Key takeaways:

- The healthcare sector has experienced significant volatility so far in 2025, as the Trump administration weighs tariffs for pharmaceuticals and cuts funding for federal health agencies.

- Even so, many companies within the sector have delivered positive returns year to date, with some even posting double-digit gains.

- This year’s top performers share certain qualities, which we think investors should seek out for a shot at market-differentiated returns.

Lately, investing in the healthcare sector has felt like watching a nail-biter playoff series, with all the upsets that can come with one. Layoffs and funding cuts at health agencies such as the Food and Drug Administration (FDA) have weighed on development-stage biotech. An unexpected surge in medical costs led UnitedHealthcare, normally a pillar of defense in the sector, to sell off sharply. And the Trump administration’s plan to impose tariffs on pharmaceuticals (usually exempt from trade levies) has raised doubts about future biopharma earnings.

Yet, like any good series, there have been exhilarating moments, with some companies hitting medical milestones driving strong returns so far in 2025. We think the characteristics that have helped set these firms apart could continue to deliver over the near (and longer) term and are worth being noted by investors.

The MVP: Innovation

The first of these qualities is innovation. Although we have long said innovation is key to outperformance in healthcare, in today’s market, it has become essential. Many firms with breakthrough medical products that advance the standard of care for patients or address an unmet medical need have seen sizable returns so far this year, even as the S&P 500® Index has turned negative and the S&P 500 Healthcare sector has been marginally positive.1

Much of that comes down to the fact that today, many new drugs offer novel mechanisms of action with improved patient outcomes. Therapies are also targeting rare diseases or new, large market opportunities such as obesity, MASH (fatty liver disease), hypoparathyroidism, and autoimmune disease. The combination has led to strong sales.

Take Verona Pharma’s novel treatment, Ohtuvayre, for chronic obstructive pulmonary disease (COPD). Approved in June 2024, this non-steroidal anti-inflammatory drug represents the first new mechanism of action for COPD in more than 20 years. Given its dual benefits of improving breathing and reducing exacerbations, uptake has been rapid. In the second quarter of launch, sales rose 95% sequentially to $71 million, well above analyst forecasts of about $50 million. For the year through April 30, the stock climbed 53%.2

Sixty drugs are pending FDA review this year, and while concerns have grown about potential delays due to staffing cuts, newly confirmed FDA Commissioner Dr. Marty Makary has shown support for innovation through accelerated approval pathways for treatments in rare diseases and a focus on making the drug review process more efficient. If investors gain confidence the FDA can operate as expected under Dr. Makary, we believe even more development-stage biotech companies could benefit.

Attractive valuations

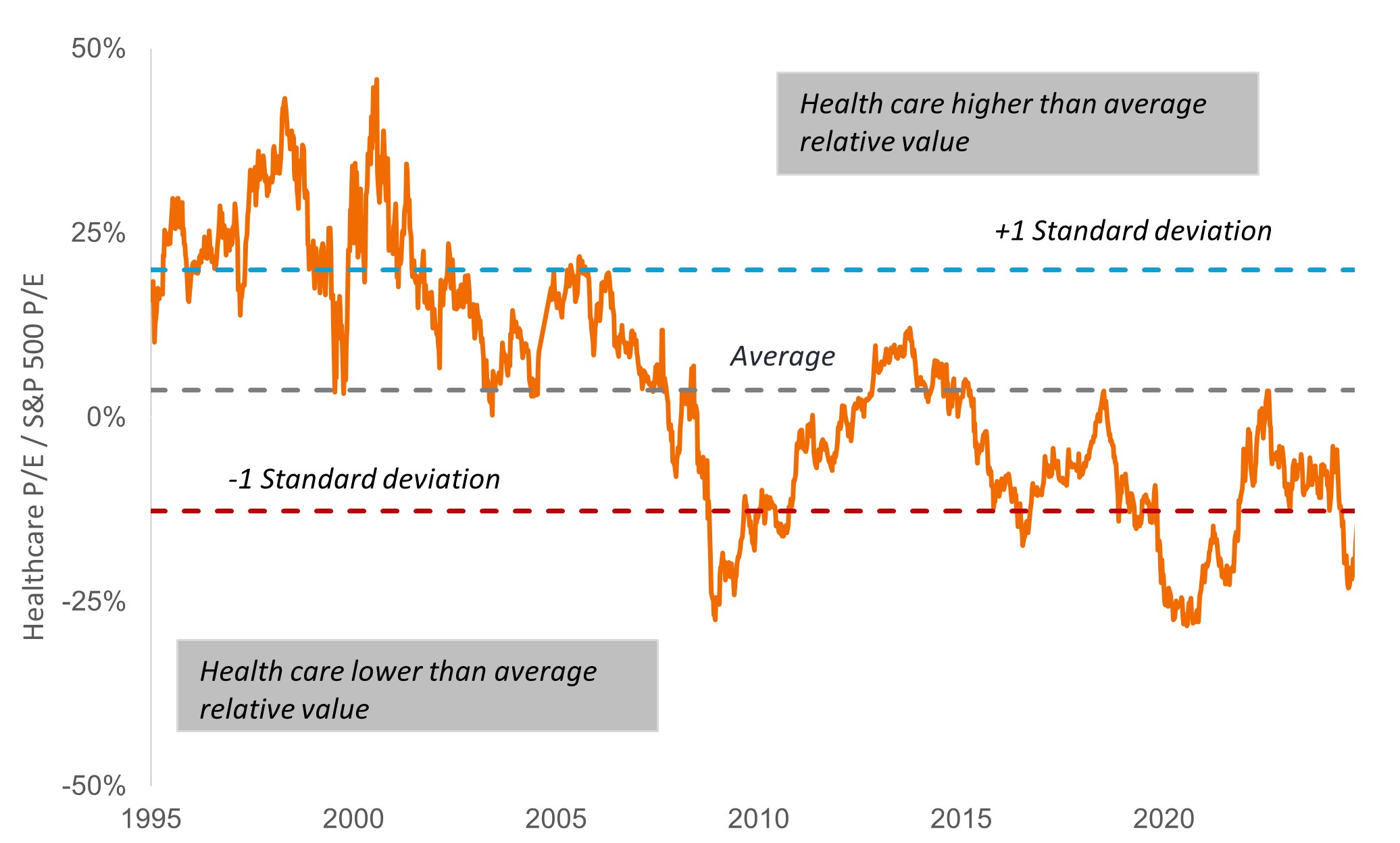

Also, key to healthcare returns are valuations, and here, the sector has the offensive advantage. Despite outperforming the S&P 500 so far this year, the healthcare sector trades at a nearly 20% discount to the benchmark versus the long-term average of a 4% premium (Exhibit 1). Some of the hardest-hit areas of the sector, such as emerging biotech, trade for even less.

Exhibit 1: Healthcare at a discount

Source: Bloomberg. P/E=price-to-earnings ratio. Healthcare=S&P 500 Healthcare Sector, which comprises those companies included in the S&P 500 that are classified as members of the GICS® health care sector. Data based on forward, 12-month earnings estimates and range from 2 June 1995 to 25 April 2025.

Starting from such low valuations, we believe healthcare stocks are primed for gains when there’s positive news, such as a surprise earnings beat or a strong data readout. Managed healthcare firms, for example, began 2025 with unusually low valuations after rising medical cost ratios (the percentage of premiums paid out for patient care) weighed on the stocks in 2024. Worries about funding cuts to Medicaid, the large government insurance program, and an earnings miss by industry-leader UnitedHealthcare led to further volatility in recent months. But year to date, many of these stocks are positive – with some even seeing double-digit gains – thanks to a recovery in earnings during Q1. Investors have also gravitated to managed care for their defensive qualities, as worries about recession have increased.

Policy resilience

Indeed, the healthcare sector is grappling with an unusual onslaught of policy uncertainty lately, including proposed funding cuts to federal health agencies and the growing likelihood that pharmaceuticals will be subject to tariffs for the first time in decades. We do not believe long-term investors should overhaul their portfolio based solely on policy shifts (which, as we’ve seen, can change quickly). But near term, we think investors should be mindful of companies that may be more resilient.

These include biopharmas with a large manufacturing presence in the U.S. and/or that maintain most of their intellectual property in the country, which could help insulate them from higher costs. Investors might also consider areas of the sector less exposed to tariffs, such as drug distributors. These companies operate domestically, facilitating the distribution of medicines from manufacturers to pharmacies. In addition, they are benefiting from new sources of revenue growth thanks to complex biologics, which require specialty handling.

Even then, we think investors should remember that with healthcare, policy is always nuanced. In fact, at the same time the Trump administration is weighing pharmaceutical tariffs, the president has also signed an executive order directing Congress and the Department of Health and Human Services to modify the “pill penalty” in the 2022 Inflation Reduction Act. The penalty – which provides small-molecule drugs (traditional pills) just nine years before Medicare price negotiations, versus 13 years for injectable biologics – is opposed by the industry. A change could protect pharma revenues and offer further incentives for the development of convenient pills in areas such as cancer and cardiovascular disease. Furthermore, the Trump administration has highlighted the strategic importance of the biopharma industry for U.S. national security, with a focus on rewarding U.S. manufacturing a key part of tariff policy.

Later-stage development

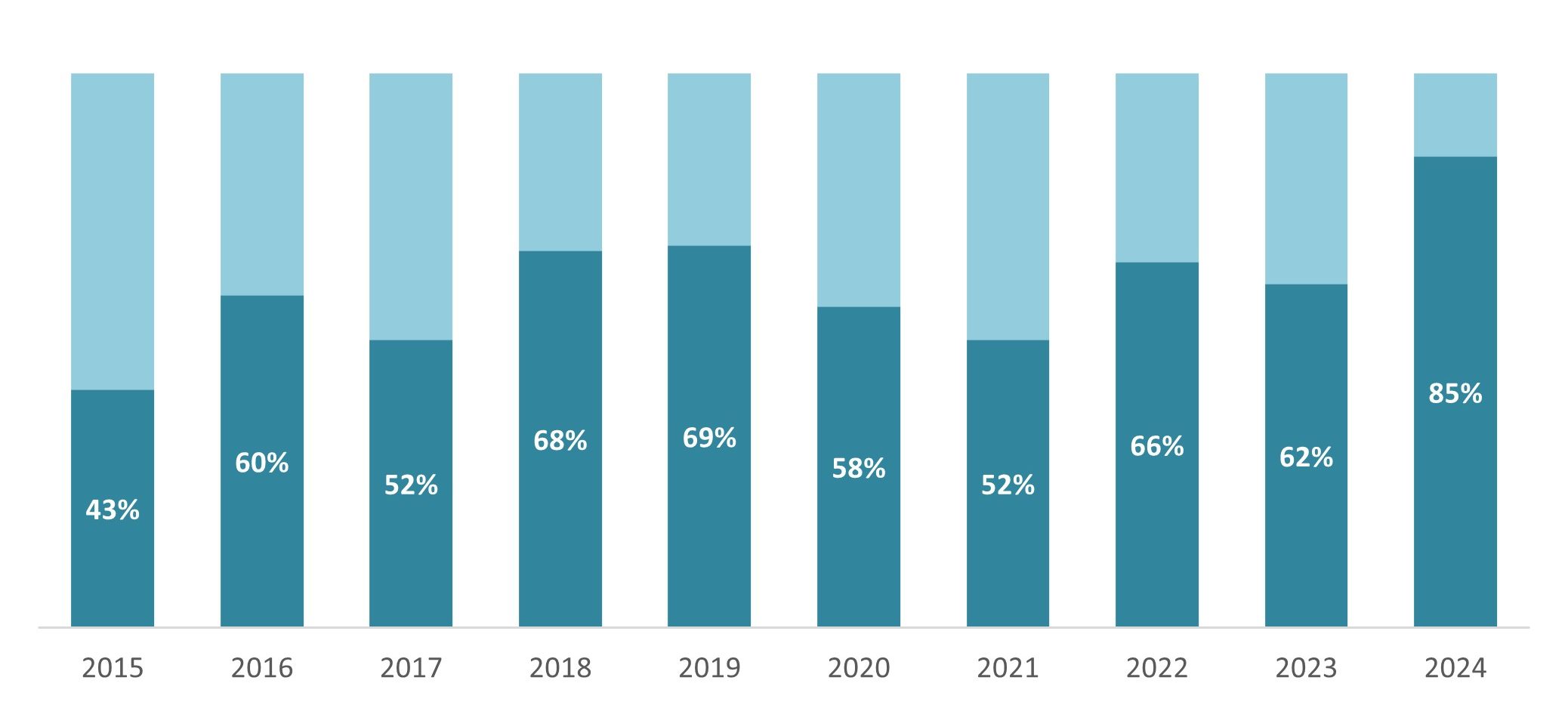

Another measure of resilience is pipeline development: how far along is a firm in getting a pipeline candidate to the market and/or does it have a product in market already? We continue to believe that small- and mid-cap biotechs are among the best sources of innovation within the sector: in 2024, 85% of new drugs were originated by these firms (Exhibit 2). But today, companies in the early stages of development could be more exposed to regulatory delays and downside risk, especially if a risk-off market persists.

Exhibit 2: Today, emerging biotech originates most new drugs

% of new active substances developed by small- and mid-cap firms

Source: IQVIA Institute, as of January 2025.

That is why for our final characteristic, we believe investors should emphasize late-stage development companies with a record of positive clinical data, or early commercial-stage companies with breakthrough products addressing unmet medical needs. Having already cleared some clinical and regulatory hurdles, these companies might be in better control of their own destinies – the proven scorers who, in a game with tight odds, might offer the best chance of making the shot when the game is on the line.

1 Bloomberg, data from 31 December 2024 to 30 April 2025.

2 Company earnings report, Bloomberg. Sales data are for the quarter ended 31 March 2025. Stock return data are from 31 December 2024 to 30 April 2025.

Price-to-Earnings (P/E) Ratio measures share price compared to earnings per share for a stock or stocks in a portfolio.

Health care industries are subject to government regulation and reimbursement rates, as well as government approval of products and services, which could have a significant effect on price and availability, and can be significantly affected by rapid obsolescence and patent expirations.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.