Key takeaways:

- Japan’s AI ecosystem extends well beyond chipmakers, with significant exposure across the semiconductor value chain, including equipment, components, materials, packaging, and data-centre infrastructure.

- Unlike many developed markets, rising rates in Japan are improving profitability for banks and insurers through wider margins and stronger investment income.

- Strong earnings growth is helping support valuations, which remain reasonable currently, with the market trading at around 17x earnings.

Continuing the trend since 2023, foreign investors have returned to the Japanese equities market, with net flows of almost JPY 10 trillion (US$60 billion) in the first half of 2026, reaching an all-time high. 1 Importantly, in recognition of the increasingly attractive long-term investment case for the asset class, the majority of these flows has shifted from futures-driven strategies to long-only cash equities.

The renewed interest in the market has been a major tailwind. In the first half of 2026, the Nikkei 225 Index gained 38% and the TOPIX rose 19% in yen total return terms. In US dollar terms this translates into gains of 33% and 14% respectively, while in comparison, the S&P 500 increased by 10% and the Nasdaq Composite 13%. 2 The macroeconomic backdrop has not been particularly favourable for equities, as costs have been impacted by significantly higher energy prices due to the US-Iran conflict, and interest rates have also increased, with the 10-year Japanese government bond yield up from under 2% at the start of the year to a 30-year high of 2.9% recently 3 (bond yields move inversely with bond prices). So, what exactly is happening? The major drivers of this rally are semiconductor-related stocks and financials.

AI is driving opportunities across Japan’s semiconductor ecosystem

While investor attention has primarily focused on US semiconductor companies as a big winner of the AI revolution, the strong share price gains we have seen for Japanese semis in the last two years are reflecting the broadening out of the beneficiaries of huge global AI capex (capital expenditure) spending. In fact, Japanese semiconductor stocks have been the main driver of the Nikkei’s recent record highs.

Investors who are concerned with concentration risk in a single sub-sector should take note of a key feature of the Japanese market – its broad industrial base. Beyond large semiconductor equipment and chip manufacturers, suppliers of parts, component manufacturers, and materials companies form a very wide AI ecosystem. Upstream, there is SoftBank Group, one of the major investors in OpenAI and semiconductor design company ARM Corp. In addition, companies such as Kioxia (semi foundry specialising in NAND flash memory) and Tokyo Electron (semi manufacturing equipment) have world-leading market shares.

However, it does not stop there. The broad semiconductor supply chain includes Ebara and Horiba, which supply components for chip manufacturing equipment. Silicon wafers are dominated by Shin-Etsu Chemical and SUMCO, which together account for roughly two-thirds of global market share. 4 Photoresists (light-sensitive liquid plastic that acts as a protective shield allowing engineers to carve extremely tiny, complex patterns like microchips or circuit boards) are effectively dominated by Japanese manufacturers such as Tokyo Ohka Kogyo.

In other related areas, Japanese companies are also leaders in semiconductor packaging materials such as IBIDEN. Similarly, there are many beneficiaries of the significant investments in data centres, with Fujikura and Furukawa Electric, manufacturers of a broad range of transmission equipment. More recently, of recognition that supplying stable voltage at high levels to ensure data integrity and prevent hardware failure with increasingly heavy computing loads has driven up Murata Manufacturing’s market cap, the top MLCC manufacturer, from almost US$40 billion in January, to more than US$100 billion at the end of June 2026. 5

But this success has been a long time coming. Up until the 1990s, Japanese semiconductor manufacturers were dominant in terms of global market share. However, with technological progress in line with Moore’s Law, the required scale of investment increased rapidly. At that time, industry consolidation should have progressed to enhance investment capacity, but Japan’s characteristic preference for in-house development prevented this, and as a result, companies fell behind in the investment race. Taiwan’s TSMC and South Korea’s Samsung Electronics emerged as winners, and among pure-play semiconductor manufacturers, Kioxia is the only global leader from Japan. Kioxia itself originated from the restructuring of a company that had lost its competitiveness. The largest company in Japan by market cap (more than US$300 billion at end June 2026), it was only worth circa US$8 billion 12 months ago. 6

Turning to semiconductor equipment, components, and materials, competition was focused not on investment scale but on technological innovation. As a result, the dynamism of the industry was maintained, leading to its current competitiveness. Factoring in the significant expansion of AI-related investment and the accompanying multi-year technology roadmap, we believe the positive impact on earnings is only just beginning. Moreover, many of Japan’s semiconductor-related companies provide differentiated and unique equipment and materials – in periods of tight supply and demand, the potential to benefit from price hikes increases. In our view, these combined factors may not yet be fully reflected in stock prices.

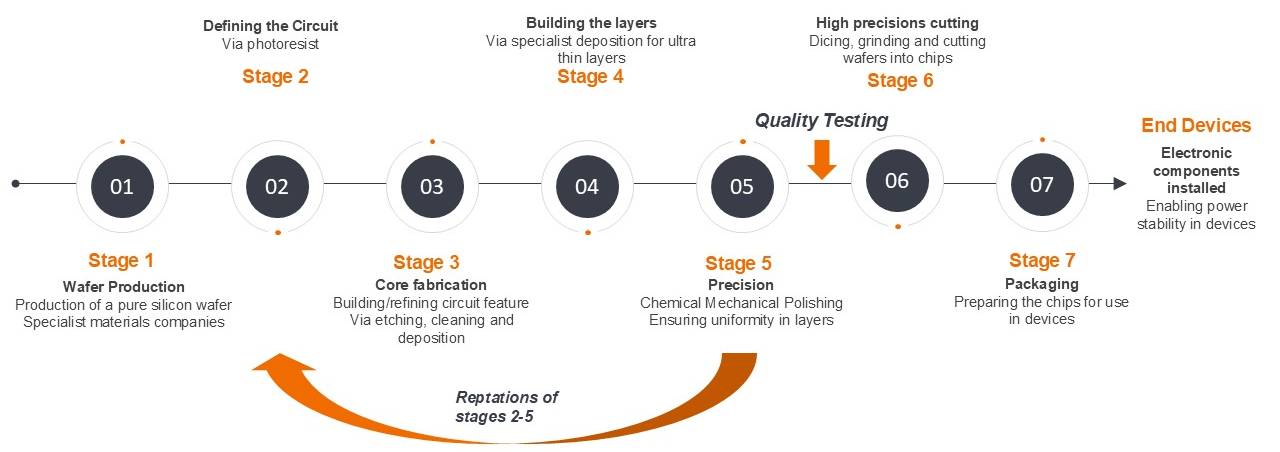

Japan offers diversified AI exposure across the semiconductor value chain

Source: Janus Henderson Investors. For illustrative purposes only.

Rate hikes will support Japanese financials

Financials are a significant component of the Japanese market and are benefiting from structural rather than cyclical drivers. Unlike other developed markets, where higher inflation and interest rates have weighed on valuations, Japan’s shift from decades of low inflation is supporting Japanese financials’ earnings growth through wider lending spreads (difference between the interest rate charged on loans and what the lender pays on deposits), stronger loan demand, and improved investment income for insurers. Globally, concerns over a resurgence of inflation have led to expectations of higher interest rates, which have capped the upside for financials in other developed markets. However, following almost three decades of deflation in Japan, inflation is gradually becoming entrenched, with its economy in a process of interest rate normalisation following years of negative interest rates. The central bank has been gradually raising its interest rate since March 2024, which benefits financial institutions and banks in particular as they can now improve their net interest margin, leading to higher profitability and earnings growth.

Another supporting factor is rising inflation expectations, which is prompting the front-loading of capital expenditure for businesses and consumer spending, which typically leads to an expansion in loan demand.

Also notable is that insurers’ main profit source is now shifting from underwriting to investments. At least over the next few years, we believe rising interest rates will act as a tailwind for earnings improvement, and ultimately, for Japanese equities.

Attractive valuations add to the compelling case for Japanese equities

From a valuation perspective, the Japanese market currently trades on a reasonable price-to-earnings (P/E) ratio of around 17x at the time of writing, 7 with roughly half of the market’s gains attributable to earnings improvement.

As earnings remain resilient and valuations reasonable, Japanese equities look well positioned to continue to attract investors seeking exposure to structural growth themes such as AI, with rising capital expenditure and personal consumption, but without paying excessive valuation multiples like other developed markets. As foreign investor demand shifts from broad market exposure toward company-specific opportunities, in our view the potential for active managers to generate alpha from stock picking is likely to increase, particularly beyond the obvious AI beneficiaries such as specialist semi value chain suppliers and market leaders with pricing power.

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

TOPIX is a free-float adjusted market capitalization-weighted index and is used as a benchmark for investment in Japanese stocks.

Nikkei 225 is the leading index of Japan’s top 225 companies traded on the Tokyo Stock Exchange.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

Nasdaq Composite® Index tracks all 3,000+ stocks listed on the Nasdaq Stock Market® making it one of the broadest measures of U.S. equity performance.

1 NHK World Japan: Net buying by foreign investors hit market record in 2026; 3 July 2027.

2 Refinitiv Datastream as at 30 June 2026. Past performance does not predict future results.

3 Bloomberg, JGB 10-year yield as at 9 July 2026. Yields may vary and are not guaranteed.

4 OECD, Mapping the Semiconductor Value Chain, June 2025.

5 Companiesmarketcap.com accessed on 8 July 2026.

6 Deutsche Bank Research Institute, July 2026.

7 Japan Exchange Group, MacroMicro as at 10 July 2026.

Alpha: The excess return generated by an investment relative to its benchmark index. Alpha is often used as a measure of an active manager’s skill.

Bond yield: The level of income on a security expressed as a percentage rate. For a bond, this is calculated as the coupon payment divided by the current bond price. There is an inverse relationship between bond yields and bond prices. Lower bond yields mean higher bond prices, and vice versa.

Capital expenditure (Capex): Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment, vehicles or technology in order to maintain or improve operations and foster future growth.

Cash equities: The direct purchase or sale of shares in listed companies, as opposed to derivatives such as futures contracts.

Deflation: A sustained decrease in the general price level of goods and services.

Futures-driven strategies: These strategies like managed futures or CTAs use derivatives to go both long and short across diverse asset classes, actively profiting from price trends and market volatility.

Interest rate normalisation: The process of moving interest rates from unusually low or accommodative levels toward more historically typical levels.

Long-only cash equities: Buying and holding stocks in the expectation that their value will rise over time.

MLCC (Multi-Layer Ceramic Capacitor): A small electronic component used to store and regulate electricity in electronic devices. MLCCs are essential in smartphones, vehicles, data centres, and AI infrastructure.

Moore’s Law: Coined in 1965 by Intel co-founder Gordon E. Moore, it is the principle that the number of transistors that can fit onto a microchip will double every two years, enabling technology to become smaller, faster, and cheaper over time.

NAND flash memory: A type of non-volatile storage technology that can retain data without a power source, usually found in devices like USB flash drives, memory cards and solid-state drives.

Net-interest margin: An indicator of a bank’s profitability. It compares the amount of money the bank is earning in interest on loans and other interest-bearing securities relative to interest paid towards sourcing its own funding (such as interest on bank accounts).

Photoresists: Light-sensitive polymers utilized in photolithography to create intricate patterns on substrates, such as silicon wafers for microchips or copper boards for PCBs. They act as a temporary protective stencil, allowing manufacturers to selectively etch, deposit, or implant materials during device fabrication.

Price-to-earnings ratio (P/E Ratio): A popular ratio used to value a company’s shares compared to other stocks or a benchmark index. It is calculated by dividing the current share price by its earnings per share.

Re-rating: A change in the valuation investors are willing to assign to a company or market, often due to improving growth prospects, profitability, or sentiment.

Valuation multiple: By dividing one financial metrics by another, investors can assess if a company is relatively underpriced or overpriced in its industry. Understanding different types of multiples, such as price-to-earnings (P/E) and EV-to-EBITDA, helps investors make informed comparisons and investment decisions.