Key takeaways:

- Geopolitical uncertainty is unsettling in the short run but rarely changes the fundamental investment picture. We believe volatility is an opportunity to add to high-quality positions, and the opportunity cost of becoming too defensive is often underappreciated over the long run.

- Earnings growth is broadening beyond AI infrastructure into sectors like biotech, digital payments, and financial services. Combined with tax reform and deregulation, we see the macro backdrop as still constructive despite near-term geopolitical and inflation headwinds.

- Artificial intelligence (AI) adoption is creating real winners, but also real disruption risk. We believe the market is not yet fully differentiating between software companies that will adapt and those that won’t; that gap is where compelling active management opportunities exist, in our view.

Q: Geopolitical events like the war in Iran can move markets quickly. How do you approach investing through that kind of uncertainty?

Michael Keough: Geopolitical events can carry real tail risks that are hard to model, but the key question is what will the sustained economic impact actually be? Often, it’s more limited than the initial reaction suggests.

Our current read is that this appears to be a shorter-duration campaign focused on specific military infrastructure rather than broader energy systems. If the Strait of Hormuz reopens in the near future and energy infrastructure is not significantly disrupted, we expect the oil price spike is likely to be temporary but potentially lasting the first half of the year. We are also mindful that the administration must balance their objectives for this campaign with the upcoming midterm elections.

It also helps to consider where we started. Oil had been at fairly low levels, around $50 to $60 a barrel, and the world was already oversupplied by roughly 2 million barrels a day heading into this. Iran produces about 3 million barrels a day, and we do not expect a sustained removal of that supply.

More broadly, our approach during periods like this is to lean into quality and use volatility as an opportunity. In our asset allocation portfolios, we came into 2026 with a meaningful overweight to equities based on our view that earnings growth would remain positive. We didn’t anticipate this level of geopolitical disruption, but we don’t see it materially changing the fundamental picture for the year, which is supported by a number of tailwinds. If markets continue to sell off, our bias is to add to equities selectively.

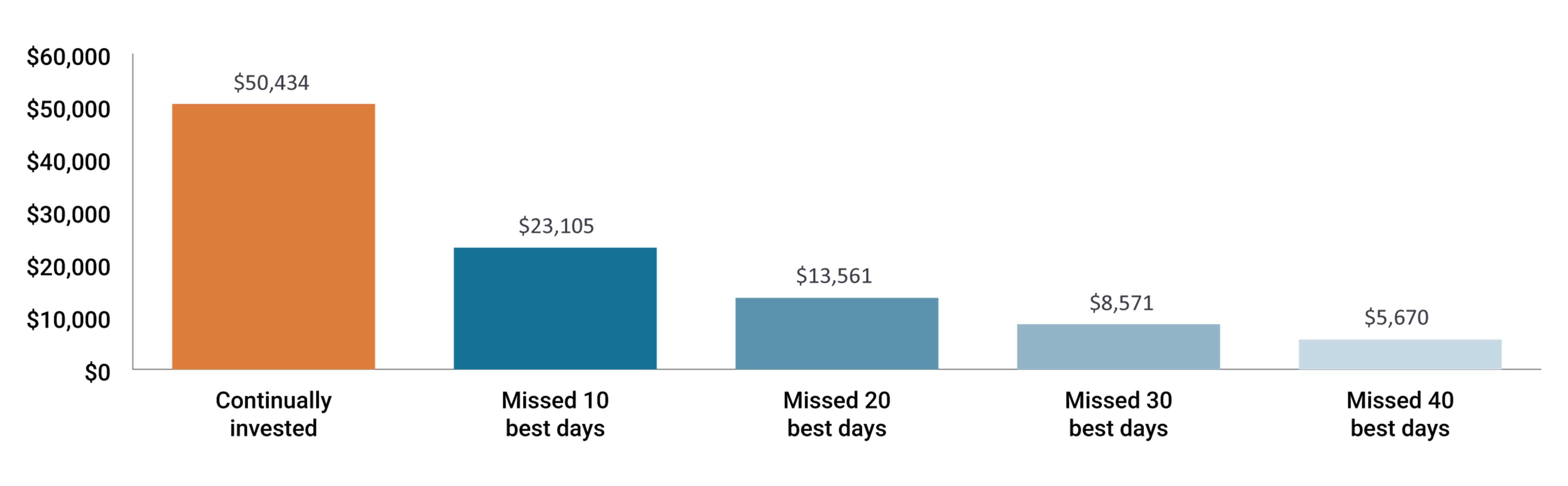

It’s worth noting the opportunity cost of becoming too defensive. Over the last couple of years, being too conservative, such as holding too much cash or underweighting equities, meant missing the recoveries that drove the bulk of returns. Historically, a handful of strong market days have contributed an outsized share of long-term equity returns, and investors need to be positioned to capture them.

Exhibit 1: Value of a hypothetical $10,000 investment in the S&P 500® Index from 1999 – 2024.

Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Source: FastSet Research Systems, Inc. from 1 January /1999 to 31 December 2024. The example is hypothetical and used for illustration purposes only. It does not represent the returns of any particular investment.

Q: You mentioned the fundamental picture remains intact. What gives you confidence, and where are you seeing the opportunity?

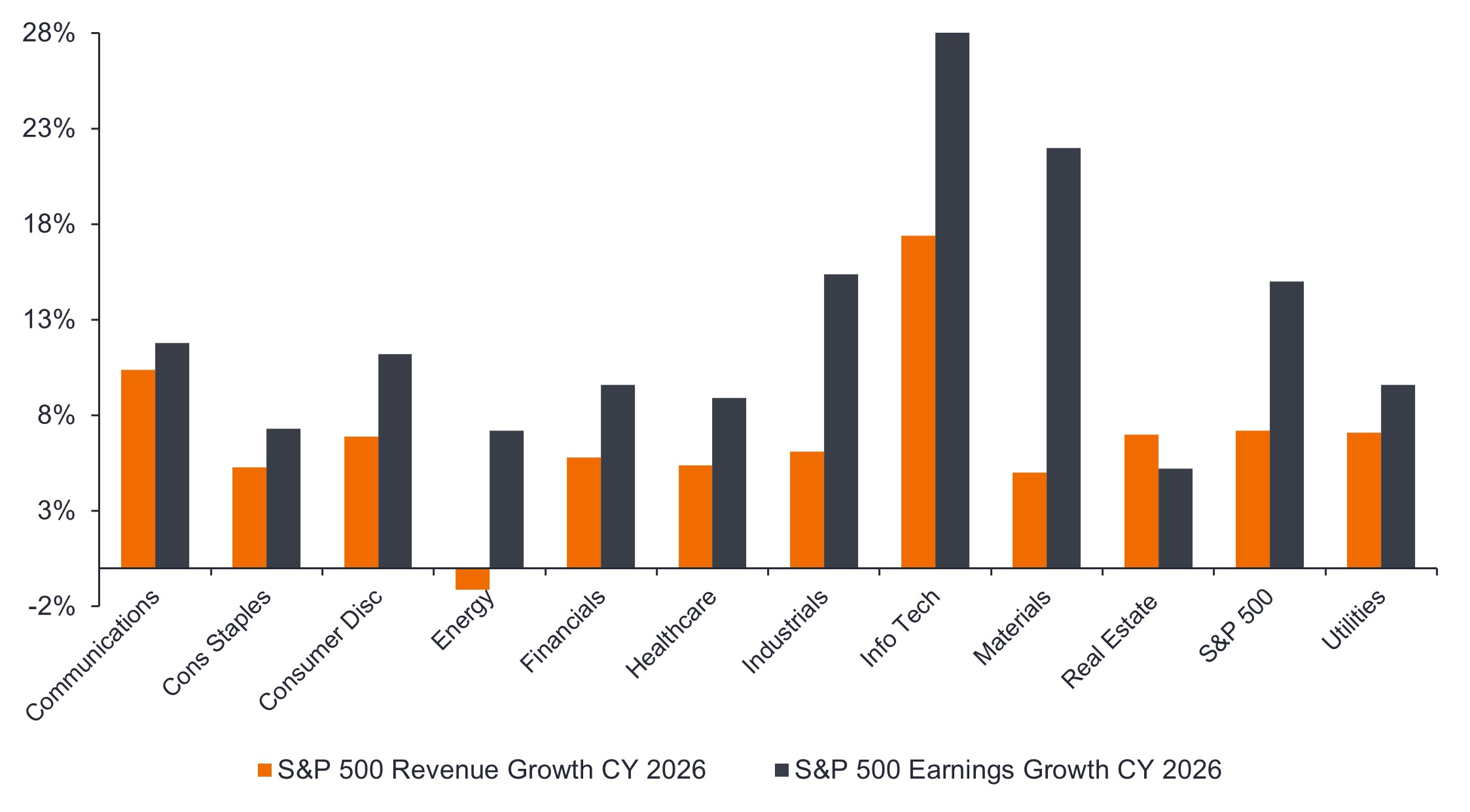

Jeremiah Buckley: The earnings story has broadened considerably, and that’s central to our constructive view. AI infrastructure and large internet platforms have been growing strongly, but they are no longer carrying the market alone. Other sectors have started contributing meaningfully, including biotech, healthcare equipment, digital payments, and financial services. Innovation in these areas is translating into earnings. Technology-related capital expenditures are contributing roughly a third of GDP growth in 2026, and the benefits are flowing well beyond the infrastructure build itself.

Exhibit 2: Strong revenue and earnings growth is expected broadly across sectors for 2026

Source: Bloomberg, as of January 2026. CY=calendar year.

There are also tailwinds that tend to get overshadowed by headlines from geopolitical events. Tax reform, deregulation, and the early productivity gains from technology investment are all constructive for corporate earnings and haven’t gone away.

We can also be active in how we are positioning through near-term volatility. In 2025, we used periods when cyclical sectors were being indiscriminately sold off to rotate into more cyclical exposure. We think a similar dynamic may be developing now, and we’ll be looking for opportunities to act on it.

Q: There’s been a lot of debate about whether inflation can get back to 2% or whether 3% is the new normal. What is your view?

Keough: We think getting back to 2% is going to be difficult to sustain. Structural pressures remain, including supply constraints, a modest degree of deglobalization, higher energy prices, and slower population weighing on labor. AI could help offset that last point, but probably not enough on its own unless productivity gains substantially exceed current expectations.

That said, some of the forces that held inflation elevated are fading. Tariff-related goods inflation is being lapped, year-over-year comparisons are getting easier, and some tariffs have since been reduced by court rulings. Those headwinds are becoming less of a factor as the year progresses.

Our base case is around 2.5%, with long-term inflation expectations closer to 2%, and we’d argue that’s a reasonably healthy environment for equities. It gives companies a bit of pricing power without forcing the Federal Reserve to tighten. Given the other tailwinds supporting earnings growth, it fits into what we still see as a constructive backdrop.

Q: As AI is adopted more broadly, risks to certain parts of the market are becoming clearer. How are you thinking about those risks, and what does it mean for software?

Buckley: Having watched many technology cycles, we do think there is some degree of overhype embedded in this one, and we’re watching returns on invested capital closely across the infrastructure build. Spending will plateau at some point, and the market will need to digest it. The early evidence on returns is encouraging. Meta’s advertising revenue growth is perhaps the clearest example of AI investment generating real, measurable results, but that is one data point in an evolving story.

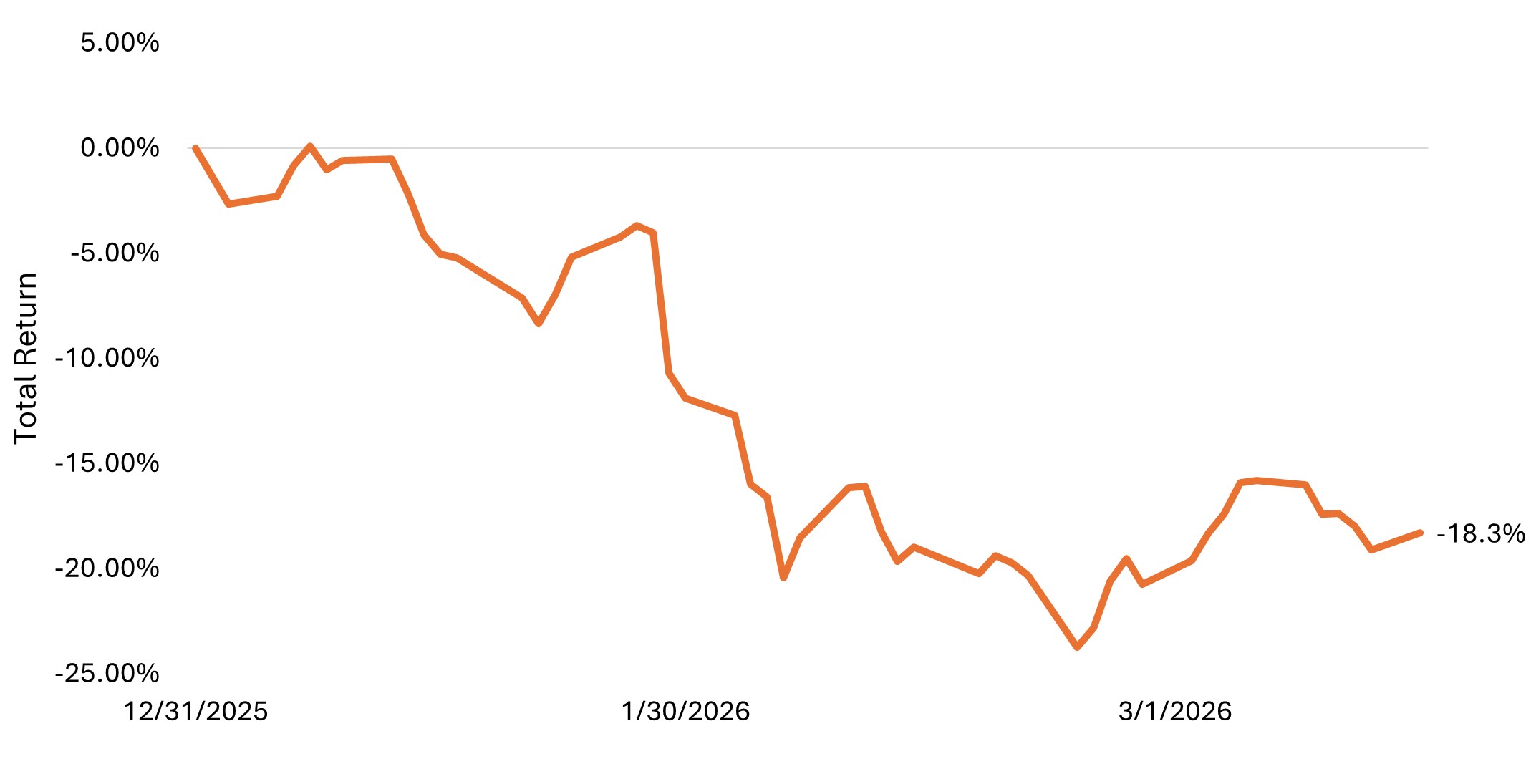

Where we’re seeing the hype manifest most acutely is in the market’s treatment of software. The software index is down roughly 18% year to date as investors price in disruption from AI. Some of that concern is legitimate, but we don’t think the market is distinguishing well between companies that will be genuinely disrupted and those that are adapting effectively.

Exhibit 3: S&P Software & Services Industry Index, year-to-date through 16 March 2026

Source: Bloomberg, as of 17 March 2026. The S&P Software & Services Select Industry Index comprises stocks in the S&P Total Market Index that are classified in the GICS Application Software, Interactive Home Entertainment, IT Consulting & Other Services and Systems Software sub-industries.

For high-quality software businesses, there’s more to their competitive position than the software itself – distribution, customer relationships, and implementation support all factor into the equation. Those advantages don’t disappear overnight.

We’re starting to see some stabilization in the space, but the longer-term sorting out process is underway, and we expect it to create real opportunities for active management.

IMPORTANT INFORMATION

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Quantitative Tightening (QT) is a government monetary policy occasionally used to decrease the money supply by either selling government securities or letting them mature and removing them from its cash balances.

S&P 500® Index reflects U.S. large cap equity performance and represents broad U.S. equity market performance. Index performance does not reflect the expenses of managing a portfolio as an index is unmanaged and not available for direct investment.

Volatility measures risk using the dispersion of returns for a given investment.