Subscribe

Sign up for timely perspectives delivered to your inbox.

Portfolio Managers John Kerschner, Nick Childs, and Jessica Shill discuss how investors can take advantage of higher short-term yields while still managing duration exposure.

While it is true that bonds can provide returns from either yield or price movements, yield (or income) has historically been the primary source of return and, therefore, the element to which we think investors should pay the most attention.

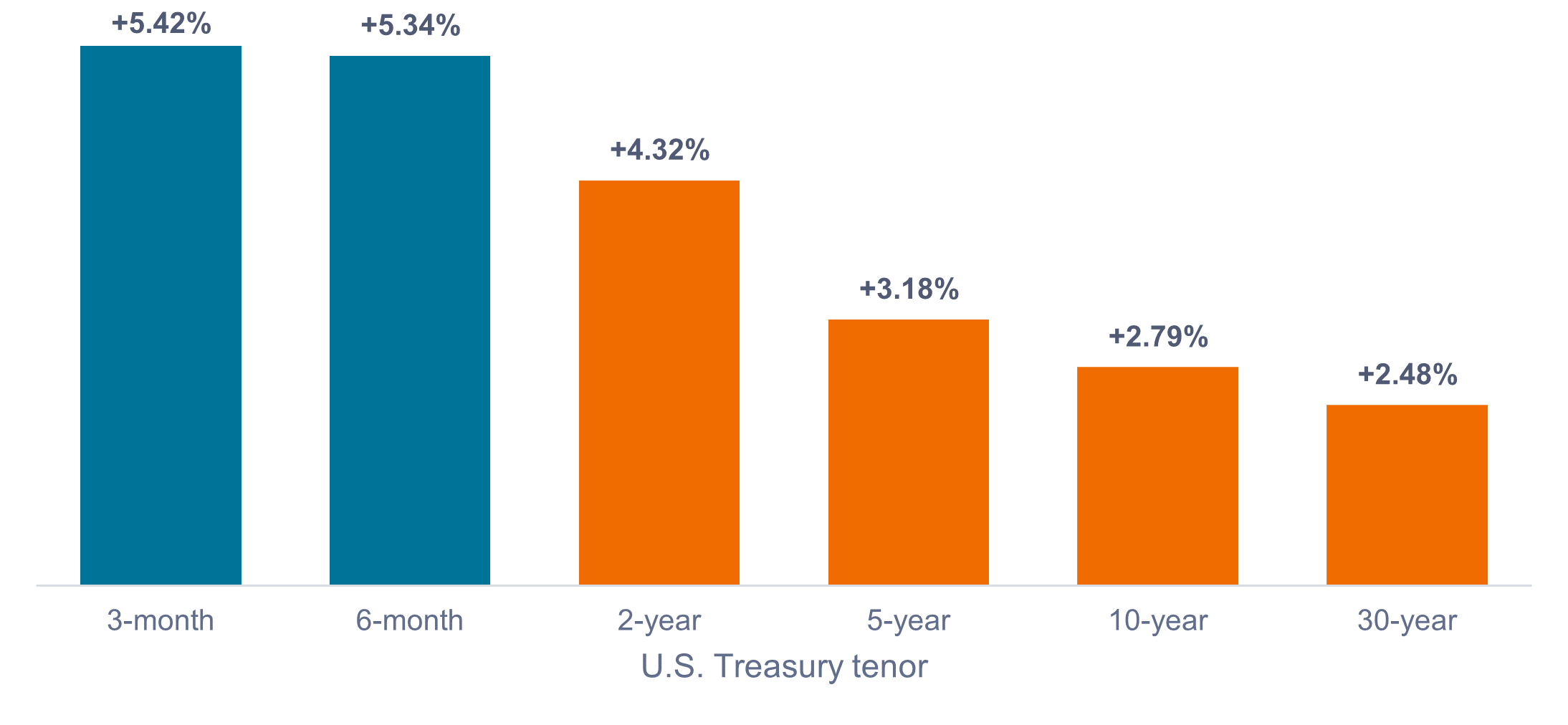

Yield changes on the 10-year U.S. Treasury have garnered much attention recently, but the bigger story is the change at the short end of the yield curve. As shown in Exhibit 1, since the beginning of 2022 when rates began to move in response to high inflation and a hawkish Federal Reserve (Fed), short-term rates have risen far more than intermediate and long-term rates.

Short-term rates have moved up far more than intermediate and long-term rates in this tightening cycle.

Source: Bloomberg, as of 18 September 2023.

Source: Bloomberg, as of 18 September 2023.

Note: Bars represent the change in the yield to maturity on U.S. Treasury bonds by tenor from 1 January 2022 to 18 September 2023.

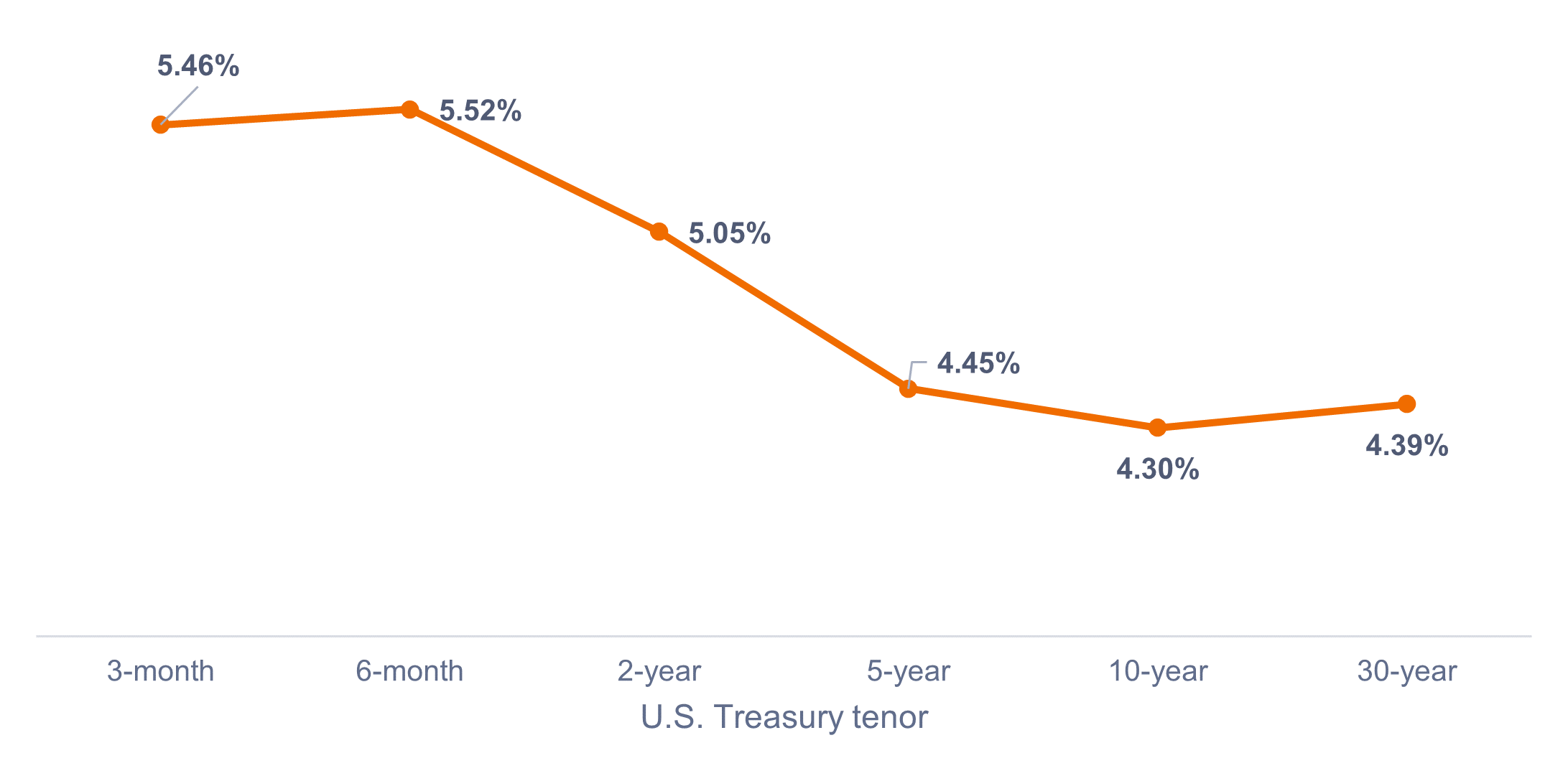

Due to disproportionate changes along the yield curve, the yield to maturity on short-term Treasuries is higher than on longer-dated Treasuries, resulting in an inverted yield curve. Bond investors now have a unique opportunity to earn higher yields while taking less duration (or interest-rate) risk, as shown in Exhibit 2.

It is important for investors to grasp how rare inverted yield curves are: In the 31 years since 1992, the yield on the 2-year U.S. Treasury has been above the yield on the 10-year Treasury for less than 9% of all trading days.

Inverted yield curve means higher yields are available with less interest-rate risk.

Source: Bloomberg, as of 18 September 2023.

Source: Bloomberg, as of 18 September 2023.

Note: Chart shows current yield to maturity for U.S. Treasuries by tenor.

As investors contemplate the attractive yields in short-duration assets, the next question becomes how best to gain exposure in the space. Typically, investors have turned to corporate credit, but we think there is a better alternative.

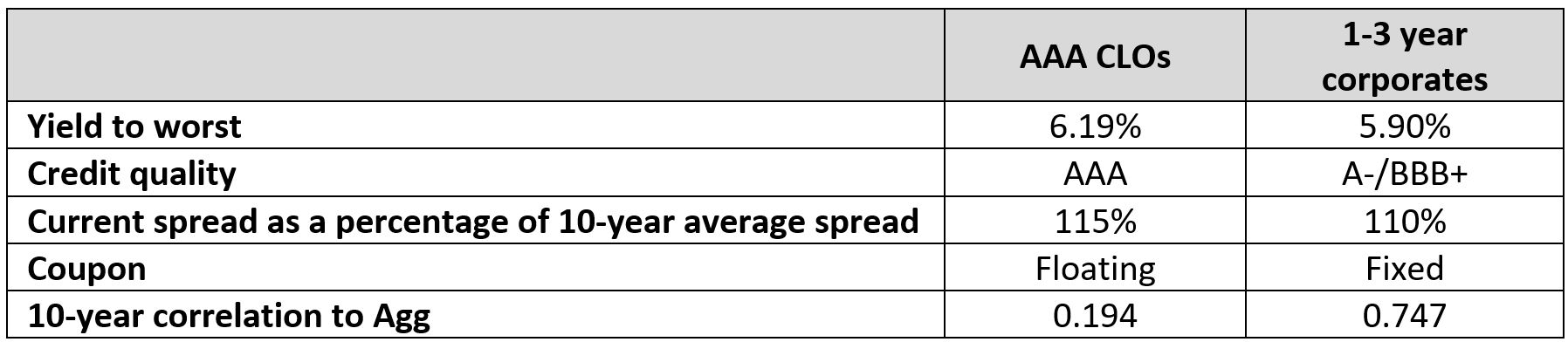

In our view, AAA rated collateralized loan obligations (CLOs) offer a compelling option for investors seeking short-duration exposure. As shown in Exhibit 3, the reasons for this are fivefold: Compared to corporate credit, AAA CLOs currently offer better yields, with higher credit quality, at more compelling valuations, with the diversification benefits of floating-rate coupons, and low correlation to the Barclays U.S. Aggregate Bond Index (Agg).

Source: Bloomberg, J.P. Morgan, Janus Henderson Investors, as of 18 September 2023. Indices used to represent asset classes: AAA CLOs (J.P. Morgan AAA CLO Index), 1-3 Year Corporates (Bloomberg U.S. Corporate 1-3 Year Index).

Source: Bloomberg, J.P. Morgan, Janus Henderson Investors, as of 18 September 2023. Indices used to represent asset classes: AAA CLOs (J.P. Morgan AAA CLO Index), 1-3 Year Corporates (Bloomberg U.S. Corporate 1-3 Year Index).

While investors can appreciate the yields on the short end of the curve, some are concerned about missing out on a rally in long-term rates. Their logic? Inflation is trending down from its 2022 peak; the Fed is close to pausing and may start cutting rates in 2024. We don’t want to be short duration once rates begin to fall – it would be better to be long duration to pick up the price appreciation.1

While there is certainly some justification to this argument, we think investors need to consider a couple of important points.

First, we believe investors should avoid trying to predict where yields will be in the future. Instead, they should focus on where the yield is right now, bearing in mind that starting yield has historically been the most significant contributor to total returns in fixed income.

Second, while it is true that inflation is coming down and we are nearing the end of the rate-hiking cycle, the Fed has not officially stopped raising rates. And with the recent uptick in energy prices and ongoing sticky shelter inflation, it seems likely that the move from 4% to 2% in core inflation will be slower and more difficult than the move from 6% to 4% was. As such, we see the central bank keeping rates higher for longer – another tailwind for floating-rate bonds.

While we think it’s unlikely that rates will fall materially anytime soon, the chances of it happening are not zero. The scenario in which this may occur is if the economy enters a recession, and if that happens, longer-duration bonds are likely to outperform.

Investors who do not want to be caught with too little duration in that scenario may consider a barbell strategy by pairing their AAA CLO allocation with longer-duration assets, such as Treasuries, mortgage-backed securities (MBS), or corporate bonds.

We think pairing AAA CLOs with corporate bonds for a recession scenario would be suboptimal for many of the same reasons we listed for short-duration corporates, as shown in Exhibit 4. Furthermore, if the economy does enter a recession, corporate credit spreads are likely to widen from current levels, because, in our view, they are not adequately pricing in the chances of an economic slowdown.

That leaves the option of pairing AAA CLOs with Treasuries or MBS. While Treasuries would be a viable option, MBS has the added benefit of a pickup in yield and the possibility of outperformance from spread tightening.

Source: Bloomberg, Janus Henderson Investors, as of 18 September 2023. Indices used to represent asset classes: MBS (Bloomberg U.S. Mortgage-Backed Securities Index), Corporates (Bloomberg U.S. Corporate Bond Index), U.S. Treasuries (Bloomberg U.S. Treasuries Index).

Source: Bloomberg, Janus Henderson Investors, as of 18 September 2023. Indices used to represent asset classes: MBS (Bloomberg U.S. Mortgage-Backed Securities Index), Corporates (Bloomberg U.S. Corporate Bond Index), U.S. Treasuries (Bloomberg U.S. Treasuries Index).

Our premise for using MBS to add duration is based on two post-COVID developments in the MBS market.

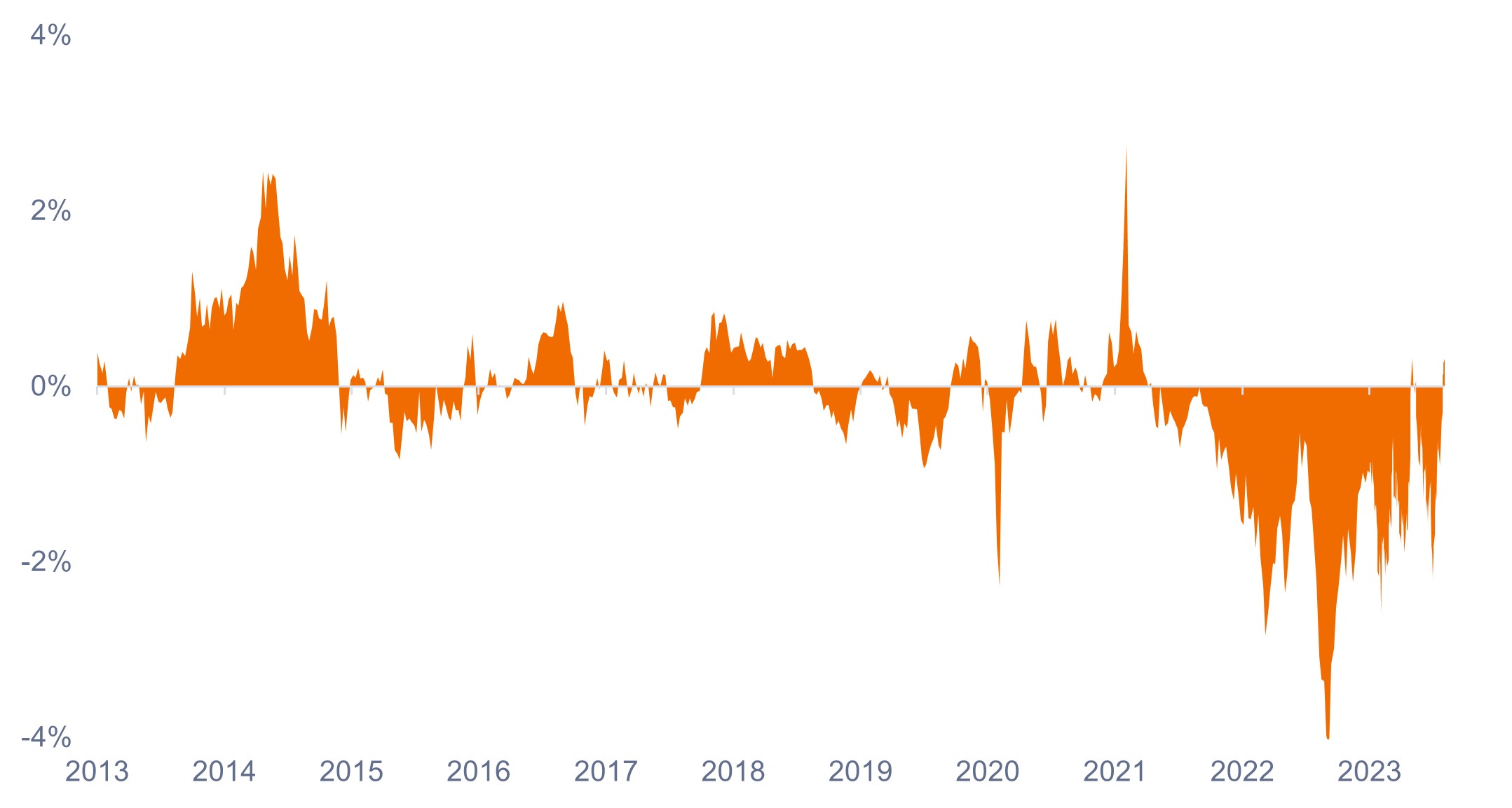

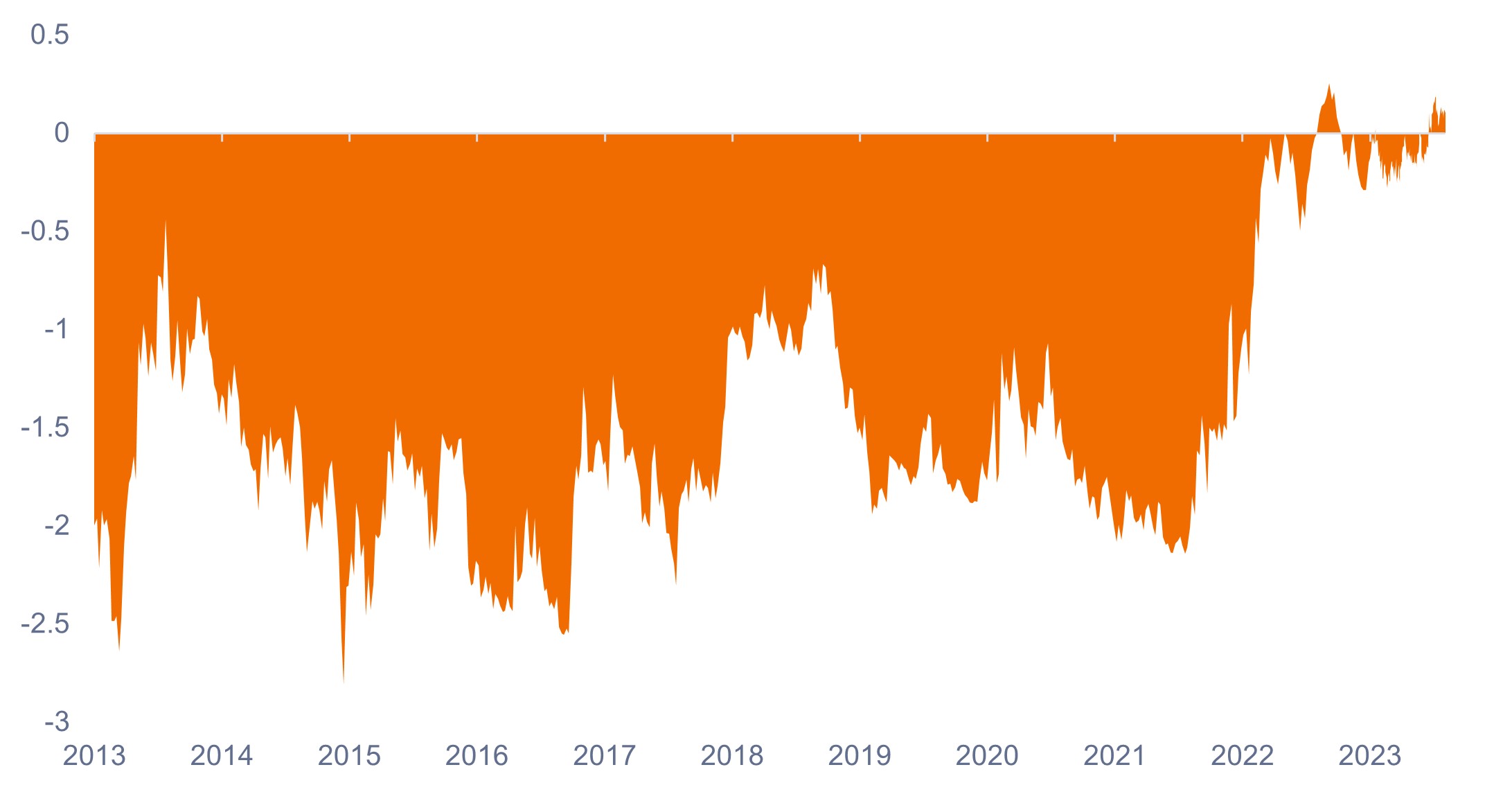

First, MBS have underperformed Treasuries since late 2021, as shown in Exhibit 5. However, many of the reasons for their relative underperformance, such as high interest-rate volatility and supply concerns as the Fed reduces the size of its balance sheet, have begun to unwind. While not as cheap as they were in the fall of 2022, we think MBS still have the potential to outperform Treasuries as priced-in risks continue to dissipate.

Since late 2021, MBS have underperformed Treasuries, but we believe they’re poised to outperform from here.

Source: Bloomberg, as of 18 September 2023.

Source: Bloomberg, as of 18 September 2023.

The second development is that negative convexity risk in MBS – which has historically dissuaded investors from using MBS as an instrument to add duration to portfolios1 – has dropped to all-time lows, as shown in Exhibit 6.

Negative convexity is simply a measure of the cash flow variability of mortgages. Due to the record number of home purchases and refinances at extremely low rates in 2020 and 2021, more than 90% of existing mortgages were originated at rates of 4% or lower. With the current mortgage rate above 7%, most mortgage holders have no incentive to refinance. The result is that mortgage cash flows are more certain than they’ve historically been and, therefore, we believe now is a good time to consider using MBS as a duration lever.

Refinancing risk is lower than ever, resulting in a more stable duration profile for MBS.

Source: Bloomberg, as of 18 September 18 2023.

Source: Bloomberg, as of 18 September 18 2023.

Since 2008, fixed income investors have been lamenting low yields under the Fed’s zero interest-rate policy. Now, rates have finally risen to the extent that bonds are generating better income, particularly on the short end of the yield curve. We think AAA rated CLOs present a compelling option for investors seeking to access the yields on offer. And by pairing AAA CLOs with Treasuries or MBS, investors can continue to harvest yields in short duration, while still fine-tuning their desired duration exposure.

1 When interest rates fall, prices of long-term bonds typically rise more than prices of short-term bonds.

2 When rates fall, duration on MBS typically falls too, because homeowners are incentivized to refinance their mortgages at lower rates. Bond investors thereby receive earlier payback, which reduces the duration of their investment, and they end up not fully benefitting from falling rates.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

A yield curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

10-Year Treasury Yield is the interest rate on U.S. Treasury bonds that will mature 10 years from the date of purchase.

An inverted yield curve occurs when short-term yields are higher than long-term yields.

Yield to worst (YTW) is the lowest yield a bond can achieve provided the issuer does not default and accounts for any applicable call feature (ie, the issuer can call the bond back at a date specified in advance). At a portfolio level, this statistic represents the weighted average YTW for all the underlying issues.

IMPORTANT INFORMATION

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Mortgage-backed securities (MBS) may be more sensitive to interest rate changes. They are subject to extension risk, where borrowers extend the duration of their mortgages as interest rates rise, and prepayment risk, where borrowers pay off their mortgages earlier as interest rates fall. These risks may reduce returns.

Sign up for timely perspectives delivered to your inbox.