Key takeaways:

- AI infrastructure spending is accelerating faster than markets expected, with hyperscaler capex forecasts more than doubling since early 2025, driving unprecedented funding requirements.

- Rising tech debt issuance is likely to increase supply pressure, potentially keeping investment grade technology spreads wider than other corporate sectors despite strong underlying company fundamentals.

- This heavy supply may favor allocating to sectors where supply dynamics are more supportive or selectively capturing opportunities in high yield and securitized markets.

Back in November 2025 we warned about the level of capital raising that would be needed to fund the artificial intelligence (AI) buildout and how supply from tech companies – particularly the hyperscalers – was set to reshape the technical picture for corporate credit. While we were right to be cautious, the market, if anything, underestimated the level of tech supply and we argue might still be doing so.

It’s all relative

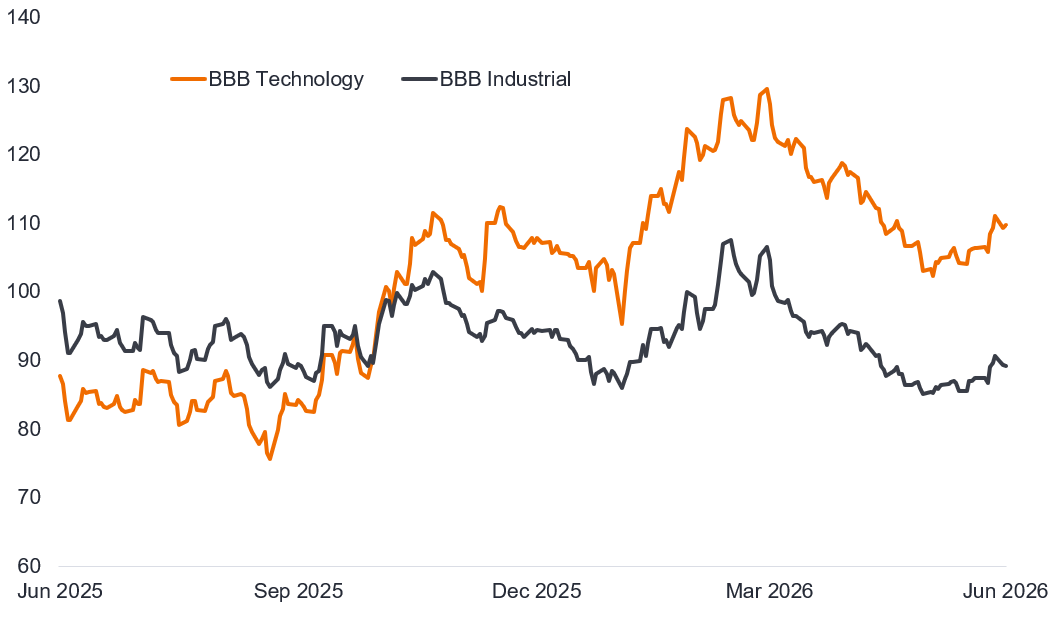

Our caution toward investment grade tech proved to be the right call as spreads on investment grade (IG) industrials have tightened since November while tech has seen a noticeable widening. For example, BBB spreads on tech and industrials were both around 100 basis points back in November, yet tech has gapped 10 basis points wider to end June 2026, while industrials have tightened around the same over that period.

Figure 1: Tech spreads widen versus industrials

US investment grade BBB spreads (basis points)

Source: Bloomberg, Bloomberg US Investment Grade Technology BBB Index, Bloomberg US Investment Grade Industrial BBB Index, Option-adjusted spread (OAS) over Treasuries in basis points, 30 June 2025 to 30 June 2026. One basis point = 0.01%, 100 bps = 1%. Past performance does not predict future returns.

One direction – AI capex trends higher

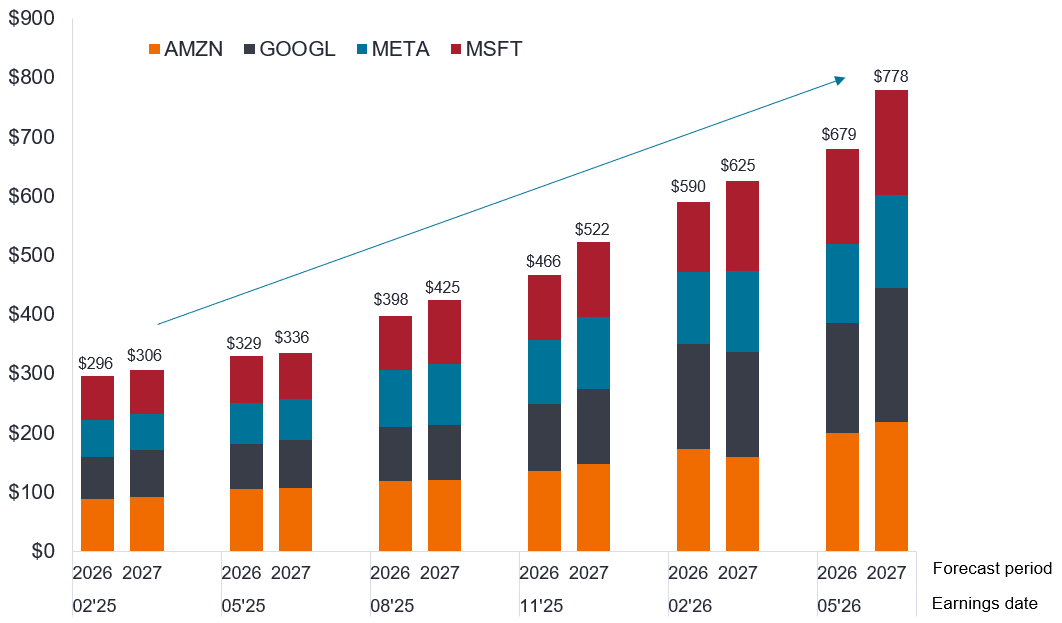

Driving the pressure on tech related spreads has been the sheer scale of capex spending. The following chart reveals how much estimated capex spending projections have risen over the course of the last 18 months. The projections are derived from market estimates around each quarterly earnings period for the Big 4 hyperscalers. Back in February 2025, the market was predicting around US$300 billion in capex in 2026 and 2027. Fast forward to May 2026 and the market is anticipating more than double the level of capex it suggested back in February 2025.

Figure 2: Hyperscaler capex estimates trending higher

Big 4 capex estimates (US$ billion)

Source: Bloomberg, S&P Capital IQ sellside consensus estimates, Janus Henderson Investors, Big 4 = Amazon, Google (Alphabet), Meta, Microsoft, February 2025 to May 2026. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. There is no guarantee that past trends will continue, or forecasts will be realized.

The race to build out AI is unlikely to ease, particularly as some of the questions around payback may begin to fade. One of the big AI companies, Anthropic (only founded as recently as 2021) has seen its revenue balloon and is anticipating moving into quarterly operating profit for the first time, potentially as soon as its next set of results.1 Anthropic is one of several large clients of the hyperscalers, so strong unit economics combined with unprecedented growth at scale should underpin continued demand. More anecdotally, companies are noticing that if they are not using AI they risk being left behind. This is increasing uptake and leading to heavy demand for the level of compute available, particularly as more users use advanced agents rather than simpler chat. Monetising compute is therefore becoming less of a concern, but users are noticing that bills are rising as greater usage outstrips the fall in the cost of tokens (the basic metric of AI input and output). The bottleneck remains available compute, creating demand for the AI buildout.

Working with big numbers

Organic cash flow can pay for some of the AI capex but even the cash-generative hyperscalers are having to tap capital markets. Barclays reckons the Big 4 hyperscalers together with Oracle, will issue around $240 billion in IG bonds this year alone.2

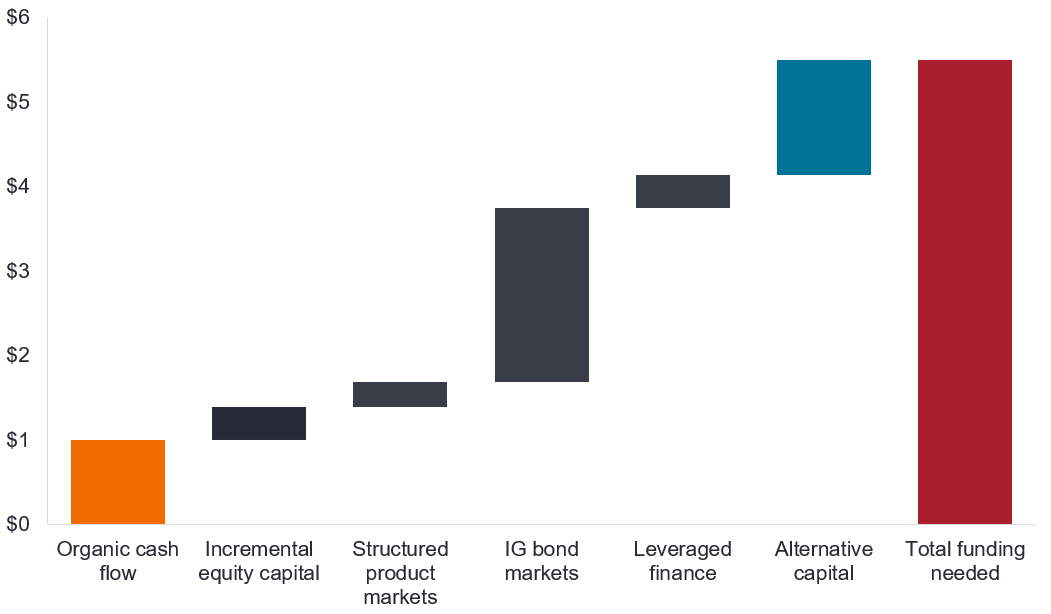

Widening the remit more broadly to cover hyperscalers, data center owners and potential chip financing and J.P. Morgan reckons organic cash flow will represent around one fifth of $5.5 trillion of capex funding over the next five years, with IG bonds needing to fund almost two fifths, around $2.1 trillion, and incremental equity capital around $400 billion. The rest to be made up of funding from leveraged finance, securitized markets and alternative capital.3

Figure 3: Anticipated AI capex funding sources (US$ trillion)

Source: J.P. Morgan, 17 June 2026. There is no guarantee that past trends will continue, or forecasts will be realized.

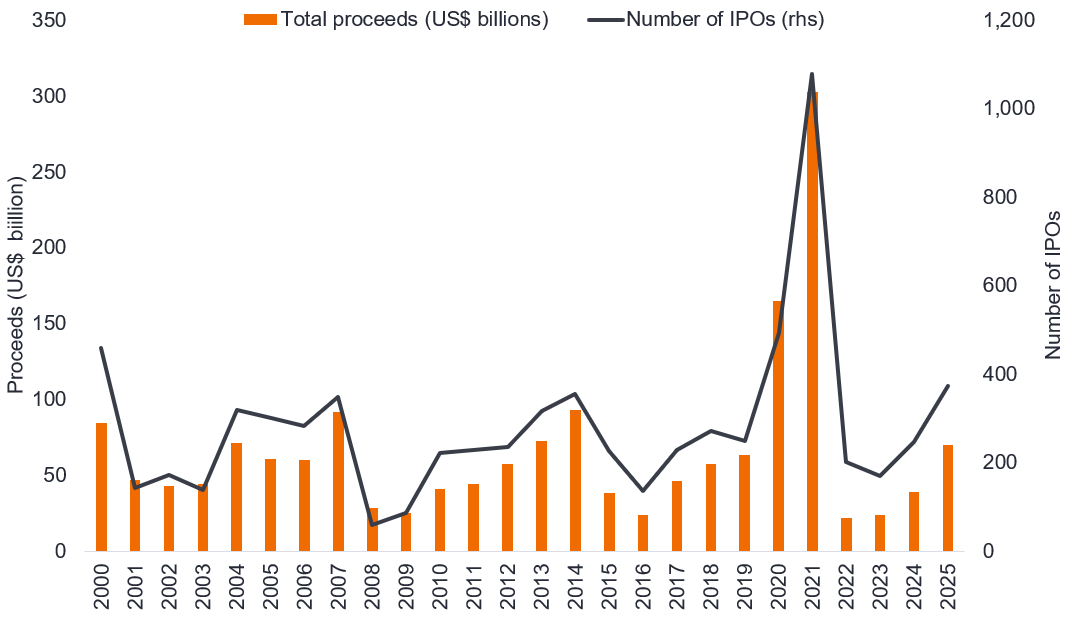

These are all big numbers. The demands on the IG bond market are coming at a time when the US equity market is set to make a bigger call on investors. Many of the hyperscalers are beginning to undo years of carefully manicured capital allocation, with share buybacks now making way for share issues. Alphabet alone raised US$85 billion in equity in the first half of 2026.4 Meanwhile, SpaceX raised US$86 billion through its initial public offering (IPO) once over-allotments are included.5 Based on the chart below the SpaceX IPO alone would catapult 2026 into the biggest year for IPO proceeds since 2021. The second half of this year already has potentially huge IPOs from Anthropic and OpenAI (ChatGPT) waiting in the wings, although the latter may delay until 2027.

Figure 4: US IPO proceeds (US$ billion) and number

Source: SEC, US Initial public offering (IPO) proceeds, calendar years, 2000 to 2025.

Credit markets, therefore, are not just competing for attention among fixed income investors but also having to contend with an equity market that is itself looking for historically high levels of funding. And this comes at a time when the US economy is showing signs of a pickup, so demands for working capital increase.

Diversification and concentration

The pressure on companies is reflected in the diversification in funding. Jumbo issues are being denominated in multiple currencies. In some respects, this is helpful because it widens exposure of the AI story to European investors looking for EUR and GBP issues. It is also creating opportunities within high yield and securitized, both directly in AI capex and wider infrastructure and energy requirements. Returning to the earlier point on monetisation, it is possible that some of the high yield-rated projects might get upgraded to investment grade as they near completion – ironically further swelling the proportion of tech within investment grade.

As of 30 June 2026, technology made up ~10% of the US Corporate Index (banking is the highest at ~22%). The US Corp Index is US$7.6 trillion in size, while tech is ~US$767 billion.6 So three years of $250bn+ (on the conservative side) in issuance doubles the technology market and likely pencils to a high-teens percentage of the index, or double where it is today. Investors tend to be wary of sectors that see an explosion of debt (think telecoms or energy in the mid-2010s) and typically demand a premium for lending. While many of larger AI-related borrowers retain enviably strong balance sheets, it is challenging not to envision spreads on IG tech going wider.

1Source: Wall Street Journal “Mind-blowing growth is about to propel anthropic into its first profitable quarter”, 20 May 2026.

2Source: Barclays, 21 May 2026. There is no guarantee that past trends will continue, or forecasts will be realized.

3Source: J.P. Morgan, 17 June 2026. There is no guarantee that past trends will continue, or forecasts will be realized.

4Source: Alphabet press release, 2 June 2026.

5Source: SpaceX press release, 15 June 2026.

6Source: Bloomberg, Bloomberg US Corporate Index, market value weights in US dollars,30 June 2026.

Note: Après-moi, le déluge (After me, the deluge) is a phrase attributed to King Louis XV of France. This phrase of indifference to excess was seen as a portend of the revolution to come.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Bloomberg US Corporate Bond Index: This measures the investment grade, fixed rate, taxable, corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

Balance sheet: Typically an accounting reference relating to assets versus liabilities for an entity, whether a household or a corporation.

Capex: Money a business spends on major, long-term assets such as property and equipment (tangible assets) or technology, software, trademarks, patents etc (intangible assets) to facilitate new projects or investments that support business growth and expansion.

Cash flow: The net balance of cash that moves in and out of a company. Positive cash flow shows more money is moving in than out, while negative cash flow means more money is moving out than into the company.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit rating: A score given by a credit rating agency such as S&P Global Ratings, Moody’s and Fitch on the creditworthiness of a borrower. For example, S&P ranks investment grade bonds from the highest AAA down to BBB and high yields bonds from BB through B down to CCC in terms of declining quality and greater risk, i.e. CCC rated borrowers carry a greater risk of default.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Hyperscaler: Technology providers that provide IT architectures that scale dynamically to handle exponential increases in workload and data. Apart from capacity, they offer enterprise-grade cloud services, flexible hardware resources, and robust software environments that support a broad range of AI applications.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

Inflation: The rate at which prices of goods and services are rising in the economy.

Investment grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

IPO, or initial public offering: The term for the first time that a private company sells shares of its stock to the public on a stock exchange.

Issuance: The act of making bonds available to investors by the borrowing (issuing) company, typically through a sale of bonds to the public or financial institutions.

Jumbo issue: A large bond issue, typically above US$1 billion in size.

Leveraged finance: Sub-investment grade debt, such as high yield bonds and leveraged loans.

Fundamentals: In the context of corporate debt, “fundamentals” refer to the essential financial health indicators and characteristics of a company that suggest its ability to meet debt obligations.

Securitization: The process in which certain types of assets are pooled so that they can be repackaged into interest-bearing securities. The interest and principal payments from the assets are passed through to the purchasers of the securities.

Share buyback: Where a company buys back their own shares from the market.

Technicals: The overall demand (appetite from investors) and supply (issuance of bonds and debt securities from borrowers) environment.

Treasuries/US Treasury securities: Debt obligations issued by the US government. Treasury bills and US government bonds are guaranteed by the full faith and credit of the US government. They are generally considered to be free of credit risk and typically carry lower yields than other securities.

Unit economics: Direct revenues and costs of a business measured on a per unit basis. It can relate to different variables but is often associated with customer lifetime value (the average amount of money earned per customer over the lifetime of the business relationship) divided by the customer acquisition cost.

Working capital: The money available in a business to fund daily operations and meet short-term obligations.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate.