation has been supported by artificial intelligence (AI) spending spillover, rate cut expectations, and tax refund stimulus – conditions we believe remain largely in place.

- Cyclical stocks dominate value benchmarks and stand to benefit if the Trump administration runs the economy hot. However, sustained high oil prices risk demand destruction and slower global growth.

- Quality small-cap stocks look inexpensive relative to lower-quality peers, and periods of rolling market volatility driven by AI disruption concerns may offer attractive entry points for longer-term investors.

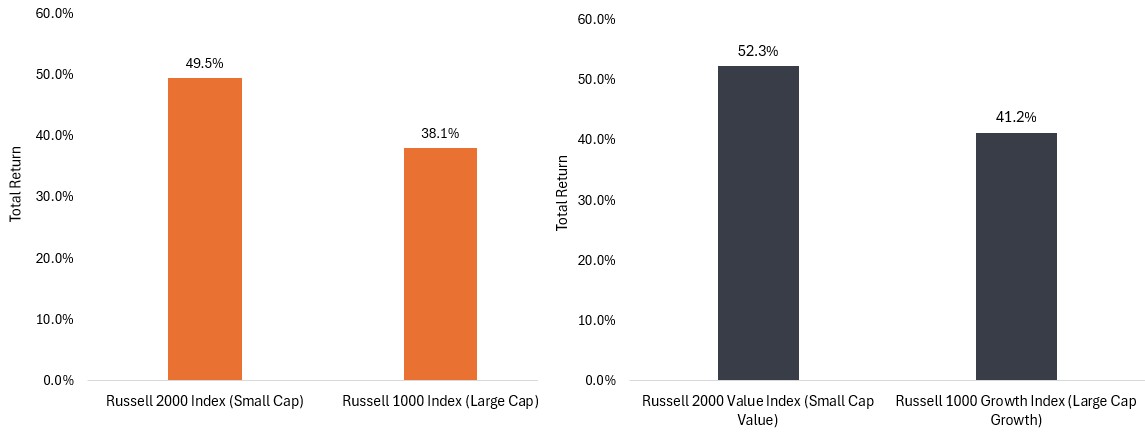

While broad U.S. equity indexes held relatively steady through February, the real action was happening below the surface: a rotation in market leadership away from large-cap growth and big tech toward small-cap and value stocks. Since the April 2025 equity market lows following Liberation Day, small-cap and small-cap value stocks have outperformed large-cap growth. We believe the fundamental case for that rotation remains intact – with one important caveat.

Exhibit 1: From April 2025 through February 2026, small cap outperformed large cap and small-cap value outperformed large-cap growth

Source: Bloomberg. Total Return performance data as of 8 April 2025 – 27 February 2026.

AI’s broader reach

For years, the playbook was straightforward: Buy large-cap growth stocks, particularly the so-called Magnificent Seven, and hold them (aka “set it and forget it”). These companies generated enormous free cash flow, and the market rewarded them accordingly.

That dynamic has changed. Heavy AI-driven capital spending has pressured free cash flow at the largest technology companies, and we don’t expect that to reverse soon. That shift, in our view, tilts the odds in favor of smaller market-cap stocks – even after the valuation gap between small and large cap has narrowed.

There’s another AI element to the rotation worth considering: The hundreds of billions of dollars being spent on AI infrastructure are flowing through the broader economy into sectors like utilities, industrials, and materials. These companies help support the data center buildout, benefiting many non-technology companies in the process.

The market is beginning to sort out winners and losers from AI adoption and has started more aggressively punishing companies it believes are at risk. We think a greater share of cyclical and value-oriented companies will end up beneficiaries rather than casualties.

The backdrop for cyclicals

We entered 2026 optimistic on cyclical stocks for several reasons. Chief among them is the fact that expectations for solid U.S. economic growth and higher tax refunds have provided a meaningful boost to lower-income consumers, a group whose economic health has lately been a source of considerable concern.

As a midterm election year, 2026 also brings its own political calculus. The Trump administration has shown a clear preference for lower interest rates and appears willing to run the economy hot, even as some signs suggest inflation may be stagnating or edging higher. That environment tends to benefit real assets and cyclicals, which carry more weight in value indexes than growth indexes.

Quality at a discount

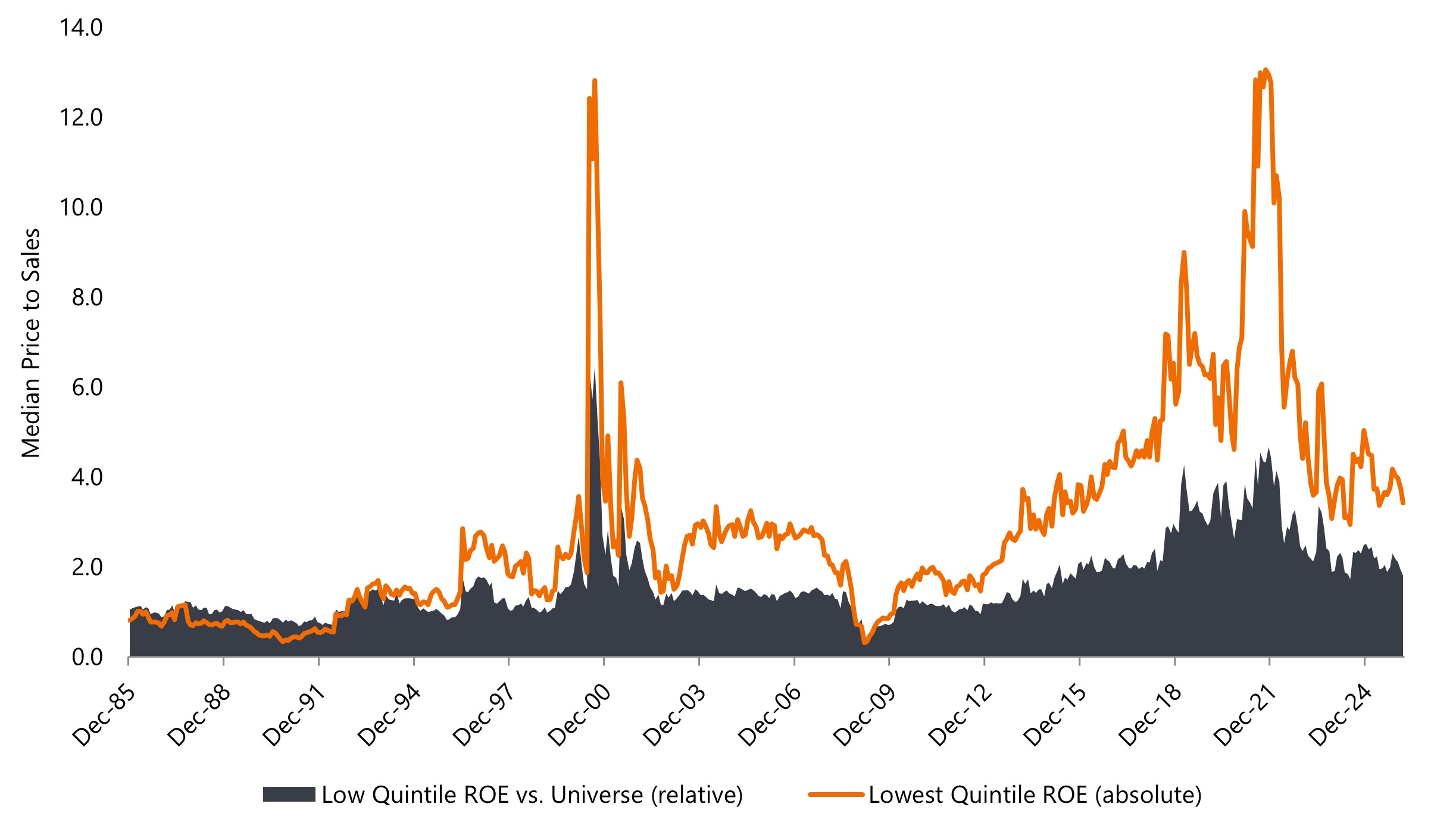

Within small caps, we focus specifically on quality, which we define as companies with strong balance sheets, consistent earnings, and reliable free cash flow generation. That emphasis has been a headwind over the past year, as lower-quality small-cap stocks commanded surprisingly rich valuations.

But we think that premium is unwarranted. Companies in the lowest tier of return on equity (ROE) have been priced as though the market environment will remain benign indefinitely. If lending standards tighten, private credit concerns spread, or geopolitical risks escalate, we’d expect unprofitable and leveraged companies to face a harder road. Quality, in our view, is simply too cheap right now.

Exhibit 2: The lowest quintile of small-cap companies based on ROE trades at 1.9x P/S above the universe on a relative basis as of February 2026

Source: FactSet; FTSE Russell; Jefferies. Note: Universe is Russell 2000; Data is Median Price to Sales (P/S); Highest ROE is Quintile 1 based on ROE.

Notably, periods of market volatility driven by AI disruption fears have created something of a silver lining for value investors. Rolling selloffs across industries have pushed quality companies to more attractive valuations, improving the shopping list for investors who understand the company fundamentals and are willing to look past near-term noise.

A word on the Middle East

The conflict in the Middle East has introduced real uncertainty into an otherwise constructive outlook. Rising oil prices are helping energy stocks but are likely to create economic headwinds elsewhere. Higher crude prices are stoking demand destruction concerns that have weighed on banks, industrials, and non-energy commodity companies since the beginning of March.

Sustained high energy prices also risk slowing gross domestic product (GDP) growth globally, and while the U.S. may be better positioned than most as both a producer and exporter of energy, it isn’t immune. A prolonged conflict means higher prices and weaker growth eventually find their way to the U.S. as well. Whether this conflict proves to be a speed bump for this small-cap and value market rotation or something more consequential depends largely on the war’s duration and intensity, and that’s difficult to forecast.

As it stands today, we remain cautiously constructive on both value and smaller-cap market stocks. The rotation that began last spring reflects a real shift in market fundamentals, and the conditions supporting it – including AI spending spillover, a pro-growth policy environment, and attractive valuations in quality small caps – remain largely in place. If the Iran conflict resolves in the near term, we believe this rotation has the potential to continue.

A quality factor captures the return premium associated with companies that exhibit strong, stable fundamentals—such as high profitability, low leverage, stable earnings, and efficient management. Typical metrics used include return on equity, return on invested capital, earnings variability, EPS growth, debt-to-equity ratio.

Return on Equity (ROE) is calculated as the earnings per share divided by the book price per share.

The Russell 2000 Index is a small-cap U.S. stock market index that is made up of the smallest 2,000 stocks in the Russell 3000 Index.

Volatility measures risk using the dispersion of returns for a given investment.

IMPORTANT INFORMATION

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Smaller capitalization securities may be less stable and more susceptible to adverse developments, and may be more volatile and less liquid than larger capitalization securities.

Value stocks can continue to be undervalued by the market for long periods of time and may not appreciate to the extent expected.