Kernpunten

- Dissent at Japan’s latest monetary policy committee meeting could signal a potential policy shift, as structural wage growth compels the BoJ to consider rate hikes to prevent overheating, while helping to sustain economic progress.

- International pressure, particularly from the US, has highlighted demand for Japan to pursue a path of tighter monetary policy to address persistent inflation and support the yen.

- Japanese financial institutions, banks in particular, could be well-positioned to benefit, as rising yields boost profitability by widening net interest margins, enhancing returns on their cash reserves and bond holdings.

In recent years, dissent within the Bank of Japan’s (BoJ’s) Monetary Policy Meetings (MPMs) has emerged as a powerful signal of change. Historically, the BoJ has operated with a high degree of consensus, but when two or more board members have a differing view, it often marks a turning point towards monetary policy.

We saw signs of this in the latest September meeting, where Naoki Tamura and Hajime Takata voted for an immediate rate hike to 0.75%, against the majority’s decision to hold at 0.5%. Although we did not see a hike, the decision was accompanied by a surprise announcement from the BoJ to begin selling exchange-traded funds (ETFs) and Japanese Real Estate Investment Trusts (J-REITs). The immediate market reaction was negative on the news, but when looking at the pace of the new divestment programme it aligns with previous programmes, and the BoJ is focused on minimising the market impact. But more importantly, these ETF and J-REIT sales send a wider signal to markets, that the BoJ is keen to undertake a broader shift toward policy normalisation.

Inflation driven by structural wage growth

Latest inflation data also supports the view favouring a hike. Japan’s inflation is no longer just a transitory phenomenon. It is increasingly underpinned by structural wage growth. Japan is experiencing a long-awaited virtuous cycle of rising wages and prices, and this current cycle is supported by a tight labour market, corporate profitability, and strong domestic demand. This is supportive of a longer term and more sustainable path for inflation.

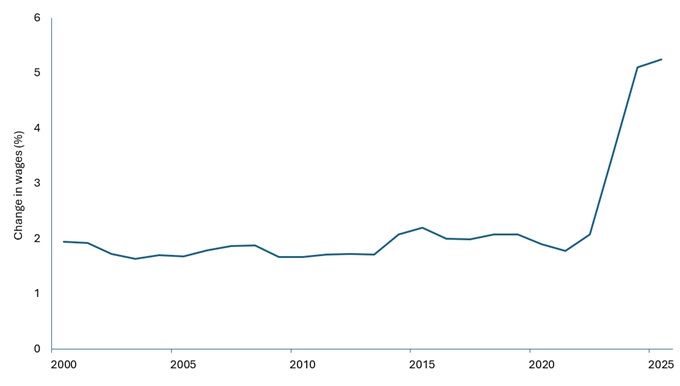

Exhibit 1 illustrates the outcomes of Japan’s annual ‘Shunto’ wage negotiations, an annual discussion held between major labour unions and employers, which highlights a growing corporate willingness to raise wages. The BoJ also uses this information to gauge whether inflation is demand driven and if hikes are justified.

Exhibit 1: Shunto wage negotiations saw a steep rise

Source: Bloomberg, Janus Henderson Investors, 2000 to 2025 Shunto wage settlements.

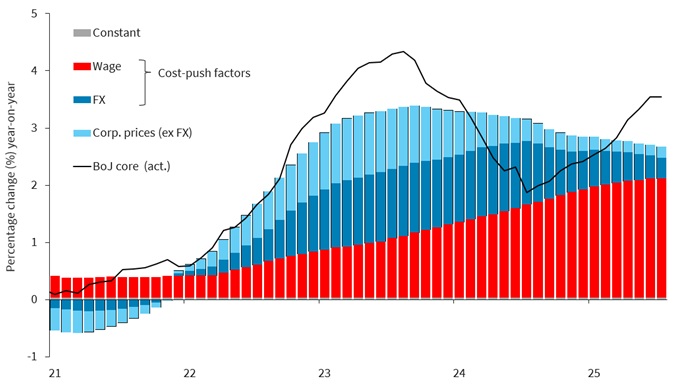

This wage-driven inflation is a departure from Japan’s deflationary past and gives the BoJ a stronger rationale to continue raising rates. With unemployment low and wage negotiations yielding meaningful increases, the central bank is under pressure to act decisively to prevent overheating.

Exhibit 2: A steady increase in wage inflation supports BoJ action

Source: MIC, BoJ, Bloomberg, Barclays Research, 1 December 2021 to 1 July 2025.

International pressure mounts

Adding to the internal momentum is external pressure, particularly from the United States. US Treasury Secretary Scott Bessent has been vocal in his criticism of the BoJ’s monetary policy stance, stating that Japan is “behind the curve” on inflation and will likely need to raise interest rates soon. In recent interviews, Bessent emphasised that Japan’s inflation challenge is both real and persistent. He argues that tighter monetary policy is essential, not only to contain price pressures, but also to support the weakening yen, which the BoJ is keen to prevent from depreciating too far.

Conclusie

We believe that Japan’s economy is approaching a point where further tightening is necessary. Since the economy has managed to improve margins through mild inflation, it is crucial for both corporate profits and the capital market that this situation is maintained through appropriate monetary policy. The risk is that delaying action could lead to a bubble and subsequent burst.

So, the pattern is clear. When two or more BoJ members dissent, it often precedes a policy shift. Combined with structural inflationary forces and international pressure, Japan appears to be entering a new phase of monetary policy – one where rate hikes are not just probable, but necessary.

From an investor perspective, Japanese financial institutions are well-positioned to benefit from any tightening in monetary policy. Banks in particular stand to gain as rising yields boost profitability by widening net interest margins (charging more on loans than they pay on deposits) and enhancing returns on their cash reserves and bond holdings.

Cost-push factors: These are conditions that affect the cost of production for goods or services, such as the increased cost of raw materials, higher wages, currency depreciation, or rising taxes.

Exchange traded fund (ETF): A security that tracks an index, sector, commodity, or pool of assets (such as an index fund). ETFs trade like an equity on a stock exchange and experience price changes as the underlying assets move up and down in price. ETFs typically have higher daily liquidity and lower fees than actively managed funds.

Inflatie: De mate waarin de prijzen van goederen en diensten in een economie stijgen. De consumentenprijsindex (CPI) en Britse index van detailhandelsprijzen (RPI) zijn twee gebruikelijke maatstaven.

Real estate investment trust (REIT): An investment vehicle that invests in real estate through direct ownership of property assets, property shares, or mortgages. As they are listed on a stock exchange, REITs are usually highly-liquid and trade like shares. Real estate securities, including REITs, may be subject to additional risks including interest-rate, management, tax, economic, environmental, and concentration risks.

Monetary policy: The policies of a central bank aimed at influencing the level of inflation and growth in an economy. Monetary policy tools include setting interest rates and controlling the supply of money. Monetary stimulus refers to a central bank increasing the supply of money and lowering borrowing costs. Monetary tightening refers to central bank activity aimed at curbing inflation and slowing down growth in the economy by raising interest rates and reducing the supply of money.

Monetary-policy normalisation: The process by which a central bank returns its policy to a more standard, neutral stance, from a previously expansionary (or unconventional) position. This typically involves moving interest rates back to their long-term average, ending asset purchase programmes, and phasing out extraordinary measures put in place to stimulate or protect an economy during a crisis.

Tight labour market: An environment where there is a scarcity of available workers and a high demand for labour. This kind of market is characterised by low unemployment, where businesses are competing for talent, generally resulting in higher wages and greater bargaining power for job seekers.

Rendement: De inkomsten uit een effect in een bepaalde periode, meestal uitgedrukt als een percentage. Een gebruikelijke maatstaf voor aandelen is het dividendrendement, waarbij de dividenduitkering per aandeel worden gedeeld door de koers van het aandeel. Voor een obligatie wordt dit berekend door de couponrente te delen door de actuele obligatiekoers.

Dit zijn de standpunten van de auteur op het moment van publicatie en kunnen verschillen van de standpunten van andere personen/teams bij Janus Henderson Investors. Verwijzingen naar individuele effecten vormen geen aanbeveling om effecten, beleggingsstrategieën of marktsectoren te kopen, verkopen of aan te houden en mogen niet als winstgevend worden beschouwd. Janus Henderson Investors, zijn gelieerde adviseur of zijn medewerkers kunnen een positie hebben in de genoemde effecten.

Resultaten uit het verleden geven geen indicatie over toekomstige rendementen. Alle performancegegevens omvatten inkomsten- en kapitaalwinsten of verliezen maar geen doorlopende kosten en andere fondsuitgaven.

De informatie in dit artikel mag niet worden beschouwd als een beleggingsadvies.

Er is geen garantie dat tendensen uit het verleden zich zullen doorzetten of dat prognoses worden gehaald.

Reclame.

Belangrijke informatie

Lees de volgende belangrijke informatie over fondsen die vermeld worden in dit artikel.

- Aandelen/deelnemingsrechten kunnen snel in waarde dalen en gaan doorgaans gepaard met hogere risico's dan obligaties of geldmarktinstrumenten. Als gevolg daarvan kan de waarde van uw belegging dalen.

- Als een Fonds een hoge blootstelling heeft aan een bepaald land of een bepaalde geografische regio, loopt het een hoger risico dan een Fonds dat meer gediversifieerd is.

- Dit Fonds kan een bijzonder geconcentreerde portefeuille hebben in vergelijking met zijn beleggingsuniversum of andere fondsen in zijn sector. Een ongunstige gebeurtenis die een impact heeft op slechts een klein aantal participaties zou tot een aanzienlijke volatiliteit of grote verliezen voor het Fonds kunnen leiden.

- Het Fonds kan gebruikmaken van derivaten om het risico te verminderen of om de portefeuille efficiënter te beheren. Dit gaat echter gepaard met andere risico's, waaronder met name het risico dat een tegenpartij bij derivaten niet in staat is om haar contractuele verplichtingen na te komen.

- Als het Fonds activa houdt in andere valuta's dan de basisvaluta van het Fonds of als u belegt in een aandelenklasse/klasse van deelnemingsrechten in een andere valuta dan die van het Fonds (tenzij afgedekt of 'hedged'), kan de waarde van uw belegging worden beïnvloed door veranderingen in de wisselkoersen.

- Wanneer het Fonds, of een afgedekte aandelenklasse/klasse van deelnemingsrechten, tracht de wisselkoersschommelingen van een valuta ten opzichte van de basisvaluta te beperken, kan de afdekkingsstrategie zelf een positieve of negatieve impact hebben op de waarde van het Fonds vanwege verschillen in de kortetermijnrentevoeten van de valuta's.

- Effecten in het Fonds kunnen moeilijk te waarderen of te verkopen zijn op het gewenste moment of tegen de gewenste prijs, vooral in extreme marktomstandigheden waarin de prijzen van activa kunnen dalen, wat het risico op beleggingsverliezen verhoogt.

- Het Fonds kan geld verliezen als een tegenpartij met wie het Fonds handelt niet bereid of in staat is om aan zijn verplichtingen te voldoen, of als gevolg van een fout in of vertraging van operationele processen of verzuim van een derde partij.