Key takeaways:

- US REITs outperformed in 1H, having started the year at historically depressed valuations and supported by healthy property-level fundamentals across most sectors.

- The sector’s outperformance in the face of rising government bond yields and central bank rate expectations challenges the view that REITs are merely a ‘rates trade’. Earnings growth, balance sheet strength and capital access are playing a meaningful role in performance.

- For investors, REITs may offer a useful combination of recovery potential, income and diversification at a time when broader equity markets remain concentrated, particularly to tech stocks.

While perhaps not as closely watched as the NBA Finals or the FIFA World Cup, the Janus Henderson Global Property Equities Team tends to view the annual NAREIT Reit Week conference, held in New York City each June, as the sector’s halfway point for the year.

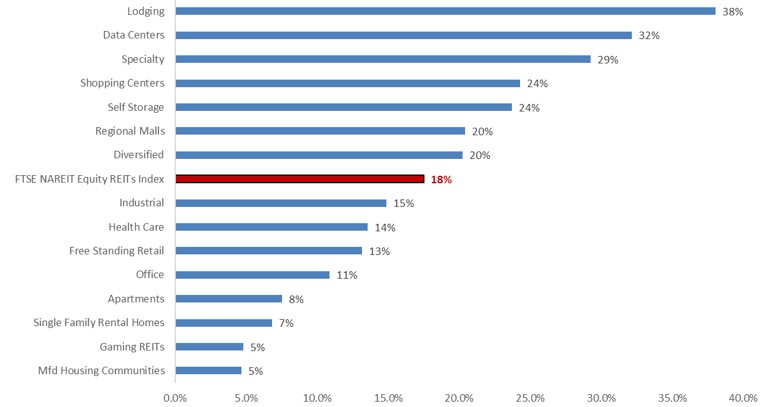

Year-to-date (YTD) through June 12, US real estate investment trusts (REITs) have gained 18%, with all property types delivering a positive return (Figure 1). This is double the YTD return of the S&P 500 Index, and has been achieved in spite of the US 10-Year Treasury yield rising from 3.9% in February to as high as 4.7% in May – pouring cold water on the notion that REITs are nothing but a ‘rates trade’ ((there is a conventional wisdom, which we view as oversimplified, that REITs typically look less attractive when rates rise, and vice versa).

Figure 1: REITs demonstrate strength beyond interest rate sensitivity

US REITs YTD total return by property type

Source: Bloomberg, Janus Henderson Investors, year-to-date property sector returns to 12 June 2026. Past performance does not predict future returns.

Following such a strong first half, it’s worth taking a look at the highlights to see how we got here:

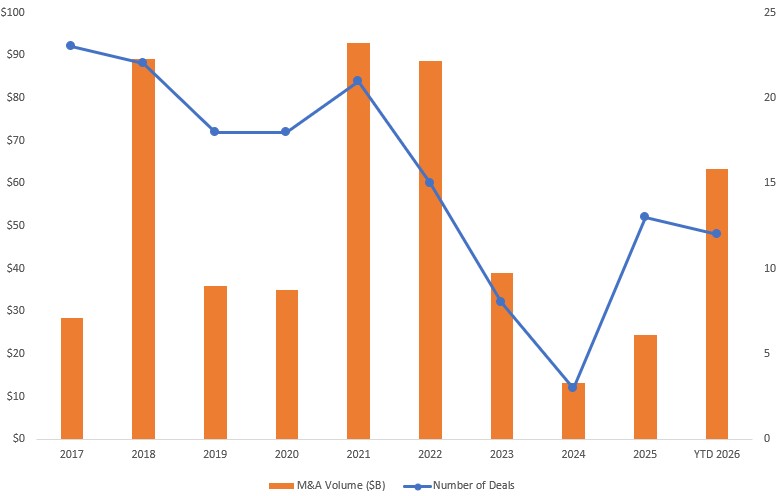

1. Game readiness – starting point matters: As we have written about previously, REITs entered 2026 as the equity sector which had de-rated the most post the US Federal Reserve rate-hiking cycle and was trading at its largest price-to-earnings (P/E) multiple discount to the S&P 500 seen in 25 years. While YTD 2026 performance has seen this begin to reverse, there remains a long way to go before we get back to “normalized” valuation spreads. Entity-level buyers have taken notice of REITs’ discounted prices, evidenced in the fact that 2026 is on pace to be the most active year for REIT merger and acquisitions (M&A) activity in the past decade (Figure 2).

Figure 2: Compelling valuations fuel increased M&A activity

REIT M&A activity by year

Source: S&P Capital IQ, Janus Henderson Investors. All US and Canadian REITs; includes deals based on announcement date, aggregate values in USD terms. Year-to-date as at 12 June 2026.

2. Focus on fundamentals: A key learning for our team from almost 50 meetings at the NAREIT conference is that the fundamental outlook for most property types remains healthy. This is evidenced by REIT’s projected 6.3% 2026 earnings growth, with 2027 growth projected to be at least as strong.1 This is even true for property types that many have loved to hate in recent years like Office, where vacancies seem to have found a bottom in almost all markets and Malls, where rents are rising nicely and foot traffic from Gen Z is ramping up – a promising sign for the future. Meanwhile, in the team’s view, “all-star” property types like Health Care and Data Centers currently show no signs of losing a step.

3. Food is fuel: US REITs have been avoiding junk food (excessive debt) for nearly 20 years post the Global Financial Crisis. Their balance sheets are built on equity with an average loan-to-value (LTV) of around 30%. This is in stark contrast to how privately-owned real estate is typically capitalized, where LTVs of 65% or higher are common. The low proportion of debt on listed REITs’ balance sheets is a key beneficial characteristic; it has enabled the asset class to weather moderate rate increases like what we have seen this year with comparative ease.

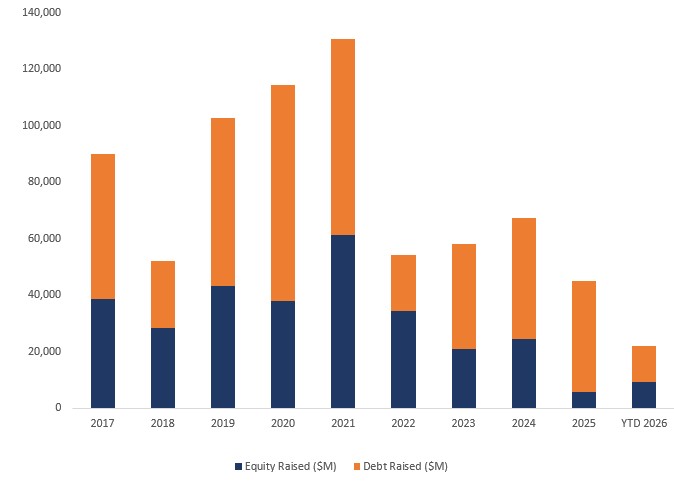

4. Great players make great plays: One of listed REITs’ greatest attributes is continuous access to capital. In 2025, the sector was very quiet on capital deployment with the bulk of issuance related to debt refinancing. 2026 started off differently. YTD equity issuance is already nearly double that of 2025’s total. (Figure 3) And unlike last year when capital raising was mostly for refinancing, 2026 capital raising has been more “offensive” and aimed at earnings growth via acquisitions. Notably, the sector has already seen three initial public offerings (IPOs) in 2026, which have traded between 10-27% above deal price at the time of writing. Our team believes an equity market that is demonstrably supportive of capital raises is a good sign for the overall health of the REIT sector.

Figure 3: Active capital markets enable REITs to play offence

Capital raising by listed REITs

Source: S&P Capital IQ, Janus Henderson Investors. All US and Canadian REITs; values in USD terms. Year-to-date as at 12 June 2026.

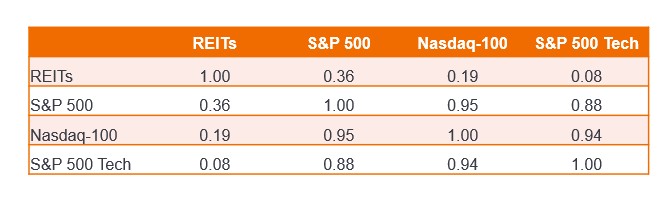

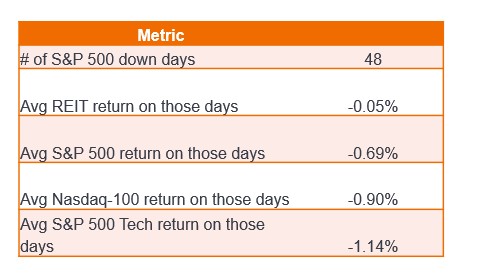

5. REITs are a role player: One role of REITs in a portfolio is to provide diversification. REITs have historically been among the least correlated to Technology stocks; we saw this play out in 1H 2026 with the sector still delivering solid absolute returns. (Figure 4) REITs exhibited close to zero correlation with Tech and very low correlations with broader equity indices. Furthermore, REITs have seen less drawdown than broader indices and tech this year, and on days when the market is down, REITs have been down much less, on average. (Figure 5)

Figure 4: REITs provide balance amid tech-driven markets

YTD corelation matrix (daily returns)

Source: Bloomberg, Janus Henderson Investors analysis, 2 Jan 2026 to 12 June 2026. Past performance does not predict future returns.

Figure 5: REITs demonstrate resilience with low correlation and smaller drawdowns

Maximum drawdown (peak-to-trough decline YTD)

Source: Bloomberg, Janus Henderson Investors analysis, 2 Jan 2026 to 12 June 2026. Past performance does not predict future returns.

Average daily return on S&P 500 down days

Source: Bloomberg, Janus Henderson Investors analysis, 2 Jan 2026 to 12 June 2026. Past performance does not predict future returns.

Like a veteran athlete you’ve watched for years: familiar, dependable, and well-tested

We are not surprised by what we’ve seen from US REITs so far this year. They started out at a historically cheap valuation, acted as a portfolio diversifier, continued to deliver steady fundamental growth, and provided investors with a yield of nearly 4%. Now we observe the sector beginning to go on offense with opportunistic capital raises that aim to enhance future returns. While no one can predict the future, these factors position REITs well to potentially sustain this momentum into the second half of 2026.

IMPORTANT INFORMATION

Yields may vary and are not guaranteed.

REITs or Real Estate Investment Trusts invest in real estate through direct ownership of property assets, property shares or mortgages. As they are listed on a stock exchange, REITs are usually highly liquid and trade like shares.

Real estate securities, including Real Estate Investment Trusts (REITs), are sensitive to changes in real estate values and rental income, property taxes, interest rates, tax and regulatory requirements, supply and demand, and the management skill and creditworthiness of the company. Additionally, REITs could fail to qualify for certain tax-benefits or registration exemptions which could produce adverse economic consequences.

FTSE Nareit All Equity REITs Index tracks the performance of the U.S. real estate investment trust (REIT) market.

1 Source: S&P CapitalIQ as June 12, 2026.

Balance sheet: A financial statement that summarises a company’s assets, liabilities, and shareholders’ equity at a particular point in time. The balance sheet can be used to gauge a company’s financial position.

Correlation: How far the price movements of two variables (e.g., equity or fund returns) move in relation to each other. A correlation of +1.0 means that both variables have a strong association in the direction they move. If they have a correlation of –1.0, they move in opposite directions. A figure near zero suggests a weak or non-existent relationship between the two variables.

De-rating: The downward adjustment of a company’s financial ratios, such as the price-to-earnings (P/E) ratio, in response to business or market uncertainty.

Diversification: Spreading investments across different asset types or securities to reduce exposure to any single risk.

Dividend yield: The income received on an investment relative to its price, expressed as a percentage. It enables comparisons of the level of income provided by different investments such as equities, bonds, cash, property, or between funds at a point in time.

Equity and debt capital: Businesses raise capital mainly through equity financing and debt financing, typically a combination is used depending on cash flow needs and ownership preferences.

Government bond yield: The interest rate on a government bond after accounting for its market price. Typically, a higher “risk-free” return/yield from government bonds decreases the appeal of the riskier returns on offer from REITs.

Initial public offering (IPO): The first time a private company offers shares to the public on a stock exchange.

Loan-to-value (LTV): A measure of debt relative to the value of an asset; in real estate, lower LTVs generally indicate more conservative financing.

Mergers and acquisitions (M&A): Transactions in which companies or major assets are combined, bought or absorbed. [investopedia.com]

Maximum drawdown: The largest decline in the value of an investment from its peak to its lowest point before a recovery

Price-to-earnings (P/E) ratio: A valuation measure comparing a company’s share price with its earnings per share. [investopedia.com]

Refinancing: The process of replacing and renegotiating terms for existing loans.

Total return: The overall return from an investment, combining price appreciation and income such as dividends.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- This Fund may have a particularly concentrated portfolio relative to its investment universe or other funds in its sector. An adverse event impacting even a small number of holdings could create significant volatility or losses for the Fund.

- The Fund invests in real estate investment trusts (REITs) and other companies or funds engaged in property investment, which involve risks above those associated with investing directly in property. In particular, REITs may be subject to less strict regulation than the Fund itself and may experience greater volatility than their underlying assets.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- This Fund may have a particularly concentrated portfolio relative to its investment universe or other funds in its sector. An adverse event impacting even a small number of holdings could create significant volatility or losses for the Fund.

- The Fund invests in real estate investment trusts (REITs) and other companies or funds engaged in property investment, which involve risks above those associated with investing directly in property. In particular, REITs may be subject to less strict regulation than the Fund itself and may experience greater volatility than their underlying assets.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund invests in real estate investment trusts (REITs) and other companies or funds engaged in property investment, which involve risks above those associated with investing directly in property. In particular, REITs may be subject to less strict regulation than the Fund itself and may experience greater volatility than their underlying assets.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.