Kernpunten

- While there are plenty of positive market developments, investors must remain vigilant about the underappreciated risk of rapid and significant market disruptions, driven by geopolitical tensions.

- An environment of heightened volatility and stock dispersion is favourable for strategies capable of combining rigorous fundamental analysis with flexibility to capture both long and short opportunities.

- Absolute return strategies can help to mitigate risk when traditional equity and fixed income correlations turn positive, strengthening portfolio resilience in uncertain markets.

As we look ahead to 2026, the investment environment remains highly complex, shaped by persistent macroeconomic and geopolitical uncertainties. Sovereign debt concerns, tariff risks, and AI-driven market dynamics continue to dominate headlines. The role and impact of fiscal and monetary policy remains crucial, particularly from the US Federal Reserve, given pressure from the US government to cut rates at a faster pace. These elements contribute to an environment of elevated volatility and dispersion, providing fertile ground for active management and stock picking.

More broadly, we see the role of absolute return strategies evolving, not just as a lower-risk equity proxy, but used more for their diversification benefits. Investors are increasingly seeking these strategies to navigate the complex landscape, in pursuit of consistent real returns, regardless of market direction. This shift highlights the growing importance of diversification and risk mitigation in portfolios, particularly relevant when during periods of positive correlation between equities and fixed income.

Opportunities across regions and sectors

In 2026, compelling opportunities are likely to arise from the increased stock dispersion and heightened volatility in global markets. Higher stock dispersion allows for more nuanced stock selection based on fundamentals, rather than broad sector trends. This kind of environment is highly favourable for equity long/short strategies, as they can exploit both long and short positions driven by fundamental analysis. The focus on company-specific factors, such as management quality, margin structure, and valuation, will be crucial, allowing skilled stock pickers to differentiate performance.

In the US, the evolving economic landscape, characterised by potential interest rate cuts and a cooling labour market, presents opportunities in sectors beyond the dominant technology firms.

In Europe, the prospects in the defence and financial sectors seem promising, given increased government spending and deregulation initiatives. The UK market, with its broad international revenue exposure, offers diversified optionality across sectors. The impact of a weakening dollar has reduced the value of foreign earnings for UK corporations when converted back to sterling. A stronger dollar could prove supportive for UK equities, specifically among businesses with significant US dollar revenue exposure, potentially reversing a headwind observed throughout much of the year.

Geopolitical shocks – the underappreciated risk

Possibly the most underappreciated risk for 2026 is the potential for geopolitical tensions to escalate unexpectedly, creating significant disruptions across global markets. 2025 provided a taster of what that could look like, with short-sharp shocks around US tariff threats and concerns related to the big ‘MAG7’ US tech stocks that are dominating markets. Investors held their breath in November 2025 in anticipation of Nvidia’s quarterly results, so if the momentum for the AI super-cycle shows even a hairline crack, we would expect markets to react.

This risk is exacerbated by the interconnectedness of global economies, where a regional conflict or policy change could ripple through markets worldwide. Unexpected tariffs or sanctions could disrupt trade flows, impacting earnings for multinational corporations and leading to market volatility. This a particular concern for highly concentrated markets, like the US, where overall market performance is dominated by a small number of mega-cap tech stocks. As such, we see maintaining a highly liquid, dynamic and diversified portfolio in more volatile periods as crucial to managing risk effectively.

Indicators of a new market regime

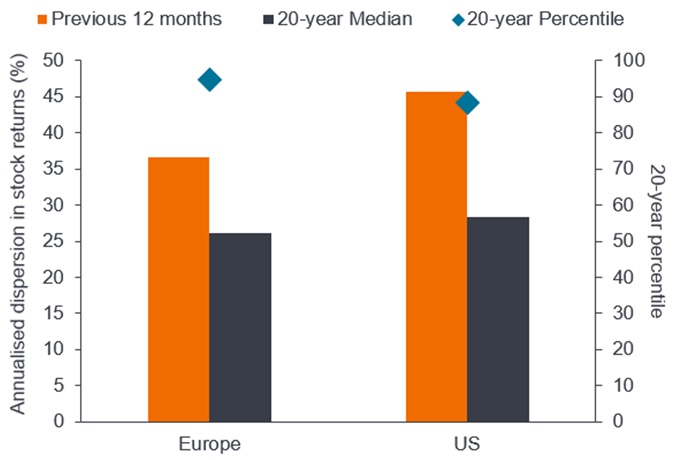

Gone are the days of rising tides lifting all boats, where just being active in the right market was sufficient to see the value of your portfolio rise. Stock dispersion remains elevated relative to history, emphasising the importance of stock selection as a primary driver of returns. Investors are paying much closer attention to results than they have at any point since the Global Financial Crisis, emphasising the importance of good stock selection.

Exhibit 1: Stock dispersion is at its highest level in decades

Source: Morgan Stanley Alpha, FactSet, as at 26 August 2025, RHS 30 June 2025. Past performance does not predict future returns.

Active management and adaptability

In a landscape characterised by heightened volatility and stock dispersion, the ability to capitalise on both long and short opportunities becomes increasingly valuable. Absolute return strategies offer the potential for consistent real returns regardless of market direction, providing diversification benefits and risk mitigation, especially when equities and fixed income exhibit unhelpful correlations.

As we look ahead to 2026, we believe that investors should focus on strategies that prioritise fundamental analysis, with the flexibility to adapt to changing market conditions. With fundamentals driving share prices more than broad market trends, the skill of stock pickers in identifying undervalued opportunities and managing risks is paramount. Engaging with experienced managers who can leverage these dynamics could be crucial for achieving differentiated performance and enhancing portfolio resilience.

Absolute return: The total return of a portfolio over a specified period as opposed to its relative return against a benchmark. It is measured as a gain or a loss and stated as a percentage of a portfolio’s total value.

Correlation: How far the price movements of two variables (eg. equity or fund returns) move in relation to each other. A correlation of +1.0 means that both variables have a strong association in the direction they move. If they have a correlation of –1.0, they move in opposite directions. A figure near zero suggests a weak or non-existent relationship between the two variables.

Stock dispersion: How much the returns of each variable (e.g., stocks in a benchmark) differ from the average return of the benchmark.

Global Financial Crisis: The global economic crisis from mid-2007 to early 2009 that began with losses related to mortgage-backed financial assets in the US and spread to affect financial markets and banks globally. Also known as the ‘Great Recession’.

Long/short: A portfolio that can invest in both long and short positions. The intention is to profit from combining long positions in assets in the expectation that they will rise in value, with short positions in assets expected to fall in value. This type of investment strategy has the potential to generate returns regardless of moves in the wider market, although returns are not guaranteed.

MAG 7: The term ‘Magnificent Seven’ refers to the seven major technology stocks – Apple, Microsoft, Nvidia, Amazon, Tesla, Alphabet, and Meta – that have dominated markets in recent years.

Mega-cap: The largest designation for companies in terms of market capitalisation. Companies with a valuation (market capitalisation) above $200 billion in the US are considered mega caps. These tend to be major, highly recognisable companies with international exposure, often comprising a significant weighting in an index.

Short position: Fund managers use this technique to borrow then sell what they believe are overvalued assets, with the intention of buying them back for less when the price falls. The position profits if the security falls in value.

Importheffing: een belasting of heffing die door een overheid wordt geheven op goederen die uit andere landen worden geïmporteerd.

Valuation: The process of determining the value of an asset, whether that is a company, investment, property, loan, as opposed to its current market value.

Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility, the higher the risk of the investment.

Dit zijn de standpunten van de auteur op het moment van publicatie en kunnen verschillen van de standpunten van andere personen/teams bij Janus Henderson Investors. Verwijzingen naar individuele effecten vormen geen aanbeveling om effecten, beleggingsstrategieën of marktsectoren te kopen, verkopen of aan te houden en mogen niet als winstgevend worden beschouwd. Janus Henderson Investors, zijn gelieerde adviseur of zijn medewerkers kunnen een positie hebben in de genoemde effecten.

Resultaten uit het verleden geven geen indicatie over toekomstige rendementen. Alle performancegegevens omvatten inkomsten- en kapitaalwinsten of verliezen maar geen doorlopende kosten en andere fondsuitgaven.

De informatie in dit artikel mag niet worden beschouwd als een beleggingsadvies.

Er is geen garantie dat tendensen uit het verleden zich zullen doorzetten of dat prognoses worden gehaald.

Reclame.

Belangrijke informatie

Lees de volgende belangrijke informatie over fondsen die vermeld worden in dit artikel.

- Aandelen/deelnemingsrechten kunnen snel in waarde dalen en gaan doorgaans gepaard met hogere risico's dan obligaties of geldmarktinstrumenten. Als gevolg daarvan kan de waarde van uw belegging dalen.

- Als een Fonds een hoge blootstelling heeft aan een bepaald land of een bepaalde geografische regio, loopt het een hoger risico dan een Fonds dat meer gediversifieerd is.

- Het Fonds kan gebruikmaken van derivaten om zijn beleggingsdoelstelling te verwezenlijken. Dit kan leiden tot hefboomwerking, wat de resultaten van een belegging kan uitvergroten en waardoor de winsten of verliezen van het Fonds groter kunnen zijn dan de kosten van het derivaat. Het gebruik van derivaten gaat ook gepaard met andere risico's, waaronder met name het risico dat een tegenpartij bij derivaten niet in staat is om haar contractuele verplichtingen na te komen.

- Als het Fonds activa houdt in andere valuta's dan de basisvaluta van het Fonds of als u belegt in een aandelenklasse/klasse van deelnemingsrechten in een andere valuta dan die van het Fonds (tenzij afgedekt of 'hedged'), kan de waarde van uw belegging worden beïnvloed door veranderingen in de wisselkoersen.

- Wanneer het Fonds, of een afgedekte aandelenklasse/klasse van deelnemingsrechten, tracht de wisselkoersschommelingen van een valuta ten opzichte van de basisvaluta te beperken, kan de afdekkingsstrategie zelf een positieve of negatieve impact hebben op de waarde van het Fonds vanwege verschillen in de kortetermijnrentevoeten van de valuta's.

- Effecten in het Fonds kunnen moeilijk te waarderen of te verkopen zijn op het gewenste moment of tegen de gewenste prijs, vooral in extreme marktomstandigheden waarin de prijzen van activa kunnen dalen, wat het risico op beleggingsverliezen verhoogt.

- Het Fonds kan geld verliezen als een tegenpartij met wie het Fonds handelt niet bereid of in staat is om aan zijn verplichtingen te voldoen, of als gevolg van een fout in of vertraging van operationele processen of verzuim van een derde partij.