Key takeaways:

- Monetary policy has become more politicised since the global financial crisis, with central banks drawn into quasi-fiscal roles and expectations that blur institutional boundaries.

- Markets remain a partial self-correcting force, but rising government debt and political interference risk undermining policy effectiveness.

- Growing politicisation raises risks to credibility and market confidence, potentially leading to higher risk premiums and a higher cost of capital.

The ‘politicisation’ of central banks is more than just an awkward word to pronounce. It reflects a growing political pressure on central banks caused by an evolving macroeconomic and political backdrop. At a recent dinner attended by policy experts, we discussed the changes that have taken place and how this might affect fixed income markets.

Independence under pressure

Central bank governors operate under difficult conditions. Operational independence means they are expected to resist political demands and maintain discipline, even at the cost of popularity. The notion that policymakers should “remove the punchbowl” during periods of economic exuberance reflects the uncomfortable but necessary role they play. In recent years, a combination of economic crises means political scrutiny has intensified and expectations have broadened.

It is worth remembering that central bank independence has not always existed. Until 1997, the Chancellor of the Exchequer in the UK set the main policy interest rate, with the Bank of England playing an advisory role. Even in the US (seen as a bastion of independence), there were flaws: Tapes recorded in the early 1970s between Federal Reserve (Fed) Chair Arthur Burns and President Nixon revealed pressure on how the Fed might aid the economy and ultimately support President Nixon.

Rather than overtly directing policy decisions, governments increasingly shape outcomes through appointments and subtle changes to mandates. Appointing individuals perceived as more ‘agreeable’ represents a relatively straightforward route to influence, albeit one that risks undermining institutional credibility.

Soft power

Central bank mandates lie at the core of their independence, yet they also represent a channel for political intervention. Governments can either constrain central banks by limiting their powers or by expanding their responsibilities to create dependencies. Adding objectives such as supporting employment, financing programmes, or addressing inequalities may appear constructive, but can blur institutional boundaries and expose central banks to political expectation.

There is also a structural bias towards looser monetary policy. Political cycles naturally favour accommodative conditions – politicians would prefer low interest rates to stimulate an economy ahead of elections and would equally like low rates during periods of economic stress. When central banks appear to align with such preferences, markets may incorporate an implicit risk premium, reflecting doubts about their independence.

A post-crisis shift

It has become something of a cliché to blame the Global Financial Crisis for ongoing ills, but the fact is that it marked a major turning point in central banking.

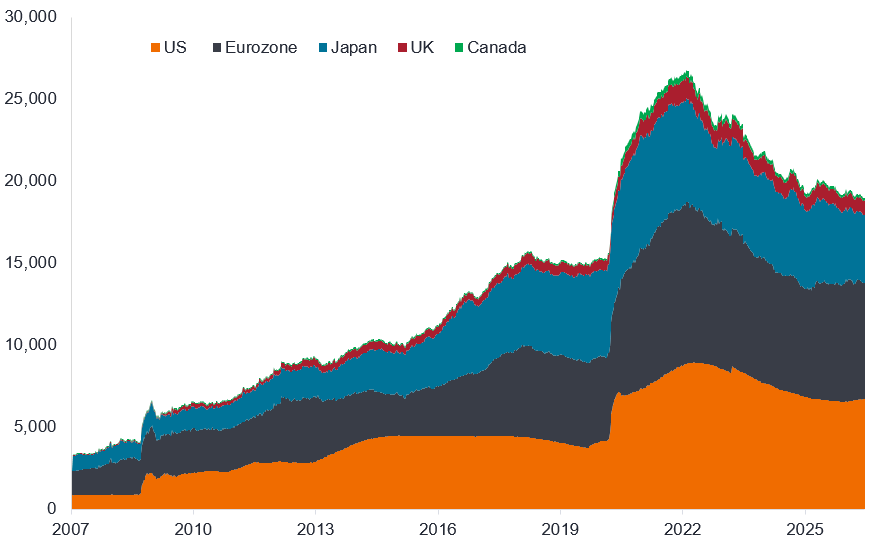

The scale and urgency of the response, notably through quantitative easing (QE) and liquidity provision, expanded the perceived capabilities of monetary policy. What began as emergency measures became, over time, standard tools. Central bank balance sheets swelled.

Central bank balance sheets (US$ billion)

Source: Bloomberg, balance sheet assets, billions in USD, weekly data, stacked area chart, US Federal Reserve, European Central Bank, Bank of Japan, Bank of England, Bank of Canada, January 2007 to June 2026.

What is more, the shift altered thinking within governments. If central banks could stabilise financial systems, support growth, and prevent deflation, then why not use these tools more broadly? In some cases, this fostered overconfidence in the ease of managing inflation and the belief that monetary policy could be aligned more closely with political priorities. Witness the growing advocacy for Modern Monetary Theory (MMT) during the COVID pandemic era, although support for MMT has since dwindled following the recent bout of inflation.

Monetary policy began to substitute for fiscal policy. Central banks were often looked on to provide stimulus, while governments avoided the more politically contentious fiscal measures (more government spending meant more borrowing or taxation). This imbalance reinforced the perception that central banks could carry a disproportionate share of economic stabilisation, further entangling them with political decision-making.

Market counterbalance

Despite these pressures, financial markets retain some degree of disciplining power. Episodes of sharp repricing, driven by concerns over fiscal sustainability or policy missteps, can quickly force a recalibration. The “mini-budget crisis” under former UK Prime Minister Liz Truss or the pushback on tariffs show how markets can seek to undo or dilute policy they see as incoherent or dislike.

In this sense, markets act as a ‘self-righting mechanism,’ albeit an imperfect one. They can signal limits to policy experimentation, although a reliance on market discipline is inherently reactive and can introduce volatility.

Sovereign borrowing costs are influenced not only by inflation and growth expectations but also by perceptions of institutional integrity. The degree of central bank independence, while difficult to quantify, forms part of the broader risk assessment applied by investors.

Is inflation targeting too narrow?

While inflation targets remain a central anchor, they have often been applied narrowly, focusing on consumer prices while overlooking broader financial metrics such as asset inflation and credit conditions. For example, much of the economic comment about inflation is devoted to energy cost inputs but we see pressure also coming from capex spending, where demand is inelastic and less price sensitive.

Monetary policy alone is a blunt tool. In crises, central banks can act quickly so it makes sense that they should be used as a first phase of response (whether lowering or raising rates or injecting liquidity) but it is better if a fiscal response then takes over (government spending or austerity). If stimulus is fiscal, and less monetary, it arguably improves the yield curve and lowers wealth inequality. Inflation targeting therefore needs to be supported by a mix of policy instruments.

Coordination in a fragmented global order

Central banks operated cohesively in an era when global policy coordination, US leadership, and multilateral institutions provided a relatively stable economic environment. While the International Monetary Fund and World Bank remain important, their authority is now being challenged by a more fragmented geopolitical landscape. States increasingly view sanctions, reserve management, and payment systems through a competitive lens.

This alters the rubric for central bank coordination. It has also undermined trust in institutions, in counterparties, the dollar system, and accessibility to global financial plumbing. This is especially relevant in reserve management where there is no simple substitute for the depth and liquidity of US treasuries.

A changing profileThe politicisation of central banks is reflected in the evolving profile of central bank leadership. There are essentially three types:

More recent central bank appointments often reflect broader considerations, including communication skills and alignment with political priorities. |

Debt levels as a constraint

The backdrop to these developments is a global economy characterised by elevated debt levels and constrained fiscal flexibility. In such an environment, monetary policy decisions carry significant distributional consequences, influencing asset prices, income inequality, and financial stability. Central banks are therefore operating in a context where their actions are inherently political.

More worryingly, the capacity to respond to future crises may be more limited than in the past. Entering a downturn with high debt levels reduces fiscal ‘wriggle room’ and increases reliance on monetary policy, reinforcing the cycle of dependence and politicisation.

Resolving the tension

It is hard to see the tension between independence and political influence being resolved. For now, we probably need to accept that an element of risk premium is built into sovereign spreads. The cost of capital, more broadly, is higher in response. Kevin Warsh, the new Fed Chair, remains something of an enigma. We expect him to quieten the influence of the Fed Board and wider messaging, which in turn places more emphasis on economic data. In such an environment, duration becomes an even more important consideration. A potential hedge to interest rate uncertainty is to consider short-dated income assets or securitised areas such as Collateralised Loan Obligations (CLOs) that have a more floating rate structure.

From a credit perspective we need to be mindful of borrowing levels but equally cognisant that companies need to take some financial risk because if they do not, they have a business risk. Chief Investment Officers can be damaged by the right decision at the wrong time, i.e. being too conservative too early and allowing other companies to take market share. There is a lot of energy in the markets right now around artificial intelligence (AI) but we think investors should be selective, looking beyond some of the hyperscalers towards areas that potentially offer better risk-adjusted value or are involved in areas that are helping to relieve bottlenecks in the AI build-out.

Regardless of the degree of central bank independence, there will ultimately come a time when the central bank needs to remove the proverbial punchbowl and investors want to be on the right side of that when it comes.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Balance sheet: Typically an accounting reference relating to assets versus liabilities for an entity, whether a household or a corporation.

Capex: Money a business spends on major, long-term assets such as property and equipment (tangible assets) or technology, software, trademarks, patents etc (intangible assets) to facilitate new projects or investments that support business growth and expansion

Collateral: In a securitisation, collateral refers to the pool of financial assets that are bundled together to form the basis of a security.

Collateralized Loan Obligations (CLOs): Debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Deflation: A decrease in the price of goods and services across the economy, usually indicating that the economy is weakening. It differs from ‘disinflation’, which implies a decrease in the level of inflation. Deflation is the opposite of inflation.

Duration: Measures the sensitivity of a bond’s or fixed income portfolio’s price to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Federal Reserve (Fed): The central bank of the US which determines its monetary policy.

Fiscal policy: Describes government policy relating to setting tax rates and spending levels. Fiscal discipline is where governments do not borrow excessively, i.e. keeping borrowing as a percentage of the output of the economy low so that the overall debt burden does not expand aggressively.

Hedge: A trading strategy that involves taking an offsetting position to another investment that will lose value as the primary investment gains and vice versa. These positions are used to reduce or manage various risk factors and limit the probability of overall loss in a portfolio.

Hyperscaler: Technology providers that provide IT architectures that scale dynamically to handle exponential increases in workload and data. Apart from capacity, they offer enterprise-grade cloud services, flexible hardware resources, and robust software environments that support a broad range of AI applications.

Inflation: The rate at which prices of goods and services are rising in the economy.

Issuance: The act of making bonds available to investors by the borrowing (issuing) company, typically through a sale of bonds to the public or financial institutions.

Maturity: The maturity date of a bond is the date when the principal investment (and any final coupon) is paid to investors. Shorter-dated bonds generally mature within 5 years, medium-term bonds within 5 to 10 years, and longer-dated bonds after 10+ years.

Mini-Budget crisis: The UK government in 2022 unveiled a sweeping economic plan, dubbed the “mini-budget” that included billions in unfunded tax cuts that rocked financial markets and ultimately led to a series of embarrassing U-turns and a loss of confidence in the new prime minister Liz Truss and the collapse of her administration.

Modern Monetary Theory: A macroeconomic framework that posits that sovereign nations which issue their own currency are not financially constrained in the way households are. It argues that governments can never default on their debt because they can always print money to pay it off. The central bank’s role is to accommodate the government’s fiscal needs.

Monetary policy: The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. Monetary policy tools include setting interest rates and controlling the supply of money.

Quantitative Easing (QE): An unconventional monetary policy used by central banks to stimulate the economy by boosting the amount of overall money in the banking system

Securitisation: The process in which certain types of assets are pooled so that they can be repackaged into interest-bearing securities. The interest and principal payments from the assets are passed through to the purchasers of the securities.

Sovereign bond/government bond: Bonds issued by governments to pay off debt or finance spending. They are typically backed by a country’s capacity to levy taxes on its citizens and/or capacity to print money.

Volatility: Measures risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.