Key takeaways:

- As planning becomes more holistic and behavior-aware, advisors are looking for tools that can solve both the financial and emotional side of the retirement equation.

- Annuities with a guaranteed income option may help clients overcome the financial and psychological hurdle of losing the security of a salary, while life insurance offers tax‑free liquidity for estate planning or legacy goals.

- Importantly, these tools shouldn’t be treated as binary decisions. Partial allocation frameworks show that investments, annuities, insurance, and all the other tools in the financial planning toolbox can – and should – work together to solve specific client problems.

Early in my career, I worked at an insurance company where the “investment people” and the “insurance people” might as well have been on different floors – different language, different advisor audiences, different conversations.

That divide doesn’t hold up anymore. Today’s advisors are increasingly having one planning conversation that includes portfolios, annuities, and life insurance. This approach makes sense, because client goals don’t fit into neat categories; they overlap, with each goal dependent upon another. As a result, that one planning conversation might seek to solve a series of problems, from creating dependable retirement income and reducing the odds of a bad return sequence early in retirement to managing taxes and protecting a spouse or legacy.

The shift is more about mindset than products; specifically, it’s about moving from product selection to outcome design. Annuities and life insurance have moved out of silos and are now part of one broad planning conversation for advisors. And these tools are no longer optional add-ons – they’re becoming standard pieces of the financial planning playbook.

So, what’s driving the change? Part of it is simply the realities of today’s markets: Volatility, longevity risk, and higher sensitivity to downside are leading investors to seek new solutions. But an equally important part is the evolution of advice: As planning becomes more holistic and behavior-aware, advisors are looking for tools that can solve both the financial and emotional side of the retirement equation.

Solving the emotional side of retirement with annuities

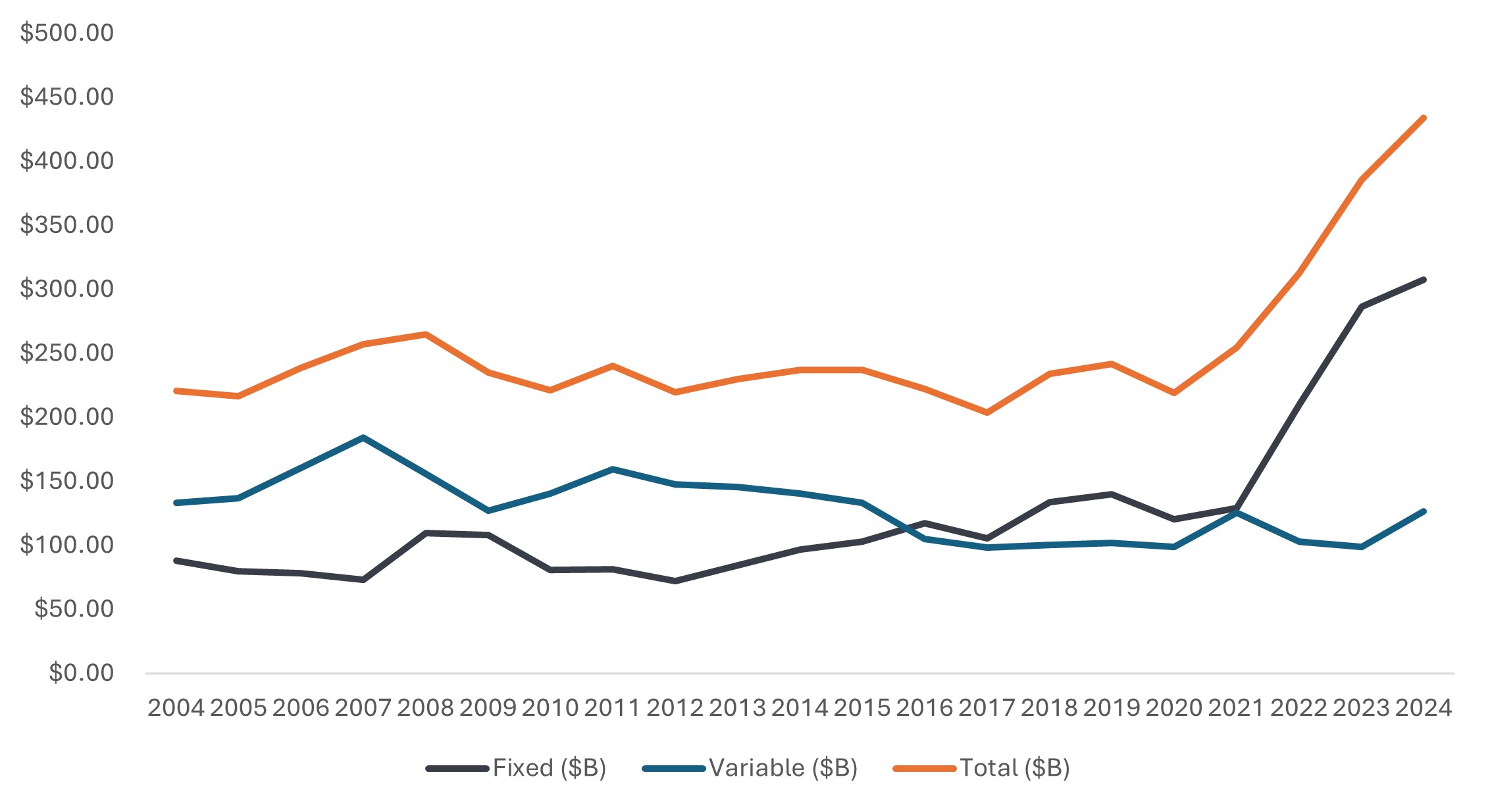

The idea of creating a “retirement paycheck” via annuities with a guaranteed income option has gained significant traction as everyday costs rise and investors hear more about the risks of outliving their savings. In fact, our 2025 Investor Survey found that retirees are seeking greater stability, and 54% are finding this through greater utilization of annuities. Losing the security of a salary is both a financial and psychological hurdle, because every dollar spent in retirement feels like a dollar that won’t be replaced.

Total U.S. individual annuity sales, 2004 – 2024

Source: U.S. Individual Annuities, 4th Quarter 2024, LIMRA, 2025.

Research also shows that many retirees spend far less than they safely could. A 2023 study showed that, after nearly 20 years in retirement, on average across all wealth levels, retirees still have 80% of their pre-retirement savings.1 Another study found that married 65-year-old households with at least $100,000 in assets withdraw just 2.1% per year on average from their retirement accounts.2 Introducing guaranteed income through annuities can help clients feel secure enough to use their savings more confidently and live a more fulfilling retirement.

This idea of fulfillment may seem uncomfortable for the spreadsheet minded. But as the industry places greater focus on behavioral finance, investor psychology, and emotional understanding, these considerations have become central to advisors’ value proposition – not to mention a source of greater client satisfaction.

Addressing uncertainty and volatility: Solving the security side of retirement

Ongoing market volatility and geopolitical uncertainty continue to push investors toward financial solutions with more certain outcomes. Annuities and life insurance play different but complementary roles in providing this type of reassurance and security.

Annuities help clients create an income floor, manage sequence‑of‑returns risk, and avoid withdrawing from portfolios at the worst possible time. We encourage investors to think about retirement spending using a Needs, Wants, and Wishes framework, where one’s needs are met with cash flows that are consistent. Social Security serves as a foundation for these cash flows, and the consistent income from an annuity may help to fill the remaining bucket. Importantly, having that level of certainty and security may help investors stay on course with investments that are earmarked for longer-term goals.

Life insurance may be valuable when clients need tax‑free liquidity for estate planning or legacy goals — especially for higher‑income and high‑net‑worth households. Along with that, for many, life insurance could be thought of as an investment and another way to diversify one’s assets, not only from the standpoint of asset class diversification, but also chronological diversification.

When it comes to life and investing, there is always some uncertainty we must be prepared for. That’s why flexibility and the ability to separate spendable income from growth capital can help clients stay invested and reduce the behavioral mistakes that volatility tends to trigger.

No longer a binary decision

Many advisors still see themselves as either “investment‑first” or “insurance‑first.” But this is a mindset that advisors need to get away from, in our view. In fact, the starting point shouldn’t be an advisor’s identity or even past areas of expertise; today, the starting point should be the client problem we’re trying to solve.

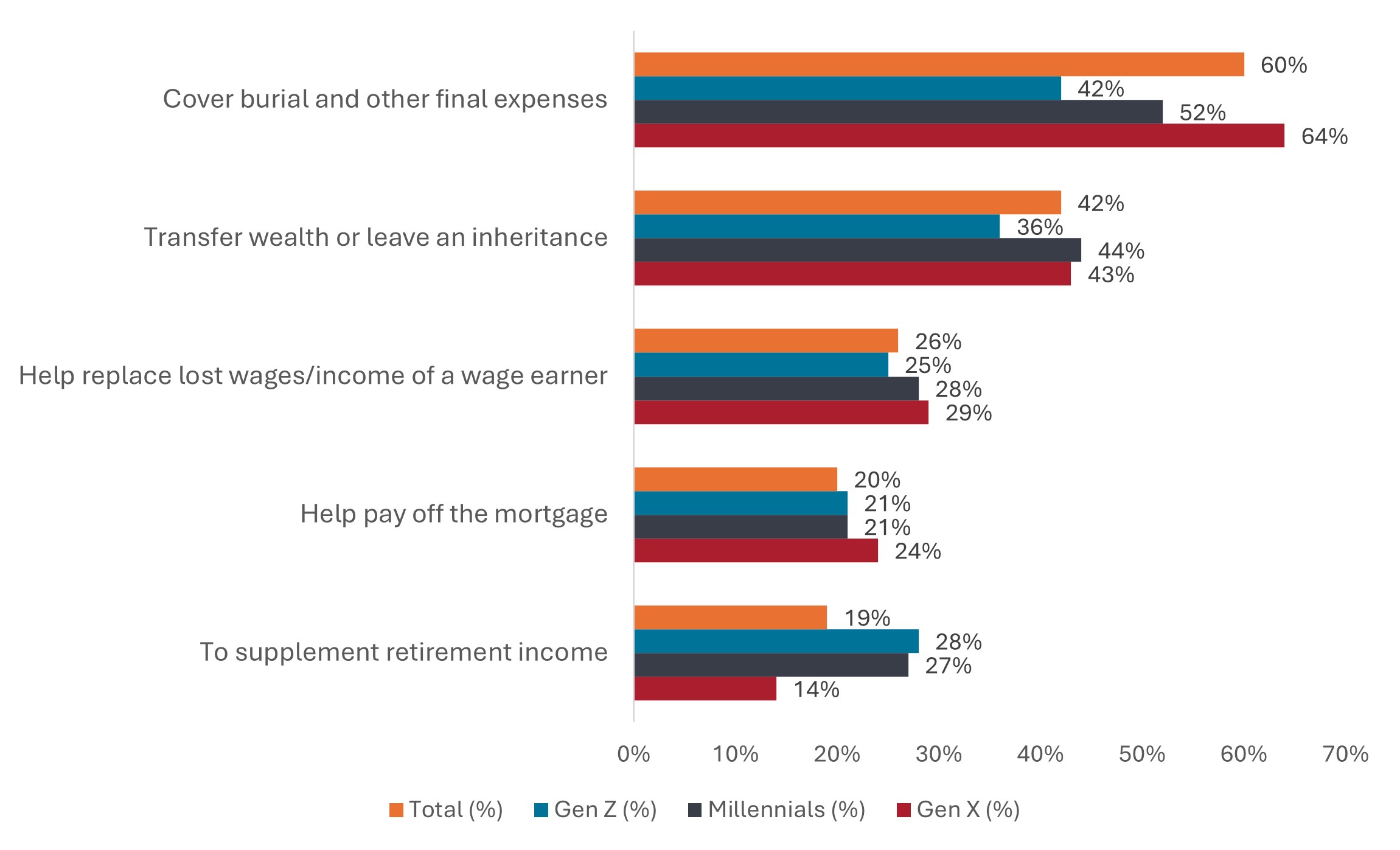

Reasons to own life insurance by generation (2025)

Source: 2025 Insurance Barometer Study, LIMRA, Life Happens.

To that end, when advisors frame the conversation around needs like income floors, longevity protection, survivor benefits, or legacy replacement, clients (and possibly advisors) are often more open to using annuities and life insurance to help meet specific goals. Focusing on needs and goals also helps frame the use of these products in a more positive and useful way.

Importantly, these tools shouldn’t be treated as binary decisions: It’s not an all‑or‑nothing choice. Partial allocation frameworks show that investments, annuities, insurance, and all the other tools in the financial planning toolbox can – and should – work together to solve specific client problems.

Clients’ needs change, and we must be willing to change with them. The financial solutions toolbox contains a vast array of options to help you address those changing needs. And whether you consider yourself a fiduciary or not, it’s your responsibility to find the best tools for the job.

Volatility measures risk using the dispersion of returns for a given investment.

1 BlackRock, EBRI, To Spend or Not to Spend, 2023 (updated from 2018)

2 Blanchett D. and Finke M. “Retirees Spend Lifetime Income, Not Savings.” Financial Planning Review, volume 8, no. 3 (September 2025).

IMPORTANT INFORMATION

Annuities are long-term investment vehicles designed to accumulate money on a tax-deferred basis for retirement purposes. They limit access to the investment as a result of a surrender charges and are subject to a 10% tax penalty on certain withdrawals. Riders are generally available for an additional charge. Variable annuities are subject to investment risk, and investment return and principal value will fluctuate.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

The information contained herein is for educational purposes only and should not be construed as financial, legal or tax advice. Circumstances may change over time so it may be appropriate to evaluate strategy with the assistance of a financial professional. Federal and state laws and regulations are complex and subject to change. Laws of a particular state or laws that may be applicable to a particular situation may have an impact on the applicability, accuracy, or completeness of the information provided. Janus Henderson does not have information related to and does not review or verify particular financial or tax situations, and is not liable for use of, or any position taken in reliance on, such information.